Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2025 edition covers Market Review for 2024, a discussion about the main themes for 2025, and some long-term multi-decade trends. In Shiuman’s Corner find out what my favourite books were from last year.

Markets

Market scorecard as of close on Friday March 14, 2025.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 24,553 | -0.8% | -0.7% |

| U.S. | S&P 500 | 5,639 | -2.3% | -4.1% |

| U.S. | NASDAQ | 17,754 | -2.4% | -8.1% |

| Europe/Asia | MSCI EAFE | 2,444 | -2.6% | 8.1% |

Source: FactSet

-

TSX higher in Friday afternoon trading, near best levels. Gains across the board. TSX declined 0.8% for the week. US equities finished sharply higher in Friday trading, ending near best levels with S&P capping its best session since November. Despite Friday’s bounce S&P 500 (-2.3%), Nasdaq (-2.4%), and Russell logged their fourth straight week of outsized losses.

-

U.S. stock indexes continued on their downward paths from the record highs set almost one month ago. Investors cited ongoing trade tensions, reciprocal tariff talk, and increasing skepticism over the effectiveness of the more assertive policy approach by the new U.S. administration.

-

This idea posited President Donald Trump’s sensitivity to a weaker stock market might temper negative policy actions and provide a floor of sorts for equities. But given the opportunity to deflect concerns of a recession in a Fox News interview last weekend, Trump declined to rule one out, characterizing the recent weakness as “a period of transition.” Recession worries appeared in other asset classes too, with U.S. corporate bond spreads hitting their widest levels since September 2024.

-

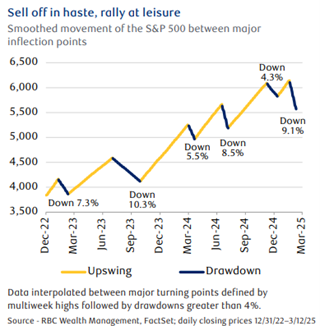

These negative headlines have contributed to the market malaise, but we also note that “recency bias” has likely influenced sentiment. Investors have ridden the equity market higher since the lows of October 2022 with few significant pullbacks (see chart). The approximately 9% decline this year is the largest in 18 months and follows a smaller December pullback. It could be argued investors had grown accustomed to infrequent downdrafts, even though the recent declines are a fairly normal part of the long-term stock market trajectory.

Economy

Canada

-

The Bank of Canada cut interest rates for the seventh time since June. The key interest rate was lowered by 25 basis points to 2.75% in an expected move with the central bank warning of an impending economic downturn from the U.S. trade war.

-

Governor Tiff Macklem said “we’re facing a new crisis,” but added the bank would proceed carefully with any further changes to the rate given the balance between lower economic activity and higher inflation caused by tariffs. RBC Economics expects the BoC to cut rates to 2.25% by summer.

-

Mark Carney has pledged to maintain retaliatory tariffs on U.S. goods, and it is possible he will call for a federal election in the coming weeks. Furthermore, a Carney-led government would work on removing interprovincial trade barriers and accelerate interprovincial projects with national interest.

U.S.

-

February’s US CPI data suggests that the Q1 bump was largely contained in January. Core CPI moderated (+0.2% MoM) after a January spike attributed to seasonality. Year-over-year core inflation moved down to 3.1%, in-line with our expectations.

-

The NFIB Small Business Optimism Index fell in February to 100.7, below its recent peak of 105.1 in December, and the NFIB’s Uncertainty Index rose to 104.0, the second-highest level on record.

Further Afield

-

Trade policy clouds continue to gather with U.S. President Donald Trump’s 25% tariffs on steel and aluminium coming into effect. The European Commission swiftly retaliated by imposing tariffs on a range of products worth $28 billion including jeans, motorbikes, peanut butter, and bourbon. Trump has vowed to respond, raising the risk of trade war escalation. However, tariffs are a less important issue for Europe than for Canada, in our view, as the region has a much lower exposure to the U.S. economy.

-

Despite these uncertainties, RBC Capital Markets increased its forecasts for euro area GDP growth significantly, citing German fiscal stimulus, higher EU defence spending, and a recovery in consumption. It now expects GDP growth of 1.4% in 2025 (up from 0.9%), followed by 1.9% in 2026 and 1.8% in 2027, up from 1.2% and 1.3%, respectively.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman