Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can view the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q3 2023 edition covers Market Review, Concentration of Returns in U.S. equities and Estate Planning Basics.

Markets

Market scorecard as of close on Friday July 28, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 20,519 | -0.1% | 5.9% |

| U.S. | S&P 500 | 4,582 | 1.0% | 19.3% |

| U.S. | NASDAQ | 14,317 | 2.0% | 36.8% |

| Europe/Asia | MSCI EAFE | 2,196 | 0.7% | 13.0% |

Source: FactSet

-

TSX finished higher in Friday afternoon trading, near best levels. Most sectors higher. Canadian equities recorded moderate 0.1% weekly drop.

-

US equities finished higher in Friday trading as the major averages all capped off solid weekly gains, including S&P 500 up for a third-straight week (+1.0%).

-

U.S. stocks shrugged off recession concerns as the S&P 500 posted new 15-month highs during the week. At the halfway mark of Q2 earnings season, corporate results have surprised to the upside, as has U.S. economic growth. This strength has puzzled market participants concerned about the impact of higher interest rates and by leading economic indicators that are flashing cautionary signals.

Economy

Canada

-

According to the minutes from the Bank of Canada meeting, its Governing Council members remain open to further raising the policy rate in the months ahead if the downward trend in inflation shows signs of stalling or if renewed inflationary risks materialize.

-

Despite tighter financial conditions, Canada’s economic growth expectations continue to be revised upwards, as sturdy employment numbers and solid household consumption metrics continue to support. Despite investor optimism, economists continue to see some probability of an economic contraction over the next 12 months the current expansion.

U.S.

-

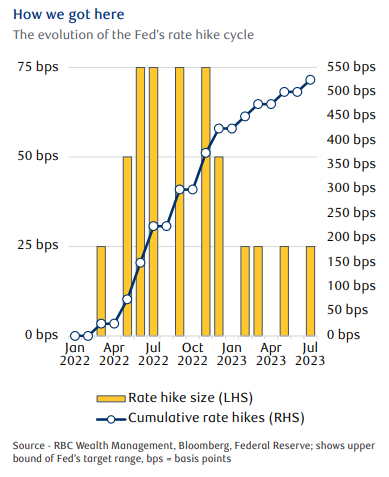

Last week the Federal Reserve raised its policy rate by a quarter of a percent (25 basis points), as was expected by just about everyone. There were barely any tweaks to the official policy statement. And Fed Chair Jerome Powell’s press conference? He took great pains to say absolutely nothing new while keeping all options going forward on the table, before making a notably brisk exit stage left. “[W]e maintain our view that the rate hike cycle is effectively over.” Global Insight Weekly, RBC Wealth Management, July 27, 2023.

-

The U.S. Commerce Department released its initial estimate of economic growth for Q2 2023. The surprisingly strong showing from the U.S. economy was met with a shrug, as the Federal Reserve’s interest rate hike and earnings excitement overshadowed the news of 2.4% annualized growth.

Further Afield

-

The European Central Bank (ECB) delivered on its interest rate hike promise at its July meeting, taking the deposit rate to 3.75% from 3.5%, in line with our expectations.

-

Investor sentiment towards Asian equities was largely boosted after the July meeting of China’s Politburo on Monday, which struck a dovish tone. The country’s top leadership acknowledged that China’s economic recovery faces challenges, and pledged to announce more countercyclical policies to boost demand and push for high-quality economic development.

Notes About Companies in Model Portfolio

-

CN (CNR) on Tuesday reported its financial and operating results for the second quarter ended June 30, 2023. Revenues of C$4,057 million, a decrease of C$287 million, or 7%. Operating income of C$1,600 million, a decrease of C$169 million, or 10%. In light of CN's second quarter results and revised expectation of weaker than anticipated volumes in the second half of 2023, CN is updating its full-year outlook and now expects flat to slightly negative year-over-year growth in adjusted diluted EPS in 2023

-

The Coca-Cola Company (KO) on Wednesday reported second quarter 2023 results. Net revenues grew 6% to $12.0 billion, included 10% growth in price/mix and 1% growth in concentrate sales. Operating margin decline (31.6% versus 30.7% in the prior year) was primarily driven by items impacting comparability and currency headwinds. Comparable EPS (non-GAAP) grew 11% to $0.78.

-

Microsoft (MSFT) reports Q4 – Q4 revenue was $56.19B, up 8% year-over-year (YoY). Cloud revenue grew 21% YoY and 23% cc, a deceleration from 29% cc last quarter. The headline was AI Services revenue, which contributed one point to Azure growth. Microsoft expects AI contribution to be gradual but did highlight FY24 contribution to be more meaningful in second half of 2024 as Azure AI scales.

-

Procter & Gamble (PG) reported fourth quarter and fiscal year 2023 results on Friday. PG reported fiscal year 2023 net sales of $82.0 billion, an increase of two percent versus the prior year. The Company generated operating cash flow of $16.8 billion and net earnings of $14.7 billion for the fiscal year.

-

TC Energy (TRP) reported Q2 2023 results with EBITDA C$2.47B. Following the sale of a 40% equity interest in Columbia Gas and Columbia Gulf TC Energy continues to expect 2023 comparable EBITDA to be +5-7% y/y.

-

-

TC Energy announce Thursday that its board has approved plans for TC Energy to separate into two independent, investment-grade, publicly listed companies through the spinoff of TC Energy's Liquids Pipelines business.

-

-

Visa (V) reported Q3 2023 Visa with $8.12B in net revenue and $2.16 adjusted earnings per share (EPS). Despite the continued rhetoric of a possible weakening consumer, Visa’s print is not showing signs of cracking, with FQ3/23 exceeding expectations and FQ4/23 guidance largely consistent with prior expectations. The travel recovery continued through the quarter as cross-border travel related spend excluding intra-Europe grew 34% y/y and is now 39% above 2019 levels. China cross-border travel still well below 2019 levels, while travel into Asia was up to 107% of 2019 levels.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman