Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can view the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q2 2023 edition covers Market Review, Recession Scorecard and Focus on Bonds.

Markets

Market scorecard as of close on Friday July 14, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 20,262 | 2.2% | 4.5% |

| U.S. | S&P 500 | 4,505 | 2.4% | 17.3% |

| U.S. | NASDAQ | 14,114 | 3.3% | 34.8% |

| Europe/Asia | MSCI EAFE | 2,189 | 4.9% | 12.6% |

Source: FactSet

-

TSX finished slightly lower Friday in a very quiet, rangebound session. Sectors were mixed. TSX posted a 2.2% weekly gain, more than recouping the previous week's decline. Canadian dollar sharply lower against USD, but still up on the week vs the greenback ($1.32 CAD to $1.0 U.S or $0.76 U.S. to $1.0 CAD).

-

US equities were mostly lower in Friday trading, ending worst levels, though stocks still posted a solid weekly gain. Big tech mostly higher with social media the standout. Treasuries weaker with the curve bear flattening after a big rally over the first four days of the week.

-

“There are positive signs the stock market rally should have some staying power. Still, investors shouldn’t get too far ahead of themselves given economic and earnings growth uncertainties later this year and next... Q2 earnings results and management guidance for upcoming quarters could provide some hints about the future path of the economy and earnings.” –Global Insight Weekly by RBC Wealth Management, July 13, 2023. Read the full article on my website here.

Economy

Canada

-

The Bank of Canada (BoC) is taking out more insurance against inflation risks. A second consecutive 25 bps hike by the BoC (following a two-meeting pause) lifted the overnight rate to 5.00% this month. The hawkish policy statement shows growing concern inflation will get stuck above the BoC’s 2% target.

-

B.C. port workers agreed to a four-year deal. The 7,400 dock workers ended their 13-day strike that had halted traffic at 30 B.C. ports, with 63,000 shipper containers stuck on vessels waiting to be unloaded. The strike disrupted around $9.7 billion in trade, according to a Greater Vancouver Board of Trade estimate.

-

Tighter financial conditions have started to work their way through the economic backdrop driving the unemployment rate up to 5.4% from 5.2% as Canadian firms experience varying degrees of profit margin compression.

U.S.

-

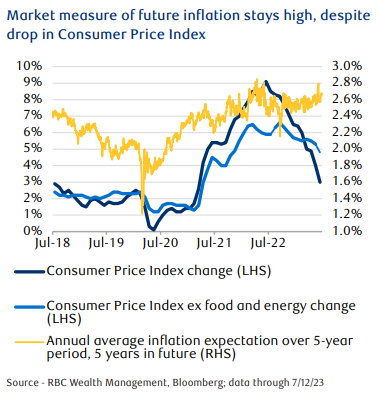

The Consumer Price Index (CPI) was up 3% y/y in June, the smallest annual increase in over two years. Core inflation—which strips out food and energy price changes—was up 4.8% y/y, above the Federal Reserve’s target but well below the 6% increase in November 2022.

-

While we believe the CPI data has likely ended the possibility of a second hike this year, we are not convinced the central bank will be as anxious to cut rates as investors may hope. We think labor markets are very unlikely to provide an impetus for near-term rate cuts, as evidenced by last week’s strong nonfarm payroll data and 3.6% unemployment rate for June.

Further Afield

-

In the UK, private sector pay growth reached 7.7% on a three-month annualized basis, up slightly from the prior period. Key drivers underpinning the continued surge were higher inflation expectations on the part of consumers and businesses and a tight labour market.

-

Chinese Premier Li Qiang chaired a symposium with major Chinese internet firms to promote development of the “platform economy” on Tuesday. Li mentioned the platform economy has played a prominent role in China’s development and that it should make a more important contribution in the future. He also urged platform companies to remain confident about China’s development while urging authorities to establish a more transparent regulatory environment.

-

As the Chinese economy struggles for momentum, European equities are seen as particularly vulnerable given their relative exposure to the region. According to J.P. Morgan, European stocks could see renewed headwinds amid signs of weakening demand in Asia, which could lead to earnings disappointment in the second-quarter reporting season.

Notes About Companies in Model Portfolio

-

Microsoft (MSFT) There is a clear path forward for Microsoft’s acquisition of Activision, as a federal judge denied the Federal Trade Commission’s (FTC) motion for a preliminary injunction to halt the deal. The FTC can still bring the case to the U.S. Court of Appeals. The only remaining hurdle is the Competition and Markets Authority (CMA) in the United Kingdom. Microsoft and the CMA agreed that it would pause litigation and try to negotiate a settlement on any remaining issues with the transaction.

-

UnitedHealth Group (UNH) reported Q2 2023 results on Friday with revenues of $92.9 billion up 16% year-over-year. Q2 2023 earnings from operations were $8.1 billion, an increase of 13%.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman