- U.S. government debt has been rising rapidly since the global financial crisis, but broader measures of borrowing across the economy have remained relatively stable and on par with other developed economies.

- U.S. fiscal policy is likely already unsustainable, with politically sensitive programs costing more than current taxes generate.

- Higher inflation—not default or foreign coercion—is the likely trigger for the U.S. to put its budgetary house in order.

The U.S. debt has always been a divisive matter. Not only is there disagreement on its causes and fixes, but no one can seem to agree if, or when, the federal debt becomes a concern.

Both sides of the argument have a problem, in our view. Folks saying that the amount of U.S. borrowing will lead to a calamity have to deal with a 40-year track record of being wrong, the counter-example of the Japanese economy functioning with debt levels nearly twice that of the U.S. today, and the fact that no sovereign has defaulted when borrowings are exclusively in its own fiat currency under its own law.

For those saying the debt is irrelevant, the path is no easier. The major stumbling block is the apparent absurdity of their argument: somehow, somewhere it must matter how much money we have borrowed to fund our current spending. After all, “there is no such thing as a free lunch” is not a bad starting premise for the study of economics.

Our view is between these two extremes. We believe the federal debt—in and of itself—is a manageable concern and that the U.S. is nowhere near a default risk. At the same time, we think that the conditions that created the debt—which are ongoing—are problematic and will impose future costs on the economy.

Got debt? Sort of

Before turning to fiscal policy, which we see as the real issue, it’s worth diving into the federal debt given how much press it gets. And it gets that level of attention for good reason—the federal government owes a gob smacking amount of money. Even without considering the debt to various government trust funds, the Treasury has borrowed nearly $28 trillion dollars, or just under 100% of Gross Domestic Product (GDP). If Social Security and similar obligations are included, the total is easily above $33 trillion. Statistics like these seem to lend credence to the view that U.S. debt is out of control.

What’s odd to us, though, is the laser-like focus on the federal government’s borrowing. After all, most economic activity in the U.S. takes place outside the government and is instead the product of corporate and household activity. When we broaden out our perspective to include these sectors, the debt position of the U.S. as a country—not just a government—looks very different.

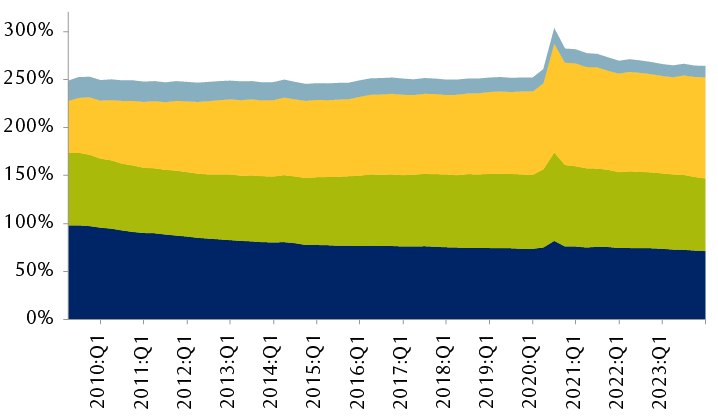

First, there has been no appreciable recent run-up in national borrowing. Aside from a COVID-19-related blip, the overall debt-to-GDP ratio has been remarkably stable over the past 15 years. There have certainly been changes in the composition of U.S. borrowing, but the amount of debt has grown at roughly the same pace as the economy overall for over a decade.

Far from exploding, U.S. debt has been boringly consistent for 15 years

Total nonfinancial debt as percentage of U.S. GDP

The chart shows total U.S. nonfinancial debt as a percentage of gross domestic product (GDP) quarterly from 2010 through 2023. Debt is broken down into four categories: (1) households and nonprofits; (2) nonfinancial businesses; (3) the federal government; (4) state and local governments. Together, these categories totaled roughly 249% of GDP in 2010 and roughly 265% of GDP at the end of 2023. The relative proportions of each category have been generally stable over the period shown. All categories showed a sharp rise in 2020 and a subsequent decrease, although federal debt has remained elevated relative to its historical level.

Source - U.S. Federal Reserve; quarterly data through 2023

Nor does the U.S. debt burden look particularly troublesome compared to other large, developed countries. The combined debt load across U.S. corporations, households, and government entities was around 260% at the end of 2022, the last year for which International Monetary Fund stats are available. This puts the U.S. essentially at the median debt level for large, developed economies.

Put differently, if the U.S. were to dedicate its entire annual production to debt repayment, it would take about 2.6 years to wipe out all the money that households, businesses, and government entities have borrowed. That’s essentially the same timeline faced by the UK or Sweden, and it’s substantially less than Canada, where every dollar of productivity capacity has the burden of more than $3 of debt outstanding.

In fact, when we look at U.S. borrowing, what stands out to us is not the amount but the composition of its debt. More than most other countries, it’s the federal government that has borrowed against national assets, not private individuals or businesses.

A broader measure of indebtedness shows the U.S. is fairly typical

Debt as percentage of 2022 national GDP

The column chart shows debt in 2022 as a percentage of national gross domestic product (GDP) for eight countries (ordered from least to most total debt): Germany (194% of GDP), Ireland (219%), the United Kingdom (252%), Italy (254%), China (272%), the United States (273%), Sweden (274%), and Canada (322%). Debt is broken down into categories of general government debt, household debt, and nonfinancial corporate debt.

Source - International Monetary Fund; includes bonds, loans, and debt securities

There’s a lot to like, we think, about that debt profile.

To start, it’s the cheapest way to borrow. As a nation, the U.S. dedicates fewer resources to financing costs than if households or businesses had taken on loans. In addition, the federal government is not—yet—forced to belt-tighten when interest rates move up. This is different from, say, Canadian households that are feeling the pinch from higher mortgage costs, with negative, economy-wide implications.

Viewed across the entire economy, the U.S. has constructed a borrowing profile that is reasonable for the size of its economy and has a relatively advantageous borrowing structure, in our view. Far from being an albatross, federal debt is a potential advantage relative to the alternative of household or corporate leverage.

At least drunken sailors pay cash

While we believe that the federal government is the best positioned entity to carry a high debt burden, it is perhaps the worst entity at deciding whether additional borrowing is worthwhile. Households and corporations typically have a plan on how to repay any new borrowing, if only because lenders demand one. The federal government, by contrast, is never asked for a long-term repayment plan—not by bond buyers or voters.

It’s important to be clear that the debt is not a partisan creation. Politicians of all stripes pay lip service to fiscal restraint, but when in office both parties keep taxes well below the level of spending.

Part of the reason is voting math. Since at least the 1980s, there have been a few budget items that are electoral third rails—touching them is political death: The big three are Social Security; Medicare/Medicaid; and, to a lesser extent, defense. Combined, these “must fund” activities now exceed the federal government’s tax receipts. Interest expense on existing debt is an increasingly important addition to this required annual outflow.

When uncuttable spending meets unraisable taxes, the budget math can’t add up

2023 U.S. revenue and expenditures by budget category ($ billions)

The chart shows the disposition of U.S. tax receipts by budget category for fiscal year 2023. Starting with tax receipts of $4,440 billion, $2,594 billion is subtracted for Medicare and health, $1,438 billion for Social Security, $1,297 billion for national defense, and $905 billion for net interest payments, resulting in a negative balance of $1,794 billion.

Source - U.S. Treasury Department, RBC Wealth Management; data for fiscal year 2023

Against that backdrop, we think it’s almost a given that the debt is going to continue to grow for the foreseeable future. In our view, it’s unrealistic to expect politicians to meaningfully raise taxes or cut popular programs without some sort of external impetus.

In theory, that could come from the electorate. Survey data shows a high degree of voter concern on the federal debt. When asked, however, about their willingness to accept higher personal taxes or reduced benefits, voters quickly change their tune. Support for debt reduction only lasts as long as someone else pays. Politics is the art of the possible, and balancing the budget without shared sacrifice strikes us as effectively impossible.

You want us in that mall, you need us in that mall

An alternate argument is that lenders will prompt fiscal retrenchment by pulling back from Treasury bonds. We see that as extremely unlikely.

In our view, simple self-interest decides the issue. The U.S. is the world’s consumer, and both foreign and domestic producers need Americans to buy their products. Even those companies that don’t directly sell in the country would almost certainly feel the impact of a U.S. economic contraction.

The current level of U.S. consumption is only possible because of credit, and it is in the producers’ self-interest to recycle at least some of their earnings into continued lending.

The dynamic is easiest to see when looking at overseas actors. Foreign countries often buy U.S. dollars to gain a currency advantage for their exports, which results in a need to invest those dollars in low-risk assets such as Treasury bonds. Those bond purchases then give the U.S. government the needed resources to continue spending beyond its means.

Another way to think about the lending/selling dynamic is to look at the history of the car industry. The rise of the automobile finance corporation did not come about because car manufacturers were drawn to the consumer loan business; it was instead the realization that without credit, car demand evaporated and the producer, ultimately, suffered.

Not with a bang but a whimper

Our view, then, is that we should expect the budget deficit to remain and probably grow, with federal debt increasing for the foreseeable future.

The process will inevitably end, and we see the inflationary impact of budget deficits as the most likely catalyst for change. Put simply, when the U.S. government spends more than it taxes, it adds to near-term demand, which is likely to be inflationary.

For the past several decades, the potential price consequences of government borrowing were, we believe, largely offset by other factors: growing low-cost supply from China, the deflationary consequences of the global financial crisis, and declines in household borrowing. These factors, we believe, are largely played out, potentially leading to more visible inflation from deficit financing.

That, we think, is good news for fiscal rationality. One of the key takeaways from the past two years, we would argue, is that inflation is intolerable across most sectors of U.S. society. While we think it’s a utopian belief that voters will wake up one day and decide to belt-tighten to help their grandchildren, we see a relatively easy link between rising prices and consumer anger.

Regardless of what sparks the shift toward fiscal balance, our view is that the resolution is likely to be painful, but manageable. It will almost certainly come from a combination of cutting government spending and benefits, increasing taxes, and allowing higher inflation to reduce some of the real cost of repayment. The outcome of these adjustments is very likely to be negative for global growth, creating a headwind for all sectors of society, including workers, taxpayers, and investors.

In essence, we are saying that neither households nor corporations are quite as well-off today as they think they are. At a certain point, some of what is currently private wealth will need to be used to pay down national borrowings. That process will be a headwind for prosperity, and one that grows in strength every year, but it is also part of the normal cycles of change in a dynamic economy. After all, government borrowing taking place today is helping create private wealth through economic growth and investment gains.

Reasons for optimism

“Predictions,” according to a Danish proverb, “are difficult, especially about the future.” The further in advance, the larger the likely error. “Catastrophizing” over long-term debt estimates ignores this reality and the history of prior failed projections.

Take the 2010s, for instance. If there was a prevailing theme to budget discussions at that time, it was rising healthcare costs and how Medicare spending would pressure the U.S. Treasury beyond control. Fast forward 10 years and Medicare costs per beneficiary were stable for a decade. The root causes of the improvement are still debated, but the beneficial financial consequences amount to nearly $4 trillion since 2011, according to an analysis published in Health Affairs.

Artificial intelligence (AI) and technology in general are obvious potential positive factors for the federal budget, in our opinion. The impact is two-fold, with rising prosperity increasing tax contributions and more efficient, technology-enabled operations reducing costs. Just as the internet helped transform the provision of government services, we think it would be foolish to rule out the possibility of an AI-induced budget fillip.

The simple reality is that not all uncertain outcomes turn out to be unfavorable.

Extreme outcomes extremely unlikely

Our view of high debt creating future growth headwinds is common in economic textbooks, but less frequently found in the popular press, who instead put forward theories of a bankrupt Treasury failing to make payments or the risk of China using its bond holdings to exert influence or control over U.S. policy.

We think these risks are vastly overstated and overlook three key realities.

First, the federal government is not a typical borrower. Its debt is issued in its own currency under its own law, giving it debt management tools such as taxing interest payments or forcing the Fed to buy bonds through money printing. These are not costless—they would come with inflation or difficulty selling bonds in the future—but they’re not even on the table for other debtors.

Second, a U.S. default would be a global economic catastrophe. There were $600 billion in subprime mortgages outstanding in 2006, and they managed to throw the global economy into a recession that took years for recovery; Treasuries have nearly 50x that amount outstanding. A U.S. default would almost inevitably throw the U.S. and the world into a severe recession and eviscerate bank capital globally. There would be, in our view, no winners, only varying degrees of losing.

Third, default is not currently a viable option for creditors. U.S. solvency is not an immutable law of nature; we accept that default is a possibility. But for a default to be a realistic alternative, there would have to be sufficient non-U.S. demand to allow for a deep and severe U.S. recession without it tipping into a global recession. In addition, there would have to be an asset that replaces Treasuries as the dominant source of inter-bank collateral. Until that happens, we think creditor self-interest argues against a default.

For these reasons, we also reject the idea that China—or any other nation—can realistically use its bond holdings for geopolitical advantage. It would be economically disastrous for whatever nation pulled its cash, and it would be unlikely to work in practice, as the U.S. can legally use its sovereign authority to cushion any blow.

More fundamentally, we think this argument reverses where power lies in the lending relationship. The U.S. has already received goods and services from China and paid for them with over a trillion dollars in IOUs. China, we would argue, is the one exposed to geopolitical risk in this scenario, not vice versa.

Debate, discussion, and debt

The so-called debate on the federal debt often seems to be a choice between hyperbolic claims of imminent collapse and a Panglossian view that no matter the amount, the debt is not a concern.

We believe that is a false dichotomy. In our view, the current level of debt will not lead to a default but will likely impose eventual economic costs in the form of lower growth, reduced government benefits, higher taxes, and higher inflation. If, as we project, deficits continue and the debt burden grows, then the eventual resolution will take longer and weigh more on the economy than if it were addressed sooner.