Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday January 14, 2022.

| Equity Indices | Level | 1 week | YTD |

| S&P/TSX Composite | 21,358 | 1.3% | 0.6% |

| S&P 500 | 4,663 | -0.3% | -2.2% |

| NASDAQ | 15,645 | -0.3% | -4.8% |

| Euro Stoxx 50 | 4,298 | -0.8% | -0.6% |

| Hang Seng | 24,383 | 3.8% | 4.2% |

Source: Bloomberg, RBC Wealth Management

-

TSX closed higher in volatile Friday afternoon trading. Sectors mixed led by energy with real estate and consumer staples the laggard. Canadian equities gained 1.3% on a weekly basis boosted by the energy and materials. Gold finished off 0.3%. WTI crude ended up 2.1%, gaining ~6.5% for the week. Canadian dollar lower against USD.

-

US equities were mixed in Friday trading, ending near best levels after a late afternoon rally. However, major averages all finished down for a second straight week. Semiconductors (particularly semicap equipment), Big Tech, energy, regional banks, casinos, aerospace/defense, HPC, food, tobacco, and hospitals outperformed. Money center banks, IBs, REITs, credit cards, retail, casual diners, airlines, coatings among the laggards. Treasuries weaker across the curve with 10-year yields back above 1.75%.

-

US equities down for a second straight week to start 2022. No one specific factor behind the pullback though Fed policy shift still seems to be reverberating, underpinned by an increasingly hawkish flurry of commentary from officials on both ends of the spectrum. December inflation prints no worse than feared but still elevated, fitting with the sticky price pressure narrative. Also more concerns about wage pressures, which have been flagged as a big risk to expectations for record profit margins in 2022.

-

While corporate commentary continued to highlight a solid demand backdrop and some signs Omicron peaking, Omicron impact on the supply side still a near-term headwind. Magnitude of bond yield backup seems to be a deterrent for credible bounce attempts in growth, while velocity of the move has negative spillover effects for broader market despite strategist commentary that stocks and yields can go higher together.

Economy

Canada

-

The Canadian labour market had a strong recovery throughout 2021, with full-year job growth at 886,000. The labour market remained firm ahead of the omicron wave, with the economy adding 55,000 jobs in December and the unemployment rate declining to 5.9%, which is just slightly above the pre-pandemic figure and around levels that are viewed as consistent with a healthy labour market.

-

The Bank of Canada (BoC) has been closely monitoring the labour market, which will be factored into its monetary policy decisions. With omicron’s impact on the labour market expected by policymakers to be temporary and inflation continuing to run above target, we believe the BoC will stay the course with its monetary tightening path, despite the possibility of a near-term rise in the unemployment rate.

U.S.

-

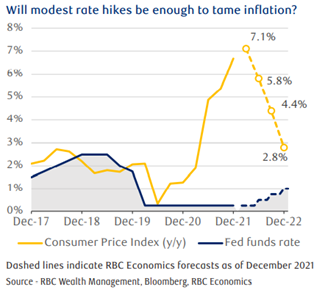

The big news of the week was, of course, inflation hitting seven percent on a year-over-year basis, according to the Consumer Price Index (CPI), the highest reading since 1982, and a level only seen as putting even more pressure on the Fed to act sooner rather than later.

-

As the chart shows, economists expect that the worst of the inflationary pressures are at least nearing an endpoint. Though inflation will likely continue to run north of seven percent on a year-over-year basis for the next couple of months, RBC Economics sees that pace slowing to 2.8 percent by the end of the year.

-

We envision a scenario where the Fed raises rates, but only to a certain point, before pausing as inflation cools, allowing for continued expansion and a full recovery of the labor market, particularly on the labor force participation front.

-

Prospects for additional fiscal stimulus in 2022 are uncertain, with key Senate Democrat Joe Manchin saying last week that negotiations on the Build Back Better Act had ended.

Further Afield

-

China’s total social financing growth in December picked up slightly to 10.3% y/y from 10.1% y/y in November. The People’s Bank of China’s underlying data shows a moderate easing in medium- to long-term loans to the household sector amid a recent relaxation in mortgage policy.

-

However, medium- to long-term loans to the corporate sector remained weak, which likely indicates that banks remain cautious in lending to property-related companies. We believe China’s overall macro policy stance will be neutral with an easing bias this year, but we do not expect a shift towards policy stimulus.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman