The most striking trend that emerged in recent months has been the return of sellers to the housing market. September was a case in point where new listings increased sequentially in all major markets (for which early reports from local real estate boards are available). The factors driving this trend are many but soaring interest costs no doubt are prompting a growing number of owners to move.

High interest rates at the same time dampen demand. Home resales are now weakening in British Columbia and Ontario—though Calgary continues to stand out for its vigour. Growing supply and cooling demand have significantly reduced earlier market tensions. Conditions in several markets—including Vancouver, the Fraser Valley and Toronto—have in fact tilted in buyers’ favour.

Indeed, this shift has led to small price declines. The MLS Home Price Index fell slightly month-over-month in Vancouver, the Fraser Valley and Toronto in both August and September. The Index continued to climb in Calgary where demand-supply conditions remain very tight.

We expect little change in this broad picture in the months ahead. We think buyers will stay on the defensive in many parts of Canada despite more choice becoming available to them. High interest rates, ongoing affordability issues and a looming recession are poised to pose major obstacles. Any material acceleration in the market recovery will have to wait until interest rates come down in 2024.

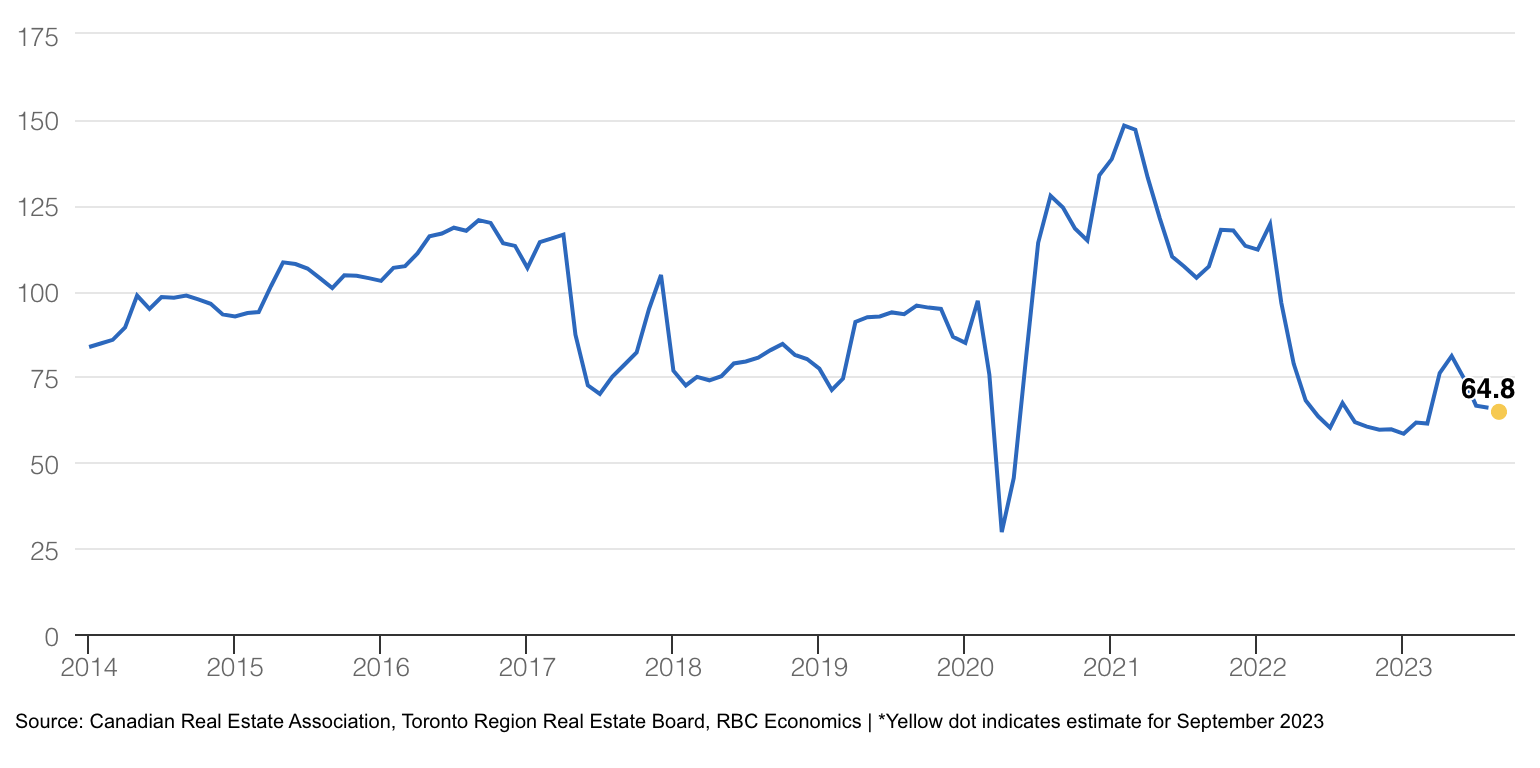

Toronto area—Market balance tipping in buyers’ favour

Frustrated by low inventories earlier this year, buyers now have more options to choose from as sellers make their way back to market. September marked the sixth consecutive month new listings have increased in the Toronto area—this time rising by a solid 11.0% m/m. But that hasn’t sparked the release of pent-up demand. Home resales continued to slide in September, down 1.8% m/m. High interest rates, poor affordability and growing economic uncertainty pose serious obstacles for buyers at this point. A sharp loosening in demand-supply conditions over the past four months is now cooling prices down. The MLS HPI edged lower in both August (-0.2% m/m and September (-0.8%). We expect further erosion in the near term with buyers holding a stronger bargaining position.

Toronto-area home resales

Thousand units, seasonally adjusted annual rate

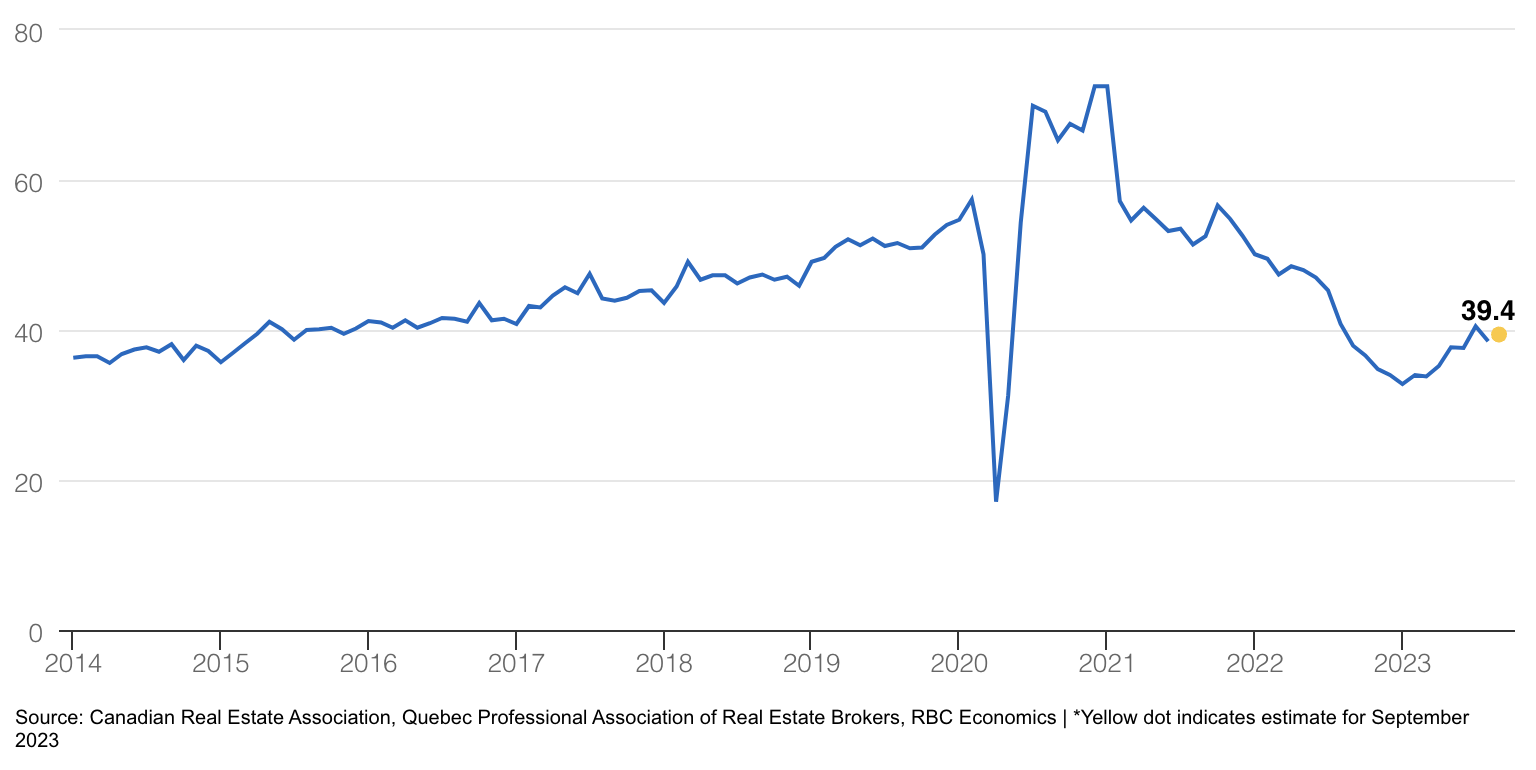

Montreal area—Opposing forces keep recovery subdued

Market activity remains quiet but continues to gradually recover from last year’s sharp correction. Home resales are up 8.9% from the (low) level in September 2022, and more than 2% from August 2023 (by our own seasonally-adjusted estimate). Two forces are at play: on one side, an influx of sellers since spring has helped unlock some pent-up demand; on the other, higher interest rates have made it more difficult for buyers to afford a home purchase—muting momentum. The balance between demand and supply has eased, which keeps prices largely level overall (with pressure varying by segment and sub-areas). The median price for a condo apartment in the Montreal region rose 2.3% m/m in September, whereas it fell 2.1% for a single-family home. Prices in both segments were up slightly from year-ago levels. The outlook calls for more of the same in the coming months.

Montreal-area home resales

Thousand units, seasonally adjusted annual rate

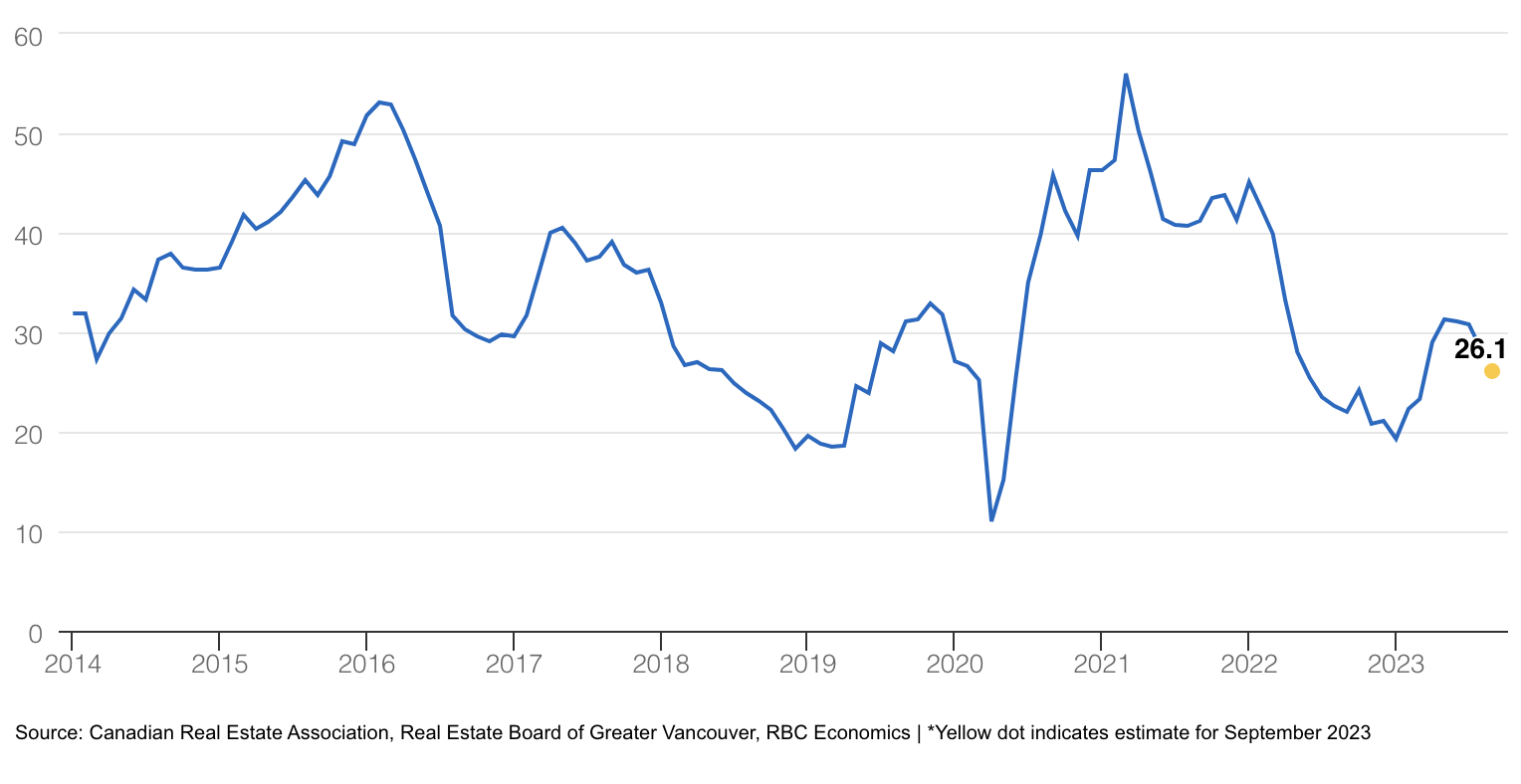

Vancouver area—Softening fast

What a difference three months make. Since June, demand-supply conditions in the Vancouver area have gone from firm to borderline soft, thanks in part to a string of sizable increases in homes put up for sale (including a hefty one in September). Buyers have also become more cautious amid high interest rates and crisis-level affordability. The upshot of this rapid shift has been an end to the price rally that began this winter. The MLS HPI for Vancouver slipped in both August and September, down 0.2% m/m and 0.4%, respectively. With new listings back above pre-pandemic levels and inventories trending higher, prices are likely to stay on a slight downward trajectory in the near term.

Vancouver-area home resales

Thousand units, seasonally adjusted annual rate

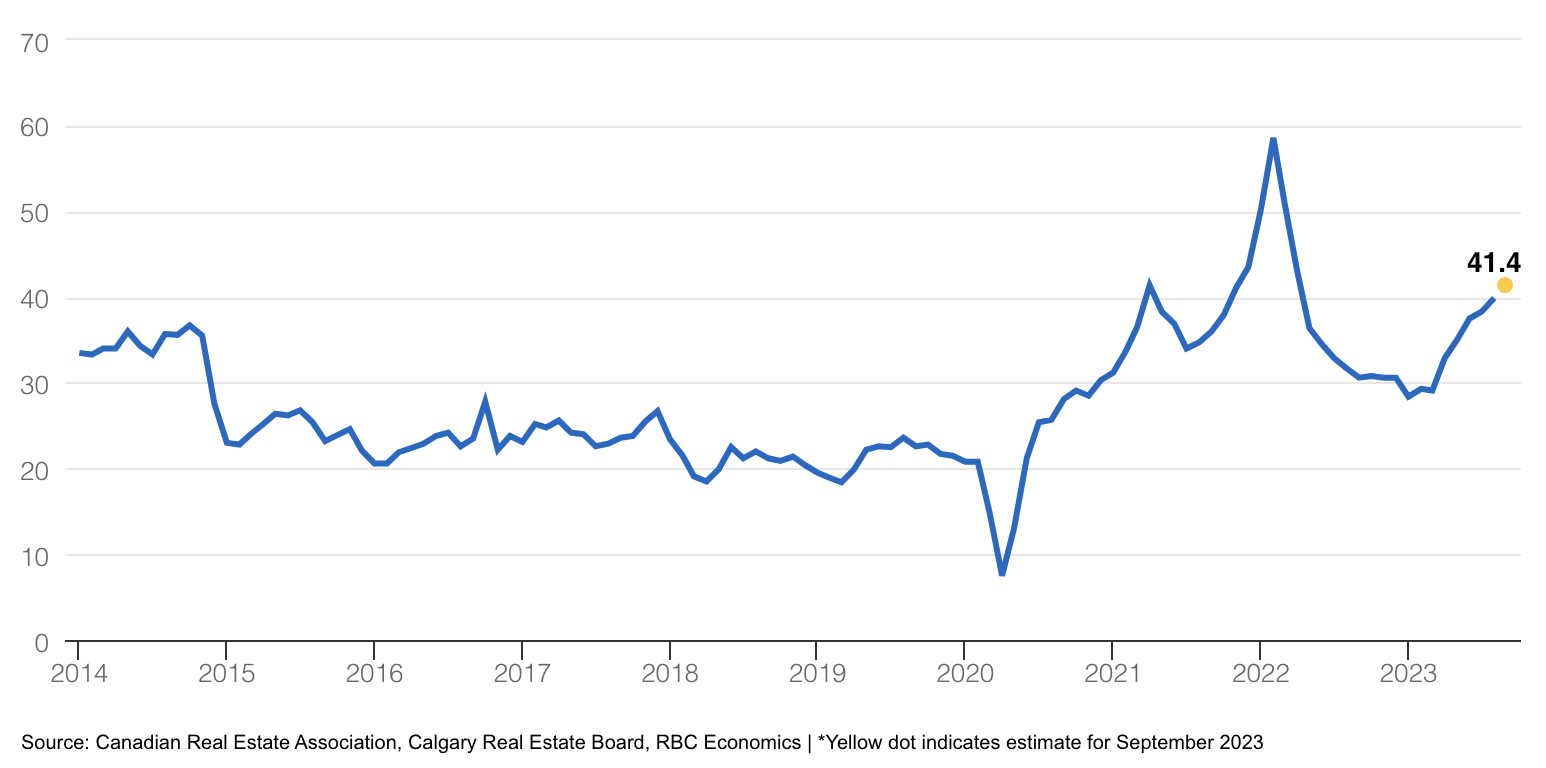

Calgary— All abuzz

Explosive population growth and lower ownership costs than in BC and Ontario are generating a lot of buzz in Calgary’s market. This is attracting droves of buyers, and driving up real estate transactions and prices to historical highs. Home resales rose for the sixth-straight month in September (up an estimated 4% m/m). Supply—while growing steadily—continues to lag demand, keeping the market highly competitive for buyers. Calgary is easily the tightest (and hottest) market in Canada at the moment. It’s not a surprise then that its MLS HPI has increased the most over the past year (up 8.7%) among the country’s larger markets. We think upward price pressure isn’t about to let up anytime soon.

Calgary-area home resales

Thousand units, seasonally adjusted annual rate

See PDF with complete charts

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.