Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2026 edition covers Market Review for the year 2025, some long-term themes that drive investments, and how to achieve a balanced approach to wealth and health. Shiuman’s Corner covers the books I read last year.

Markets

Market scorecard as of close on Friday February 27, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 34,340 | 1.5% | 8.3% |

| U.S. | S&P 500 | 6,879 | -0.4% | 0.5% |

| U.S. | NASDAQ | 22,668 | -1.0% | -2.5% |

| Europe/Asia | MSCI EAFE | 3,180 | 1.2% | 9.9% |

Source: FactSet

- TSX ended lower on Friday, near worst levels. Most sectors lower. Tech and financial the outsized decliners. Consumer discretionary, dragged by ATZ-CA and GRGD-CA, and health care other notable laggards. Real estate, industrials, and staples also down. Communications the best performer, led by QBR.B-CA. Energy and materials other outperformers. Utilities a moderate gainer. Canadian equities finish the week up 1.7%.

- US equities were lower in Friday trading, though ended just off best levels. Major indices capped off a lower weekly finish, while S&P and Nasdaq ended February with biggest monthly loss since Mar-25. However, breadth positive and equal weight (RSP) finished slightly higher. Big tech mostly lower with NVDA-US the biggest Mag 7 decliner.

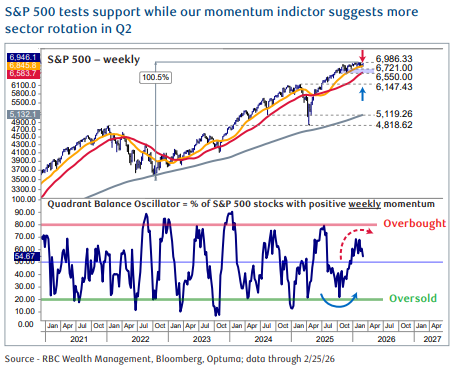

- Robert Sluymer, Technical Strategist, RBC Wealth Management:

- -The 2022–2026 bull market is mature but intact after a 100 percent rebound by the S&P 500 and 150 percent rally by the Nasdaq 100 from the Q4 2022 lows. While valuations remain a headwind, U.S. equity markets remain above key technical support levels with potential for another round of sector rotation developing heading into Q2.

-

-The bottom line is that we think it will be important for the megacap growth stocks that have either paused or pulled back since Q4 to begin stabilizing and rallying to keep the overall market cycle intact. While our expectation is that a rotation back to growth appears likely, an inability to do so would lead to the S&P 500 and Nasdaq 100 breaking below the key support levels highlighted above that we view to be useful downside risk control levels. A well-diversified portfolio remains prudent moving through 2026, which we continue to expect will be volatile consistent with the pattern of many U.S. midterm election years.

-

- ECONOMY

- Canada

- The Government of Canada released its Defence Industrial Strategy, outlining an ambitious CA$81.8 billion spending commitment over five years to rebuild and rearm the Canadian Armed Forces. These initiatives are projected by the Government to create high-paying jobs and add CA$6.1 billion to national income through research and development in advanced technologies.

- Canadian trade will be nearly unaffected following the U.S. Supreme Court’s ruling against the Trump administration’s broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA), according to RBC Economics. In December 2025, 89% of Canadian exports to the U.S. were exempt from tariffs because they were compliant with the Canada-United States-Mexico Agreement (CUSMA)

U.S.

- U.S. trade policy underwent structural changes last week following the U.S. Supreme Court’s ruling that the International Economic Emergency Powers Act (IEEPA) did not allow the president to impose tariffs. In response to the decision, which ended collection of most U.S. import taxes, the Trump administration announced a universal 10% tariff on essentially all imports, with an additional 5% applied “where appropriate,” according to U.S. Trade Representative Jamieson Greer.

- We expect the universal tariff to function as a bridge while the administration compiles the required reports and official findings to impose larger, longer-lasting tariffs under other legal authorities.

Further Afield

- EU lawmakers suspended approval procedures for the U.S. trade agreement negotiated last summer. The chair of the European Parliament’s trade committee, Bernd Lange, has asked for clarity on U.S. trade policy now that the U.S. Supreme Court has overruled the president’s use of the International Emergency Economic Powers Act to impose tariffs.

- China resumed activities this week after an extended nine-day Lunar New Year holiday. Travel data revealed robust tourism growth, with domestic traveler numbers and revenue rising 5.7% and 5.5% y/y, respectively, after adjusting for the longer holiday period. Beyond traditional tourist cities, lower-tier cities hosting cultural activities emerged as popular destinations.

Notes About Companies in Model Portfolio

- Element Fleet Management Corp. (TSX: EFN) the largest publicly traded, pure-play automotive fleet manager in the world, announced financial and operating results for the three months ended December 31, 2025 and for full-year 2025. The Company generated $1.2 billion in net revenue in 2025, an increase of $98 million or 9% from 2024 ("year-over-year"), supported by solid performance across all revenue categories. the Company generated $1.57 in diluted FCF per share in 2025, up $0.21 or 15% from $1.36 in 2024.

- Royal Bank (TSX & NYSE: RY) reported Thursday record net income of $5.8 billion for the quarter ended January 31, 2026, up $654 million or 13% from the prior year. Diluted EPS was $4.03, up 14% over the same period, reflecting higher results in Wealth Management, Personal Banking, Commercial Banking and Capital Markets, partially offset by lower results in Insurance. Adjusted diluted EPS of $4.08 was up 13% from the prior year.

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.