Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday September 23rd, 2022.

| Equity Indices | Level | 1 week | YTD |

| S&P/TSX Composite | 18,481 | -4.7% | -12.9% |

| S&P 500 | 3,693 | -4.6% | -22.5% |

| NASDAQ | 10,868 | -5.1% | -30.5% |

| Euro Stoxx 50 | 3,349 | -4.3% | -22.1% |

| Hang Seng | 17,933 | -4.4% | -23.4% |

Source: Bloomberg, RBC Wealth Management

-

TSX closed sharply lower in Friday afternoon trading, near worst levels. All sectors down, energy and materials the outsized decliners, financial, real estate, consumer discretionary, utilities, industrials and health care other laggards. Tech and staples held up best. Canadian equities declined 4.7% this week. BoC Governor Poloz said Canadian economy is in a strong position but warned against entrenched inflation and acknowledged nobody knows if recession can be avoided.

-

US equities were lower in Friday trading, though finished well off worst levels. Major indices capped big weekly losses, with S&P logging its fourth weekly drop of more than 3% in the past five weeks. Energy was the notable sector decliner after oil sold off. Treasuries were mostly lower with curve flattening; 2Y yield earlier breached 4.25%.

-

Stocks were under pressure with the S&P at one point violating the 16-Jun closing low, however regained that level in late day trading. Evaporation of the early-summer rally has accelerated this week after a flurry of worldwide central-bank hikes, particularly the Fed's 75bp hike Wednesday.

-

Path of least resistance for equities remains to the downside amid the broadly reiterated raise-and-hold messaging that has heightened concerns about the possibility of a hard landing and lent credence to more bearish analyst forecasts. Coming Q3 earnings season also a big focus, especially the degree to which estimates may still need to come down to reflect deteriorating macro backdrop. Nevertheless, also some thoughts market may be ripe for an oversold bounce with broad and growing pessimism a possible contrarian buy indicator.

-

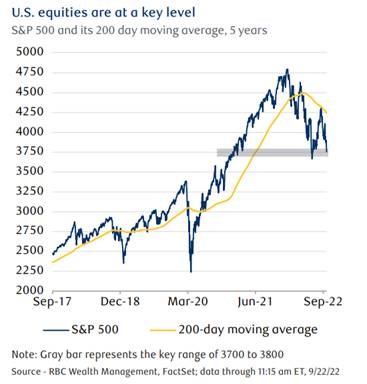

Technically speaking, the week’s moves have renewed concerns around where the equity market will bottom this cycle. It’s still too early to know whether the June 2022 lows will hold, according to RBC Capital Markets, LLC Technical Strategist Rob Sluymer. However, the broader point is that we believe the 3700–3800 range to be critical because the next level of support, should that range be broken, is near 3500 for the S&P 500. A value of 3500 would represent a further 6% to 7% contraction from today’s levels.

Economy

Canada

-

Canadian inflationary pressures decelerated more sharply than anticipated in August, with headline CPI registering a 7.0% y/y increase, 0.3 percentage points below consensus estimates. This marks the second consecutive month of slowing headline inflation, down from 7.6% in July.

-

Alongside elevated inflation, rising interest rates have been another key headwind for the financial markets. Following the BoC’s September rate hike of 75 basis points (bps), the overnight policy rate now sits at 3.25%, having risen 300 bps since the beginning of the year. As we approach the end of 2022, the futures market is pricing in a terminal rate of approximately 4%, implying another 75 bps of rate hikes are still on the table.

U.S.

-

Economically speaking, the Fed’s 75 basis point rate hike, which brought the federal funds rate into a range of 3.0% to 3.25%, was the highlight of the week. The Fed remains hopeful of engineering a “growth recession” according to its updated projections and Powell’s post-meeting press conference. Market reaction was less optimistic as equities sold off sharply.

-

RBC Economics maintains a more cautious outlook with a mild recession expected in early 2023 that gives way to unemployment rates closer to 5.0 percent, before the Fed delivers rate cuts in the back half of next year.

Further Afield

-

On Friday the new UK Chancellor Kwasi Kwarteng announced a mini budget that featured tax cuts to be funded by borrowing. Markets reacted negatively including a sharp drop in sterling.

-

The Bank of Japan (BoJ) stayed on hold, keeping its yield curve control policy and asset purchase program unchanged. The yen weakened further against the U.S. dollar following the BoJ’s announcement, falling to its lowest level since 1998.

Notes About Companies in Model Portfolio

-

Brookfield (BAM.A) announced that its board has unanimously approved the transaction for the public listing and distribution of a 25% interest in its asset management business. The transaction will result in the division of Brookfield into two publicly traded companies - the Corporation and the Manager - with the holders of Brookfield's class A limited voting shares, class B limited voting shares and Series 8 and 9 class A preference shares becoming shareholders of the Manager on completion. The transaction will enable Shareholders to access a leading pure-play global alternative asset management business, through the Manager. Brookfield Corporation will continue focusing on deploying capital across its operating businesses, growing its cash flows and compounding that capital over the long term.

-

Costco Wholesale (COST) reports Q4 revenues of $72.09B vs FactSet estimate of $72.04B. With consumers focused on value amid inflation and economic uncertainty, we are not surprised that members continue to look to Costco for savings. Considering both this factor and the long-standing loyalty its members have exhibited (with renewal rates in the low-90s in the U.S. for the last several years).

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman