Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can view the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q3 2023 edition covers Market Review, Concentration of Returns in U.S. equities and Estate Planning Basics.

On August 26 and 27 I will be riding 200km on my bicycle from Vancouver to Chilliwack and then to Hope, to raise money for BC Cancer Foundation. To find out more about the event called Tour de Cure, or why I ride, see my personal webpage.

Markets

Market scorecard as of close on Friday August 18, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 19,818 | -2.9% | 2.2% |

| U.S. | S&P 500 | 4,370 | -2.1% | 13.8% |

| U.S. | NASDAQ | 13,291 | -2.6% | 27.0% |

| Europe/Asia | MSCI EAFE | 2,058 | -3.4% | 5.8% |

Source: FactSet

-

TSX finished little changed Friday after recovering from initial weakness at the open. Sectors were mixed. TSX logged a 2.9% weekly decline, worst weekly performance since March. Stocks stabilized after morning weakness, capping off a down week as sentiment remains negative. Downbeat China headlines continued to dominate.

-

U.S. stocks struggled during the week, with the benchmark S&P 500 Index posting a third successive weekly loss for the first time in six months. August is typically a weak month for stocks as low trading volumes discourage active investments. But investors’ concerns over sticky inflation and a weakening consumer also fed into the bearish sentiment.

Economy

Canada

-

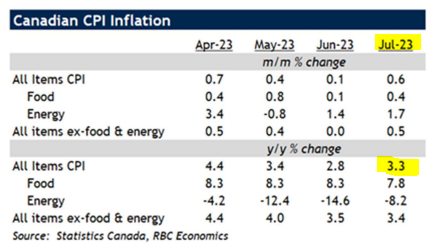

Canada’s July inflation data came in stronger than expected, remaining above the Bank of Canada’s (BoC) target and raising the likelihood of further monetary policy tightening in September. Headline Consumer Price Index (CPI) inflation increased to 3.3% y/y in July from 2.8% y/y in June as the pace of decline in energy prices moderated.

-

RBC Economics believes the BoC is likely to hold rates steady in September, but notes that policymakers appear quite willing to raise rates further if inflation proves more persistent than they expect.

U.S.

- Economic data published during the week was surprisingly strong. July retail sales growth of 0.7% m/m beat the consensus forecast of 0.4% and suggests to us that tighter monetary policy is still having remarkably little impact on real economic activity. And while spending on goods continues to moderate, the 1.4% m/m rise in spending at bars and restaurants indicates the service sector shows no signs of slowing down, in our view.

- The combination of generally stronger data pushed the Atlanta Fed’s GDPNow indicator of growth for the current Q3 up to 5.8%, implying the long-awaited recession may be pushed out until at least the end of the year.

Further Afield

-

UK inflation and labour data released this week intensifies the challenge for the Bank of England (BoE) to meet its 2% inflation target. We think the central bank is left with little to no choice but to keep raising rates, and we therefore continue to expect a 25 basis point (bps) hike in September.

-

China’s recent decision to lift a ban on group tours to Japan and South Korea has generated a wave of investor enthusiasm in the retail, cosmetics, and travel sectors in those two countries.

Notes About Companies in Model Portfolio

-

Johnson & Johnson (JNJ) announced that, based on preliminary results, its previously announced offer to its shareholders to exchange their shares of Johnson & Johnson common stock for shares of Kenvue common stock owned by Johnson & Johnson was oversubscribed

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman