Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

Markets

Market scorecard as of close on Friday June 11, 2021.

| Equity Indices | Level | 1 week | YTD | 52-week |

| S&P/TSX Composite | 20,138 | 0.5% | 15.5% | 33.8% |

| S&P 500 | 4,247 | 0.4% | 13.1% | 41.5% |

| NASDAQ | 14,069 | 1.8% | 9.2% | 48.2% |

| Euro Stoxx 50 | 4,127 | 0.9% | 16.2% | 31.2% |

| Hang Seng | 28,842 | -0.3% | 5.9% | 17.8% |

Source: Bloomberg, RBC Wealth Management

-

Canadian equities rose 0.6% last week to a fresh record high led by health care, real estate and tech, while financial and consumer discretionary lagged. S&P 500, Nasdaq and Russell all finished higher last week. Growth outperformed value by more than 200 basis points.

-

Asian equities mixed in quiet overnight trading. Japan outperformed while Australia, Taiwan and Greater China markets were all closed.

-

Global markets are inching higher this morning after European and U.S. indexes ended last week at record levels.

-

Markets in waiting mode ahead of Wednesday's FOMC meeting. Lot of attention on the weekend's G7 summit. China flagged as a source of tension at the meeting. ECB's Lagarde said far too early to debate removal of stimulus.

-

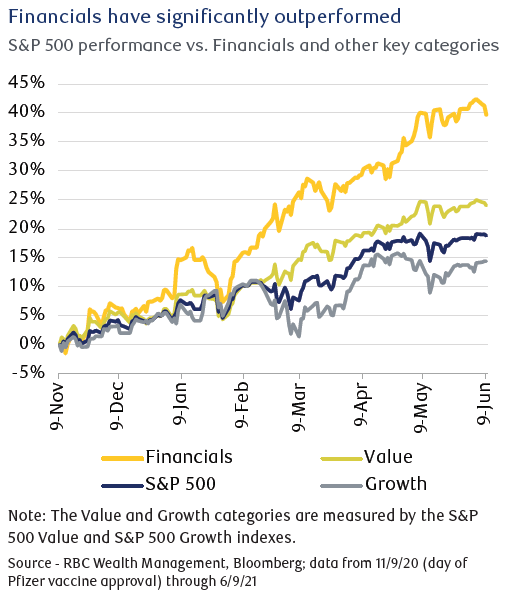

Financials have sprinted higher since late last year when the first vaccine was approved in the U.S., which prompted optimism about the eventual economic recovery—one that is now unfolding. This equity sector has significantly outperformed the overall market, surging 38 percent since early November 2020, double the S&P 500’s gain of 19 percent and outpacing all other sectors (excluding Energy).

-

Bonds rallied this week with yields on the 10-year Treasury declining below 1.5%, the lowest closing yield since early March. Fixed income demand was also helped by last week’s lackluster jobs report and a continuing lack of progress on infrastructure legislation.

Economy

Canada

-

The Bank of Canada’s (BOC’s) latest monetary policy announcement came and went largely as expected—uneventful. There were no changes to policy or forward guidance with the overnight rate remaining at 0.25% and the pace of quantitative easing (QE) purchases at CA$3 billion per week. The central bank still believes that sharply rising inflation will prove transitory in nature, expected to hover near 3% throughout the summer and then ease later in the year as “base-year effects diminish and excess capacity continues to exert downward pressure.”

-

The Canadian labour market slid for a second consecutive month in May, shedding 68,000 jobs, as reported by Statistics Canada. As lockdown restrictions begin to ease, spurred by declining case counts and increased vaccination rates, RBC Economics expects these latter industries [accommodation, food services, and retail] could begin recovering in June of this year. In all, the Canadian labour market remains approximately 571,000 jobs short of its pre-pandemic levels.

-

Canadian companies face supply-chain bottlenecks as the economy rebounds. According to the Globe and Mail, the economic recovery is leading to higher prices and narrower margins, at the detriment of Canadian companies. Commodity prices are approaching record levels, with the Bank of Canada’s commodity price index of 26 commodities reaching its highest level since 2014.

U.S.

-

Pension funds have been a beneficiary of rising equity and debt markets. Recent data from Milliman—an actuarial and pension consultancy—indicate that the 100 largest private pension funds are, in aggregate, nearly fully funded, with assets worth 98.8% of discounted future liabilities; the measure had been as low as 82% in July of last year.

-

These pension funds may serve as a source of future fixed income demand, as fund managers may look to add bonds to lock in recent gains and match investment cash flows with expected future pension obligations.

Further Afield

-

The next and final step of the UK’s planned reopening of its economy is in doubt, with it looking increasingly likely there will be a delay to the June 21 target date for a “full reopening” and removal of all outstanding social contact restrictions amid increasing cases of the Delta COVID-19 variant. Prime Minister Boris Johnson plans to announce the government’s final decision on Monday (June 14).

-

As widely expected, the European Central Bank (ECB) kept monetary policy unchanged, leaving the deposit rate at -0.5%. ECB projections for GDP growth were markedly increased for this year and next, to 4.6% and 4.7%, respectively, compared to the March forecasts of 4% for 2021 and 4.1% for 2022.

-

On June 9, the Biden administration revoked Trump-era bans on Chinese-owned apps, including TikTok and WeChat, but said it will conduct its own review of apps that may pose a risk to Americans’ personal data.

-

Japan Prime Minister Yoshihide Suga said he wants to finish inoculating citizens who are willing to receive a COVID-19 vaccine by October or November. Japan has given nearly 20 million first and second doses of vaccines. After a slow start, the pace of inoculations has picked up since May, and Japan has vaccinated about 11% of its population with at least one dose. Tokyo and other major urban areas are still under a state of emergency, which is set to run to June 20, though it could be extended.

Feel free to contact me with any questions and/or to discuss investment ideas.

I appreciate the opportunity to serve you and look forward to continuing to help you accomplish your long-term financial goals.

Regards,

Shiuman