Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q4 2023 edition covers Market Review, the Type of Recession we may have, and how to build Resilience in portfolios.

Markets

Market scorecard as of close on Friday December 18, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 20,529 | 1.0% | 5.9% |

| U.S. | S&P 500 | 4,719 | 2.5% | 22.9% |

| U.S. | NASDAQ | 14,814 | 2.8% | 41.5% |

| Europe/Asia | MSCI EAFE | 2,193 | 2.6% | 12.8% |

Source: FactSet

-

TSX finished lower in Friday afternoon trading, near worst levels. All sectors lower. Canadian equities rose 0.7% Thursday with TSX closing at its best level of 2023 (though came up just shy of intraday high from February).

-

US equities were mixed in Friday trading, though breadth narrow as equal-weighted index trailed cap-weighted S&P 500 by nearly 80bp. Major averages capped off another week of big gains with small-caps a standout while S&P higher for a seventh straight week, something that has happened only ten other times since 1990 (last time in 2017). Treasuries weaker with curve flattening; 10Y yield still holding below 4%.

-

U.S. equities are sharply higher on the week after the Federal Reserve indicated interest rate cuts are likely next year. All the major indexes are higher. The S&P 500 has outperformed the Nasdaq Composite, but both are higher, rising 2.21% and 1.97%, respectively.

Economy

Canada

-

Canada’s bank regulators left the mortgage stress test unchanged for the third year in a row. According to the Office of the Superintendent of Financial Institutions (OSFI), the minimum qualifying rate (MQR) for uninsured mortgages will remain at the higher of 5.25% or 2.0% above a borrower’s mortgage rate.

-

Canada’s sluggish labour productivity growth remains a source of concern to policymakers. Labour productivity fell 0.8% in Q3 according to data released by Statistics Canada last week, marking the sixth consecutive quarterly decline. The drop in productivity was mainly driven by a contraction in business output, while hours worked increased slightly. As a result, the federal government has faced mounting pressure to refocus on boosting investment, especially as Canada’s gross domestic product per capita has remained on a downward trend in recent years.

U.S.

-

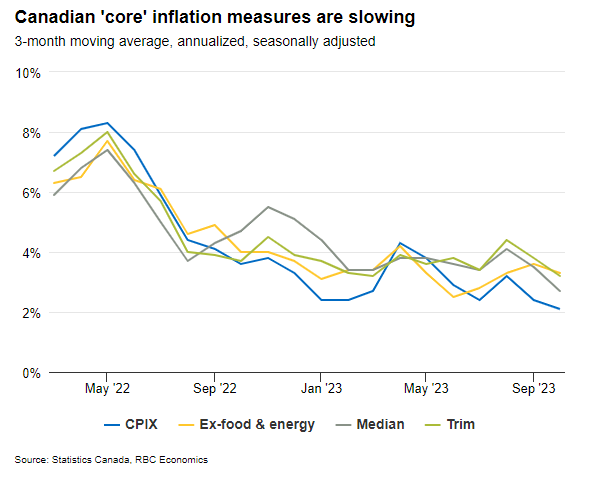

Tuesday’s inflation report was broadly in line with expectations as both headline and core CPI matched consensus expectations, coming in at 3.1% and 4.0%, respectively. A 2.3% decrease in energy prices helped push headline CPI slightly lower compared to October.

-

As widely expected, the Federal Reserve held the fed funds target range steady at 5.25% to 5.5% for a third consecutive meeting today as easing labour demand and slowing inflation readings over recent months move the central bank closer towards their mandates.

-

In addition to holding rates steady, policymakers also lowered their “dot plot” projections for 2024, with officials now seeing the fed funds rate ending 2024 at 4.6%, down from the September projection of 5.1%, suggesting the Fed anticipates cutting rates by 0.75% next year.

Further Afield

-

In a “finely balanced” decision, the Bank of England (BoE) maintained the Bank Rate at 5.25% to tame inflation that remains stuck at elevated levels—core inflation was a high 5.7% y/y in October. The BoE also maintained its “sufficiently restrictive for sufficiently long” message.

-

China experienced its most significant consumer prices decline in three years, indicating the difficulties encountered during the economic recovery. According to a statement released by the National Bureau of Statistics on Saturday, November’s consumer price index dropped by 0.5% m/m and y/y.

Notes About Companies in Model Portfolio

-

Dollarama Inc. (DOL) reported its financial results on Tuesday for the third quarter ended October 29, 2023. Sales increased by 14.6% to $1,477.7 million. Comparable store sales grew 11.1%, over and above 10.8% growth the previous year. EBITDA increased by 24.0% to $478.8 million, or 32.4% of sales, compared to 29.9% of sales. Operating income increased by 27.8% to $386.7 million.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman