Since my last update regarding market volatility and the tilting of the Yield Curve, I've had the opportunity to listen to Jim Allworth, RBC's Chief Strategist on three occasions: two times at conferences I have attended, and once at a client event I hosted for Hamilton business owners.

I have Jim's fall strategy for anyone that is interested, and he will have an update in the coming weeks which we will send out.

In essence Jim's message is that though indications are that the market will continue to rise, the economy is slowing and it would be prudent as investors to be cautious. There is now a greater chance that a shock, such as a political event or an escalation in trade tension, could hasten the drop in growth and push us into recession.

The Yield Curve: This time it's different?

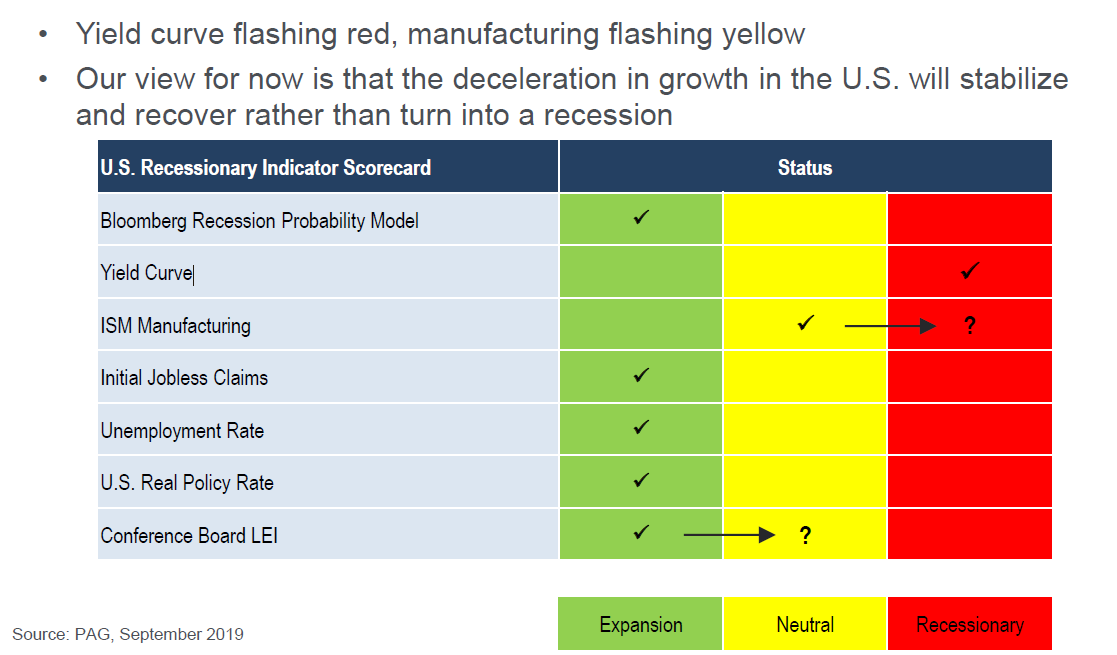

Jim references 6 leading indicators the Portfolio Advisory Group follows. For the first time in 10 years, some of these have changed from green to yellow and red.

The inversion of the yield curve refers to the fact that Long Term Interest rates on US Government Bonds have dropped below Short Term rates. These bond rates have a direct impact on lending rates, and as short term rates go up quickly surpassing the long term rates, Banks are less likely to lend money to businesses. Businesses that have difficulty borrowing money employ less people, and we thus have the beginning of the cascading effects of a recession.

This indicator has been a very accurate description of a pending recession. There is however great debate about the circumstances this time. In the past, the inversion has happened because short term rates have risen faster than long term rates and ultimately surpassed them, usually in an effort from the Central bank to curb inflation. This time however rates are extremely low, and the inversion occurred because long term rates have fallen, not short term rates rising.

Why has this occurred? Japan and parts of Europe are offering negative interest rates: Many of you will know this, but if you hold deposits in a savings account in some of these countries, the bank will actually debit the balance as it sits there. The drop in US long term rates has come because residents of these countries have started to move large amounts of savings into US Long term Bonds, thus driving those rates down.

So the argument goes that rates are low, and banks are still eager to lend money, so this inversion is different and should not be heeded.

This is where Jim says all this is true and compelling, but he is very reluctant to jump onto the "this time it's different" argument. Perhaps this is a self-fulfilling prophecy, and even though rates are low and and credit is not "tight", this will in fact incentivize banks to lend less money for different reasons.

Though we feel markets will most likely continue to rise, signs are pointing to a slow down. Markets have a tendency to peek on average 6 months prior to a recession commencing. To add to the that, the market peak is typically led by a handful of companies- not a broad market rise. The ability to pick those handful of names has more luck involved than skill. This is risk to an investor.

All these factors lead us to the conclusion that we should be cautious in our investment selection. It is a time to trim and rebalance and have a market neutral approach.