Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday January 21, 2022.

| Equity Indices | Level | 1 week | YTD |

| S&P/TSX Composite | 20,621 | -3.5% | -2.8% |

| S&P 500 | 4,398 | -5.7% | -7.7% |

| NASDAQ | 13,769 | -7.5% | -12.0% |

| Euro Stoxx 50 | 4,230 | -1.6% | -1.6% |

| Hang Seng | 24,966 | 2.4% | 6.7% |

Source: Bloomberg, RBC Wealth Management

-

TSX finished lower Friday, just off worst levels. Energy, tech and materials the big laggards. Canadian equities posted a 3.5% weekly decline, with technology a notable laggard for third straight week (sector down 17% YTD). Gold ended down 0.6%. WTI crude settled down 0.5% but still posted fifth straight weekly gain. Canadian dollar lower against USD at $0.795 U.S. (or US$1.00 = $1.258).

-

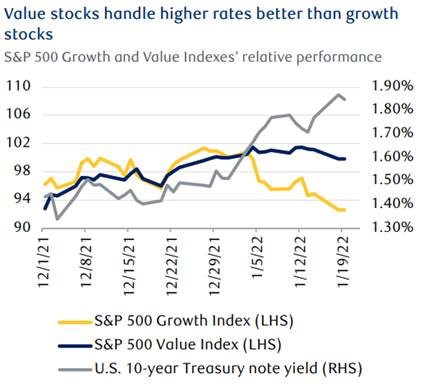

U.S. stocks continued their January slide during the holiday-shortened week as higher interest rates upset equities. Not all sectors were impacted equally; growth stocks, led by the higher-valued Technology sector, bore the brunt of the selloff while value sectors trod water (see chart). The downdraft tipped the tech-heavy Nasdaq Index into official correction territory, after it logged a 10% decline from its Nov. 19, 2021 high during the week.

-

Biggest headwind has been the velocity and magnitude of bond yield backup (driven by real yields) stemming from the Fed's hawkish policy shift. This shift, driven by concerns about more persistent inflation, initially revolved around an accelerated taper. However, it quickly intensified to include expectations for a March liftoff and four rate hikes this year, along with earlier and more aggressive balance sheet runoff (QT).

-

The volatility in bond and equity markets overshadowed the start of Q4 2021 earnings season. Analysts expected revenue and earnings per share growth of 13% y/y and 21% y/y for the quarter, according to consensus expectations at the start of the week.

Economy

Canada

-

The quarterly Business Outlook Survey from the Bank of Canada (BoC) painted a picture of an economy contending with mounting inflationary pressures and labour market tightness. Demand remains robust across most of the economy, but the number of firms indicating that their sales are being limited by supply constraints increased.

-

Inflationary pressures came into focus last week, with the December Consumer Price Index (CPI) report revealing Canadians are experiencing the largest yearly price increases in more than 30 years. CPI growth came in at 4.8% y/y, and among the biggest drivers were some of the most essential and hardest-to-avoid categories including transportation, food, and shelter.

U.S.

-

The yield on the U.S. 10-year Treasury bond jumped to 1.87% at the start of the week, its highest level since January 2020, as inflation concerns triggered hawkish rhetoric from Federal Reserve officials. Market indicators now suggest traders expect four 25 basis point interest rate hikes this year, although we note that actual year-on year inflation figures should peak during the first half of the year due to low base prices in the first half of 2021 and an improving supply of goods and labor.

Further Afield

-

Unlike most of the Western world that is trying to live with COVID-19 by imposing relatively light restrictions, and despite some 85 percent of its population being fully vaccinated, China is steadfast in pursuing its zero-tolerance policy of stopping community transmission through strict and swift containment measures. It recently locked down the city of Xi’an, home to 13 million people and a centre of semiconductor manufacturing. More cities, including Beijing, have also reported omicron cases in the past few days.

-

Many observers believe China’s zero-tolerance policy is destined to fail due to the emergence of the highly transmissible omicron variant, and eventually China will have no choice but to follow the path taken in the West. Our RBC Wealth Management analysts do not agree. They point out that due to China’s very large population, the unvaccinated 15 percent (totaling 210 million people) could easily overwhelm the health care system should a significant portion require emergency treatment. Moreover, research shows China’s vaccines are less effective against omicron than against previous variants.

-

Lockdown risks therefore continue to rise in China, even as they decline elsewhere. Increased pandemic restrictions could lead to additional supply chain disruptions, hold back the normalization of the global economy, and fuel global inflation, while capping Chinese economic growth.

Notes About Companies in Model Portfolio

-

Microsoft (MSFT) will acquire Activision Blizzard for $95.00 per share, in an all-cash transaction valued at $68.7B, inclusive of Activision Blizzard's net cash. Bobby Kotick will continue to serve as CEO of Activision Blizzard, and he and his team will maintain their focus on driving efforts to further strengthen the company's culture and accelerate business growth. Once the deal closes, the Activision Blizzard business will report to Phil Spencer, CEO, Microsoft Gaming. The acquisition also bolsters Microsoft's Game Pass portfolio with plans to launch Activision Blizzard games into Game Pass The deal is expected to close in FY23 and will be accretive to non-GAAP EPS upon close.

-

Procter & Gamble Company (PG) reported second quarter fiscal year 2022 net sales of $21.0 billion, an increase of six percent versus the prior year. P&G increased its outlook for adjusted free cash flow productivity to 95% and now expects to pay over $8B in dividends and repurchase $9-10B of common shares in FY2.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman