Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can view the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q2 2023 edition covers Market Review, Recession Scorecard and Focus on Bonds.

Markets

Market scorecard as of close on Friday July 7, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 19,831 | -1.6% | 2.3% |

| U.S. | S&P 500 | 4,399 | -1.2% | 14.6% |

| U.S. | NASDAQ | 13,661 | -0.9% | 30.5% |

| Europe/Asia | MSCI EAFE | 2,088 | -2.1% | 7.4% |

Source: FactSet

-

TSX finished slightly higher Friday, well off best levels. Sectors were mixed. Health care, energy and materials the outsized gainers, financial modestly higher. TSX logged a 1.6% weekly decline after posting its best weekly performance since Feb-2021 last week.

-

US equities finished mostly lower in relatively quiet Friday trading, with the S&P seeing an accelerating selloff from best levels through the afternoon. All major indices logged weekly declines. Big tech was mostly lower.

Economy

Canada

-

Canadian jobs growth surprised to the upside, bolstering case for a Bank of Canada (BoC) rate hike next week. However, unemployment rate also rose more than expected and wage growth decelerated. June LFS showed Canada added 60K jobs, blowing past ~20K consensus. Unemployment rate rose 0.2 percent to 5.4% as more people searched for work.

-

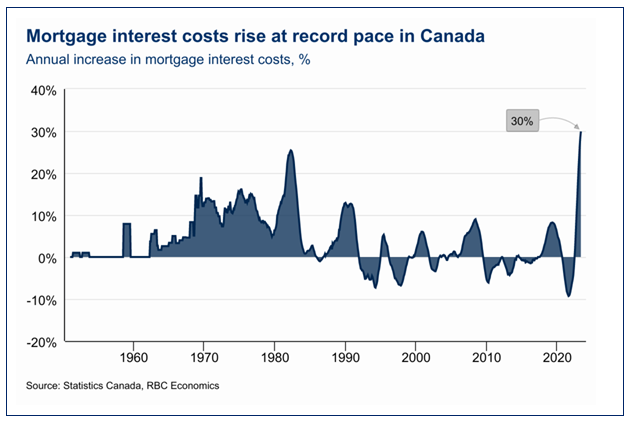

Inflation fell enough in May to hit rates at the top of the BoC’s target range. But a series of new data releases suggest consumer demand hasn’t slowed enough yet to deter regulators from following June’s 25 basis point hike with another Wednesday, according to RBC Economics.

-

Canadian trade balance swung to a $3.4B deficit, the largest since Oct 2020, from $894M surplus in April. StatCan reported imports rose 3.0% while exports declined 3.8%. Energy exports declined 7.3% due to lower prices.

-

Not many changes to the bearish talking points last week, which continue to center around the risks of higher-for-longer Fed policy, particularly after several hotter than expected labor market data points this past week. Market median terminal rate now around 5.40%, highest since March before banking turmoil, while year-end 2024 fed funds rate of ~4.25% up more than 35 bp from last week.

-

Treasury Secretary Yellen returned from a four-day trip to China stating that meetings with Chinese officials were “direct, substantive and productive.” Officials from the two nations discussed recent export restrictions, national security, and climate change.

Further Afield

-

Overseas, ECB President Lagarde said in an interview with French press that more work is still needed to bring inflation down and reach its target.

-

Chinese Premier Li reiterated pledge to speed up policy measures to bolster economy. However, lack of specifics and follow-through continues to disappoint markets.

Notes About Companies in Model Portfolio

-

Market in a bit of a waiting mode ahead of the week's coming inflation data and the start of Q2 earnings season, starting with U.S. banks on Friday.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman