Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday February 25, 2022.

| Equity Indices | Level | 1 week | YTD | 52-week |

| S&P/TSX Composite | 21,106 | 0.5% | -0.6% | 16.9% |

| S&P 500 | 4,385 | 0.8% | -8.0% | 15.0% |

| NASDAQ | 13,695 | 1.1% | -12.6% | 3.8% |

| Euro Stoxx 50 | 3,971 | -2.5% | -7.6% | 15.6% |

| Hang Seng | 22,767 | -6.4% | -2.6% | -22.9% |

Source: Bloomberg, RBC Wealth Management

-

TSX closed higher in Friday afternoon trading, near best levels. Most sectors ahead led by energy, financial, and materials with utilities the laggard. TSX recorded a 0.5% gain on the week, following last week's 2.5% drop the index is still in negative territory YTD.

-

US equities were higher in fairly quiet Friday trading, with major indices ending near best levels and finishing mostly higher in a choppy week. Friday's price action came after stocks finished higher on Thursday, rebounding from a big selloff at the open. All sectors seeing good gains.

-

Latest bout of upside seems to be a function of headlines about Russia's willingness to hold high level talks with Ukraine. Overall, geopolitical developments remain extremely fluid and there continues to be a lot of uncertainty about what Putin ultimately wants, as well as what he can actually achieve.

-

Other "positive" spin surrounding geopolitics includes thoughts Russian invasion will be over quickly and decision by Western governments not to impose the harshest sanctions. Oversold conditions and technical/options dynamics also cited as supportive.

Russia-Ukraine Conflict

-

Financial and energy markets have been jolted by Russia’s precision missile strikes on Ukraine and rapid deployment of troops, tanks, and armored vehicles deep into Ukrainian territory.

-

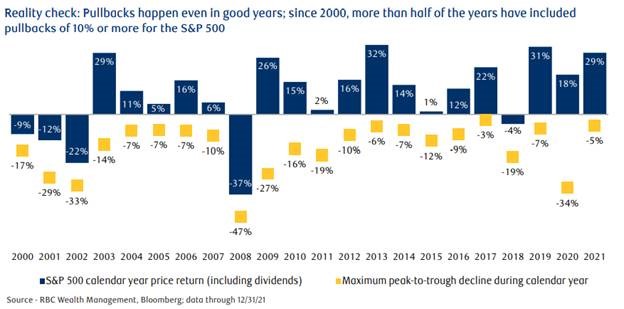

In the 18 post-World War II events that we evaluated, the S&P 500’s selloff was limited in magnitude at 6.2 percent, on average, and typically played out over a brief period. While this 6.2 percent level of decline is nothing to dismiss, it’s well within the bounds of a typical pullback in many scenarios that often confront markets.

-

On average, the pullbacks and corrections tended to last 30 days from the time the selloff began until the market climbed its way back to even. This occurred despite the fact that many of the actual events lasted longer—sometimes much, much longer.

-

Ultimately, after the immediate equity market impact of the Russian military assault fades, the trend of the U.S. and global economic and earnings growth will set the tone for developed market equities going forward, in our view.

-

The good news is, heading into this crisis, all seven of our leading U.S. economic indicators were healthy—flashing green—and none of them were hinting of recession risks. The current Q4 2021 corporate reporting season, which is drawing to a close, has shown solid earnings, revenue, and profit margin trends.

Economy

Canada

-

The Canadian economy has historically benefitted from rising commodity prices, as terms of trade (the ratio of a country’s export prices to import prices) generally turn positive after a commodity rally. This has implications for Canadian economic growth, typically providing a lift across the board as a result of Canada’s commodity-heavy exports.

-

While improving terms of trade can serve as a modest tailwind to the Canadian dollar over the medium to long term, the loonie could remain under pressure in the near term owing to the prevailing risk-off sentiment which typically bolsters the U.S. dollar’s appeal

U.S.

-

For the Fed, the invasion and NATO’s likely response create several potential concerns, in our opinion. Declining risk appetite and consumer balance sheets weakened by falling asset prices have the potential to constrain growth, as consumers may postpone purchases and businesses could defer investments until there is greater certainty.

-

Traditionally, growth risks would be met with more accommodative Fed policy. On the other hand, rising food and energy prices—alongside potentially broad trade disruptions—are likely to keep inflation elevated, potentially arguing for a faster pace of rate normalization.

Further Afield

-

European preliminary economic activity indicators for February point to a pick-up in growth which exceeded consensus expectations and suggest to us the impact of the omicron wave is waning in the UK and euro area.

-

The selloff in Chinese technology stocks resumed this week with the Hang Seng TECH Index falling to its lowest level since the gauge was introduced in mid-2020. Investors thinking the worst of China’s tech crackdown had passed were dealt a blow last week as new measures/developments—guidance on food delivery platforms, warnings against illegal fundraising schemes tied to the metaverse, and an inquiry into state-owned firms with exposure to Ant Financial—prompted a sharp drop in share prices.

Notes About Companies in Model Portfolio

-

Berkshire Hathaway (BRK.B) reported on Saturday operating results for the fourth quarter and full year of 2021 and 2020. Operating earnings per class B share calculated by dividing operating earnings of ~$7.29B by average equivalent Class B shares outstanding of ~2.23B. Approximately $6.9B was used to repurchase shares during Q4 bringing the total for the year to approximately $27B.

-

Canadian Apartment Properties Real Estate Investment Trust (CAR.UN) announced on Wednesday operating and financial results for the three months and year ended December 31, 2021. CAPREIT has maintained a very high level of rent collection, with over 99% of rents collected year to date. On turnovers, monthly residential rents for the year ended December 31, 2021 increased by 5.9% on 21.8% of the Canadian portfolio, compared to an increase of 7.9% on 18.7% of the Canadian portfolio for the year ended December 31, 2020.

-

Johnson & Johnson (JNJ) US Bankruptcy Judge Michael Kaplan refused to throw out a Chapter 11 petition filed by LTL Management LLC, the unit J&J set up to handle litigation related to personal injury claims from talc-containing baby powder. The ruling blocks most lawsuits filed by cancer victims as the company continues to negotiate a global settlement rather than fight each claim in court, individually, permitting J&J to continue with its controversial strategy of transferring baby power-related lawsuits to a business unit, LTL Management, specifically set up to handle such claims. The unit was then put into bankruptcy, effectively staying individually lawsuits and transferring them to the jurisdiction of the bankruptcy court, where ~$2B in assets is available to settle claims.

-

Royal Bank of Canada (RY) Thursday reported net income of $4.1 billion for the quarter ended January 31, 2022, up $248 million or 6% from the prior year, with strong diluted EPS growth of 7% over the same period. Personal & Commercial Banking and Wealth Management saw strong earnings growth, while robust Capital Markets results were down from record first quarter earnings last year. Investor & Treasury Services and Insurance results were also lower.

-

TD Bank Group (TD) and First Horizon announced that they have signed a definitive agreement for TD to acquire First Horizon in an all-cash transaction valued at $13.4B, or $25.00 for each common share of First Horizon.

-

The transaction is expected to be immediately accretive at closing to TD's adjusted EPS and over 10% accretive to 2023E adjusted EPS on a fully-synergized basis. TD expects to achieve approximately $610M in pre-tax cost synergies equal to 33% of First Horizon's 2023E non-interest expense through a combination of technology and systems consolidation, and other operational efficiencies.

-

TD will benefit from First Horizon's strong regional presence, including leadership positions in Tennessee and Louisiana, additional density in Florida, the Carolinas and Virginia, and important footholds in the attractive Atlanta, Georgia, and Dallas and Houston, Texas markets.

-

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman