Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2024 edition covers Market Review for 2023, a Turning Point on interest rates, and advantages of Bonds. Plus my Book List for 2023.

Markets

Market scorecard as of close on Friday January 26, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 21,125 | 1.0% | 0.8% |

| U.S. | S&P 500 | 4,891 | 1.1% | 2.5% |

| U.S. | NASDAQ | 15,455 | 0.9% | 3.0% |

| Europe/Asia | MSCI EAFE | 2,211 | 1.5% | -1.1% |

Source: FactSet

-

Canadian equities finished slightly higher Friday in a very rangebound session. Sectors were mixed. TSX posted a 1.1% weekly gain, closing at best level this year after a sluggish start to 2024 trading.

-

US equities closed mixed in fairly quiet Friday trading, ending off some modest midday strength. S&P and Nasdaq each broke six-session gain streaks, though the major indices all notched weekly gains.

Economy

Canada

-

The Bank of Canada held the overnight rate unchanged for a fourth consecutive meeting, extending a pause that started after the last hike in July last year. Interest rates are already at levels that are high enough to restrict economic activity and wobbly-looking GDP growth and labour market backdrops mean the most likely trajectory for inflation going forward is still lower.

-

The post-meeting statement dropped an earlier reference to being prepared to raise interest rates further, but Macklem didn’t rule out additional tightening if inflation reaccelerates.

U.S.

-

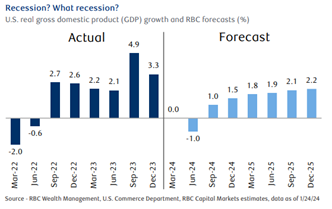

U.S. Q4 GDP jumped another solid 3.3% (annualized) in Q4 after surging by 4.9% in the third quarter. That leaves the annual growth rate in 2023 at 2.5%, up from 1.9% in 2022. There are still signs that economic momentum is slowing – the household saving rate continues to run below pre-pandemic levels and declining job openings are flagging a softening in the labour market.

-

The U.S. Federal Reserve is widely expected to hold the fed funds target range unchanged for a fourth consecutive meeting on Wednesday. Attention will be focused on any hints on the potential timing of a pivot to cuts.

Further Afield

-

As widely expected by market participants, the European Central Bank (ECB) held interest rates at 4% for the third consecutive meeting. In its policy statement, the central bank retained its stance on maintaining elevated interest rates for a “sufficiently long duration” to bring inflation back to its 2% target.

-

The People’s Bank of China announced on Wednesday a move to cut the required reserve ratio for all financial institutions by 50 basis point to 10%, effective Feb. 5.

Notes About Companies in Model Portfolio

The Tech sector will feature prominently on the earnings front with Apple, Microsoft, Amazon and Alphabet headlining the list of companies scheduled to provide financial updates during the week.

-

CN (CNR) reported its financial and operating results for the fourth quarter and year ended December 31, 2023. For the full year revenues were C$16,828 million, a decrease of C$279 million or 2%. Operating income was C$6,597 million, a decrease of C$243 million, or 4%. Adjusted net income was C$4,800 million, a decrease of C$334 million, or 7%.

-

Johnson & Johnson (JNJ) reported Q4 and full-year 2023 results. 2023 Full-Year reported sales growth of 6.5% to $85.2 billion with operational growth of 7.4% and adjusted operational growth of 5.9%. Operational growth excluding COVID-19 Vaccine of 9.0%. 2023 full-year earnings per share (EPS) of $5.20 decreasing 15.3% due to a special one-time charge in the Q1, and adjusted EPS of $9.92 increasing by 11.1%.

-

Procter & Gamble (PG) reported second quarter fiscal year 2024 net sales of $21.4 billion, an increase of three percent versus the prior year. Organic sales, which excludes the impacts of foreign exchange and acquisitions and divestitures, increased four percent. Diluted net earnings per share were $1.40, a decrease of 12% versus prior year primarily due to a non-cash impairment of the carrying value of the Gillette intangible asset. Core net earnings per share were $1.84, an increase of 16% versus prior year.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman