Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q4 2025 edition covers Market Review up to Q3 of 2025, the Artificial Intelligence (AI) boom and gold’s surge. Shiuman’s Corner is a about my cycling adventures for fund raising. The latest 2026 Q1 Smart Investor will be published this week!

Markets

Market scorecard as of close on Friday January 16, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 33,041 | 1.3% | 4.2% |

| U.S. | S&P 500 | 6,940 | -0.4% | 1.4% |

| U.S. | NASDAQ | 23,515 | -0.7% | 1.2% |

| Europe/Asia | MSCI EAFE | 2,992 | 1.4% | 3.4% |

Source: FactSet

- TSX finished little changed in Friday afternoon trading. Sectors mixed. Energy the outsized gainer. Canadian equities ended the week up 1.3% lifted by materials strength and energy rebound.

- US equities were mostly lower in Friday trading, though downside very limited. Friday’s uneventful session capped off a week of modest declines for the S&P 500 and Nasdaq, though small-cap R2K tracking posted solid weekly gain (and outperformed S&P for eleventh straight session, longest run since the 90s). Breadth negative and equal-weight S&P lagged cap-weighted index.

- Markets have entered the new year digesting a steady stream of headlines, underscoring the importance of staying focused on fundamentals. The year has begun with heightened geopolitical activity, led by U.S. actions in Venezuela alongside renewed tensions involving Iran and Greenland.

- Corporate fundamentals remain constructive. Forward earnings expectations across major markets continue to trend upwards, and the U.S. Q4 2025 earnings season began this week, with analysts expecting high-single-digit earnings growth for the S&P 500 Index. More broadly, after approximately 12% global earnings growth in 2025, consensus expectations point to a further 14% increase in 2026.

ECONOMY

Canada

- Prime Minister Mark Carney announced Canada and China reached a preliminary joint agreement on addressing bilateral economic and trade issues. Canada to lower tariffs on Chinese EV from 100% down to 6.1% for the first 49,000 vehicles. In return China to cut tariffs on canola seed to approximately 15% from current levels of 84%.

- Canada’s labour market is experiencing a structural shift as population growth pauses following surges in 2023–2024. The breakeven employment rate, the estimated pace of job creation needed to prevent the unemployment rate from rising, has declined sharply.

- We believe this shift in Canada’s labour market dynamics means modest job losses—which would normally be expected to contribute to a rising unemployment rate—could instead result in a stable or declining unemployment rate in the future.

U.S.

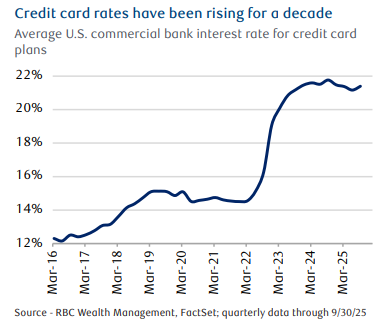

- President Donald Trump’s proposal to cap credit card rates at 10% is framed as an attempt to lower borrowing costs for households and businesses. However, we believe caps on credit card rates would negatively affect profit margins at lending and credit card firms. A rate cap may push borrowers with low credit scores out of the lending pool and could limit available credit for others, potentially driving up rates for this cohort.

Further Afield

- The UK economy defied expectations in November, with GDP rising 0.3% month-over-month, reversing October’s 0.1% contraction and surpassing both our economists’ forecast of flat growth and the 0.1% growth consensus estimate.

- The sharp moves in Japanese equities came after Kyodo News reported that Prime Minister Sanae Takaichi told a senior member of her ruling Liberal Democratic Party (LDP) that she intends to call a snap election. With the prime minister’s approval rating running high, we believe a snap election could help the LDP expand its thin majority in the lower house of Parliament, making Takaichi’s expansionary policies more likely to pass.

Notes About Companies in Model Portfolio

- Quarterly earnings kicked off last week, starting with major U.S. banks. To round out fiscal 2025, three of the four largest U.S. banks reported what we view to be broadly positive earnings, driven by continued net interest income growth, as well as better loan loss provisions and credit quality. Forward estimates by the street were revised upward, but large banks are down this week due to the Trump administration’s proposal to cap credit card rates.

- The Procter & Gamble Company (NYSE:PG) declared a quarterly dividend of $1.0568 per share on the Common Stock. P&G has been paying a dividend for 135 consecutive years since its incorporation in 1890 and has increased its dividend for 69 consecutive years.

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.