Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can view the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q2 2023 edition covers Market Review, Recession Scorecard and Focus on Bonds.

Markets

Market scorecard as of close on Friday June 9, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 19,892 | -0.7% | 2.6% |

| U.S. | S&P 500 | 4,299 | 0.4% | 12.0% |

| U.S. | NASDAQ | 13,259 | 0.1% | 26.7% |

| Europe/Asia | MSCI EAFE | 2,107 | 0.4% | 8.4% |

Source: FactSet

-

TSX ended lower in rangebound Friday trading, just off worst levels. Most sectors down. Canadian equities fell 0.7% on the week with TSX notching its sixth decline in seven weeks.

-

US equities mostly higher in very quiet Friday trading. The S&P ended off best levels, just under the 4300 level, though highest finish since Aug-22. Friday’s modest gain also came after the index ended Thursday up more than 20% from its 52-week low.

-

Friday’s uneventful session ended a very quiet week though this week should be much more interesting with CPI and the Fed. Fed expected to leave policy unchanged, but it is a close call.

-

At nearly the midway point of the year, the S&P 500 Index has proven surprisingly resilient despite numerous headwinds. These include multiple Fed rate hikes amid economic uncertainty, instability in the U.S. regional banking system, and corporate earnings expectations that have been, until recently, on the decline.

-

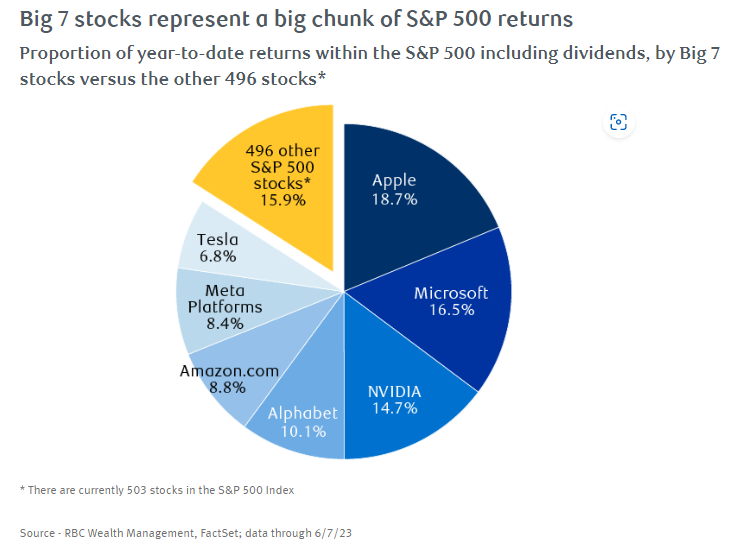

The S&P 500 is up 12.0 percent including dividends on a year-to-date basis. However, seven large technology stocks represent 84% of that return. Excluding these seven stocks the rest of the S&P 500 return was 2.5%. Read the whole article on this topic.

-

While the S&P 500’s 12 percent year-to-date total return looks pretty good on the surface, there are currents underneath that may be driving many portfolios to underperform the index.

Economy

Canada

-

Following two meetings with no policy changes, the Bank of Canada (BoC) decided last Wednesday to resume its monetary tightening campaign. The 25 basis point (bps) hike was a surprise to markets, and brought the benchmark overnight interest rate to 4.75%.

-

Canadian households are beginning to feel the impact of higher interest rates, but tighter monetary policy hasn’t stopped a rebound in domestic housing market activity. According to RBC Economics, home resales rose nationwide in April by more than 11% month over month, the fastest pace in nearly three years.

U.S.

-

U.S. service and manufacturing activity continued to weaken in May. On Monday, the Institute for Supply Management (ISM) reported its U.S. Services Purchasing Managers’ Index (PMI) fell to 50.3 in May from 52.1 in April. Although the index remained above the 50.0 level, which the ISM says indicates growth, this month-over-month slowdown appears to highlight the growing risk of recession.

-

Initial jobless claims have reached the highest level since October 2021. On Thursday, the Department of Labor announced that initial claims for state unemployment benefits rose to 261,000 for the week ended June 3, up 28,000 from the week prior. While the overall job market remains tight, with an unemployment rate of only 3.7%, we believe the increase in claims is an early sign that more cracks are forming in the labor market.

Further Afield

-

The eurozone is in a technical recession. The latest revisions to Q1 GDP figures suggest growth dipped by 0.1%, a second quarterly decline after Q4’s 0.1% contraction. But an important factor of a recessionary environment is absent, with the unemployment rate at a 25-year low.

-

Chinese exports fell 7.5% y/y to US$284 billion in May, worse than consensus expectations. The number indicates weakened global demand, in our view. Exports to most destinations decreased, with double-digit declines to markets including the U.S., Japan, Southeast Asia, France, and Italy.

Notes About Companies in Model Portfolio

-

Apple (AAPL) At its Worldwide Developers’ Conference (WWDC), Apple previewed its VR headset (Vision Pro AR Headset) last Monday, to be released in early 2024 at ~$3,500 U.S. The M2 Ultra chip was also in focus at the event as Apple announced its 15" Macbook Air, Mac Studio, and Mac Pro hardware would get rolled out with the M2 Ultra Chip.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman