Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2024 edition covers Market Review for 2023, a Turning Point on interest rates, and advantages of Bonds. Plus my Book List for 2023.

Markets

Market scorecard as of close on Friday February 23, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 21,413 | 0.7% | 2.2% |

| U.S. | S&P 500 | 5,089 | 1.7% | 6.7% |

| U.S. | NASDAQ | 15,997 | 1.4% | 6.6% |

| Europe/Asia | MSCI EAFE | 2,280 | 1.0% | 1.9% |

Source: FactSet

-

TSX closed higher in Friday trading, near best levels. Most sectors higher. Canadian equities closed 0.7% higher last week at YTD highs and best level in nearly two years. TSX remains more than 775 points (~3.75%) below its record close from March 2022.

-

US stocks have continued to outperform as S&P 500 and DJIA hit all-time highs while Nasdaq is just a whisper away from its November 2021 record close. Nvidia alone added $225B+ in market cap on Thursday (more than the total market cap of any TSX-listed company).

-

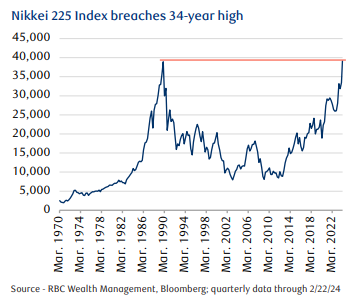

After blowout earnings/guidance from Nvidia helped spark a risk-on move in global equities, Canadian equities have continued to lag. Japan's Nikkei 225 hit a record high earlier last week, up nearly 17% YTD (partly attributed to the AI-driven chip demand boosting Japanese semiconductor stocks). European benchmarks notched fresh all-time highs on Thursday with the STOXX 600, France's CAC and Germany's DAX all hitting record levels (UK's FTSE a notable laggard).

A key factor behind the equity market's strength lately has been earnings results. Fourth quarter U.S. earnings are set to rise by just over 3% year-over-year, roughly double the expected pace. Though not remarkable in absolute terms, this growth is notable given the anticipated drag from higher interest rates on operating profits.

Economy

Canada

-

Canada’s inflation decelerated more than the Bloomberg consensus anticipated in January. The headline Consumer Price Index (CPI) rose 2.9% y/y last month, following December’s gain of 3.4% y/y, marking the lowest level since June 2023 and falling within the Bank of Canada’s (BoC) target range of 1.0%–3.0%.

U.S.

-

The Leading Economic Indicator (LEI) was down 0.4% month over month, marking the 23rd consecutive month of declines. This indicator usually correlates well with stock market performance, but the relationship has diverged since Q3 2022.

-

So, what has caused this breakdown? Specific aspects of the recent economic cycle are clearly different to what we’ve seen in the past, including an inflation spike caused by COVID-19 and deglobalization, and unprecedented advances in AI. While we don’t believe this indicator is past its prime, we do believe it needs to include more service-sector inputs given the evolving nature of the economy.

Further Afield

-

A resurgence in travel over the New Year holiday in China offers some signs of a pickup in consumer spending. More than 61 million rail trips were made in the first six days of the holiday period. The average daily sales of the services sector rose 52.3% y/y with rapid growth in tourism, cultural and sporting activities, catering, and lodging.

-

In the EU, negotiated wage data covering 75% of employees in the bloc’s five largest economies showed an increase of 4.5% y/y in Q4, pleasant progress from the prior period’s 4.7%. With inflation in the EU receding to 2.9%, this suggests to us that real wages are growing and should, in time, help prop up consumption.

Notes About Companies in Model Portfolio

-

Overall, earnings season appears to have progressed well. With 85% of S&P 500 companies having reported by midweek, Q4 2023 revenues and earnings were up 4% and 8%, respectively, beating the initial FactSet consensus forecasts of 3% and 1%, respectively, with demand and input costs in the quarter both better than feared.

-

As we look to the rest of 2024, earnings growth is expected to pick up. Analyst estimates suggest an earnings growth rate of nearly 9% for the year. And unlike the past year, this growth is anticipated to be more broadly distributed across various companies, not just the “Magnificent Seven”. This more evenly distributed earnings growth would be a welcome development, but this outlook is predicated on several assumptions: consumer and business demand that remain resilient and potentially improve, a deceleration in inflation, and lower interest rates.

-

Scotiabank and Bank of Montreal are scheduled to kick off the Canadian banks’ quarterly reporting season on Tuesday, followed by Royal Bank of Canada and National Bank of Canada on Wednesday and CIBC and TD Bank on Thursday. Provisions for credit losses and expenses are two potential areas that investors could scrutinize in the financial updates from the Canadian banks.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman