Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q4 2023 edition covers Market Review, the Type of Recession we may have, and how to build Resilience in portfolios.

Markets

** U.S. financial markets are closed today (Monday January 15) in celebration of Martin Luther King Jr. Day.

Market scorecard as of close on Friday January 12, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 20,990 | 0.3% | 0.2% |

| U.S. | S&P 500 | 4,784 | 1.8% | 0.3% |

| U.S. | NASDAQ | 14,973 | 3.1% | -0.3% |

| Europe/Asia | MSCI EAFE | 2,227 | 1.1% | -0.4% |

Source: FactSet

-

Canadian equities finished modestly higher Friday, well off best levels. TSX eked out a 0.3% weekly gain, off to a sluggish start to 2024 after a big two-month rally into year-end.

-

US equities finished narrowly mixed in fairly quiet Friday trading. S&P and Nasdaq logged good weekly gains after a sluggish start to 2024 trading last week.

-

Market action in the first few weeks has been relatively muted, contrasting with the strong gains witnessed towards the end of last year. This moderation can be attributed to a string of slightly stronger global economic data, prompting investors to reassess their expectations for interest rate cuts. We expect the timing and degree of rate cuts to be one of the biggest debates this year.

-

We foresee this fueling swings in the markets in both directions as investors recalibrate their expectations. Nevertheless, this year should mark a notable shift in the environment as central banks transition to a more accommodative policy. That has historically proven to be a more constructive backdrop for investors.

Economy

Canada

-

In-person spending made a comeback this holiday season. More Canadians opted to peruse bricks and mortar stores with online purchase volumes growing more slowly in Q4.

-

RBC’s own cardholder data suggests that household spending remained relatively firm over the holidays, and with weaker inflation data in October and November implying the amount purchased increased.

-

Vancouver and Toronto continue to be the least affordable housing markets, with the share of income a typical household would need to cover ownership costs being 102.6% and 84.1%, respectively. The light on the horizon remains the possibility that Canadians could see rate cuts later this year, which would help ease home ownership costs.

U.S.

-

US headline inflation growth rose to 3.4% in December, above consensus and our expectation for a 3.2% reading and up from 3.1% in November. The increase was supported by rising energy inflation while price growth in food and other non-energy components slowed.

-

Still, the central bank is expected to stay on a cautious path, especially against a still solid consumer backdrop and persisting resilience in the labour market. RBC Economics expects the first cut to the fed funds target range in Q2, 2024.

Further Afield

-

In recent months, a broad range of euro area economic indicators have shown signs of bottoming. RBC Capital Markets continues to think Q4 growth is likely to be softer than the 0.1% q/q expansion projected by the European Central Bank (ECB) in its December staff forecasts. Instead, it looks for a modest 0.1% q/q contraction, in line with consensus expectations, which would mark a shallow “technical recession.”

-

The annual gathering of the World Economic Forum kicks off today in Davos under the theme of Rebuilding Trust. The five-day meeting is anticipated to cover a number of timely themes, ranging escalating geopolitical tensions to challenges posed by AI.

Notes About Companies in Model Portfolio

-

UnitedHealth Group (UNH) reported 2023 results on Friday with revenues of $371.6 billion (+15% year-over-year). Earnings from operations were $32.4 billion, an increase of 13.8%. Adjusted earnings per share was $25.12 (up from $22.19 last year).

-

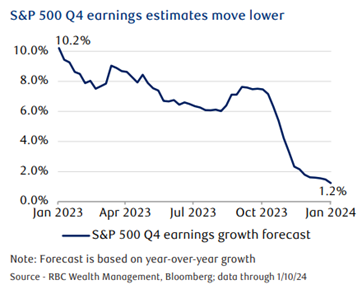

As Q4 earnings season is set to begin, Wall Street analysts have been cutting their growth expectations for the S&P 500; year-over-year growth is now expected to be just 1.2%, according to Bloomberg. This is down sharply from the start of 2023 (see chart above).

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman