Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday February 24, 2023.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 20,219 | -1.4% | 4.3% |

| U.S. | S&P 500 | 3,970 | -2.7% | 3.4% |

| U.S. | NASDAQ | 11,395 | -3.3% | 8.9% |

| Europe/Asia | MSCI EAFE | 2,035 | -2.5% | 4.7% |

Source: Bloomberg, RBC Wealth Management

-

TSX ended slightly higher in Friday afternoon trading, after spending most of the session in negative territory. Most sectors lower. Canadian equities declined 1.4% for a third straight weekly drop.

-

US equities weaker Friday but off worst levels. S&P 500 down for a third straight weekly pullback, down 2.7%.

-

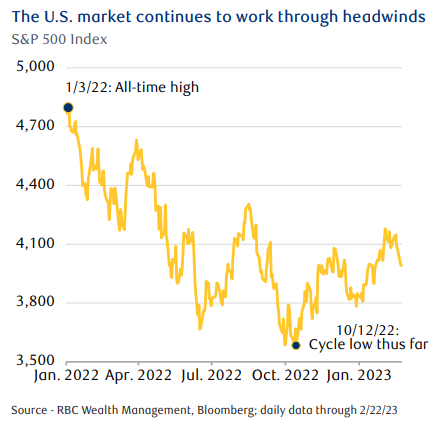

Following a strong run since last autumn, the U.S. equity market has been wobbly. Uncertainties that had previously receded have come back to the fore, generating volatility and downside in major U.S. indexes. While the S&P 500 shot up almost 17 percent from the October 2022 low through early February, it has pulled back 4.5 percent since then. As of last Wednesday’s close, the index is 16.8 percent below the all-time high reached in early 2022.

Economy

Canada

-

The January consumer price index (CPI) rose 5.9% y/y, a comforting sign that a deceleration in inflation is occurring. Although inflation data continue to come in well above the Bank of Canada’s 2% target, we think the continued easing of inflation promotes a positive tone for the central bank to hold rates at 4.5% at its March 8 policy meeting.

-

Canadian headline retail sales have continued to advance as nominal consumption metrics in the economy show some sustained signs of resilience. Retail sales increased 0.5% m/m in December. That being said, despite the nominal headline strength, when adjusting retail sales for seasonality and inflation, sales growth is not nearly as impressive as Canadians continue to experience the effects of above-trend inflation.

U.S.

-

The minutes of the Fed’s most recent meeting emphasized a view that additional rate hikes are likely to be needed as the central bank continues to fight inflation above its target level.

-

One beneficiary of the shift toward higher yields is the U.S. dollar. The DXY Dollar Index, which tracks the greenback on a roughly trade-weighted basis against a basket of global currencies, is up 2.4% so far in February.

Further Afield

-

The UK and European economies seem to be more resilient than anticipated. Both surprised to the upside of consensus with the February S&P Global Eurozone Composite Purchasing Managers’ Indexes jumping to 53 and 52.3 in the UK and Eurozone, respectively, from below 50 at year-end 2022.

-

Earnings in Europe and the UK combined have also been resilient. With just over half of companies having reported, positive trends are becoming apparent. Top-line growth has been very robust—over 10%—thanks to strong demand and pricing. Flow-through to earnings has been limited, however, due to higher costs including wage inflation.

Notes About Companies in Model Portfolio

-

Berkshire Hathaway (BRK.A, BRK.B) reported operating results for the fourth quarter and full year of 2022 on Saturday. For the fourth quarter, revenue, including realized and unrealized gains and losses from Berkshire's investment and derivative portfolios, declined 17.6% to $92.6 billion from $112.4 billion in the prior-year period on a marked decrease in gains from the investment portfolio. The company closed the year with $128.6 billion in cash and cash equivalents, down from $146.7 billion at the end of 2021, despite putting $34.3 billion (net of sales) in stock purchases and paying $11.5 billion to acquire Alleghany.

-

Nutrien Ltd. (NTR) today announced that the Toronto Stock Exchange (TSX) has accepted Nutrien's notice to commence a normal course issuer bid (NCIB) to purchase outstanding common shares representing up to five percent of its issued and outstanding common shares.

-

TD Bank Group (TD) today announced that it has agreed to a settlement in principle relating to litigation involving the Stanford Financial Group. Upon final approval of the settlement by the Court, TD will pay $1.205 billion (USD) to the court-appointed receiver for the Stanford Receivership Estate. TD expressly denies any liability or wrongdoing with respect to the multi-year Ponzi scheme operated by Stanford and makes no admission in connection to any Stanford matter as part of the settlement.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman