“Bad Medicine”

Each era of financial extremes has its poster-children of “money gone wild.” In the time I have been in the financial industry the list would look something like this:

1985/1987 – Leveraged buyouts (LBOs)

2000/2001 – Technology stocks

2007/2008 – Real estate, mortgage debt

2020/2021 – “Everything bubble”, centered in government bond bubble.

Of course, the bubble in government bonds facilitated the bubbles in everything else. The COVID-19 response by governments and central banks extended the bubble’s life and magnified the size to which it grew.

I need each reader to hold up right here.

Do you agree with what I just wrote? Do you agree strongly, mildly, or totally disagree?

Honestly, I’m not looking for you to nod your head and tell me I’m right. As a matter of fact, I really hope I’m wrong. But I need you to decide if you believe the world is in an “everything bubble.”

The Everything Bubble refers to believing interest rates have been suppressed to virtually zero around the world every asset class is relatively to very expensive.

To the extent you agree with this statement dictates how strong of defensive position your portfolio will gravitate to IF the “everything bubble” starts to decay, which may be happening now.

I have three stop losses in place at the moment. Two were breached Monday, September 21st.

Canadian TSX Index – 15,800 level

US S&P 500 – 3150 level

Gold bullion USD - $1900

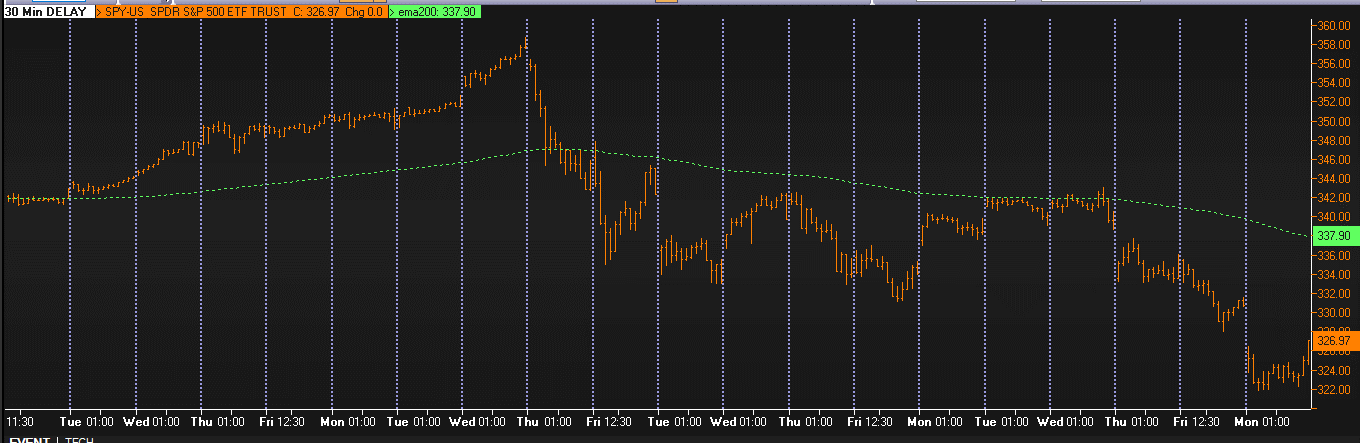

I wanted to lead with a concise look of financial markets because it sums up what I have been saying in so many more words for the past few weeks.

Take a look at the 30 day chart below of the S&P 500. You do not need to be a graduated technical analyst to see how it is trading differently since it made a top a couple weeks ago. Much choppier and making a series of lower highs and lower lows…so far.

The largest difficulty investors face this cycle is, when they choose to sell to cash, their money earns virtually zero return.

Because of this difficulty, many don’t want to take much action in reducing equity exposure.

Fair enough, but now is the time to consider risk reduction not down 20% if that happens.

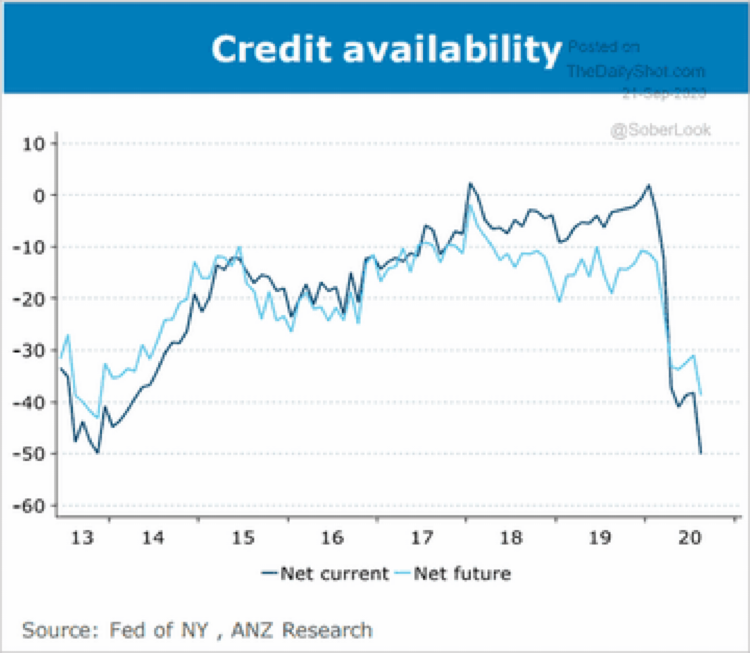

The US political climate continues to spin out of control. Ruth Bader Ginsburg’s passing and the process of replacing her on the US Supreme Court makes for a poor environment for cooperation on a stimulus package. Financial markets were hoping for more free money.

When the people don’t get free money from the government they can’t depend on the banks to lend either. The chart below depicts the shocking drop in credit availability that has accompanied the 2020 recession.

Last week I showed a chart of how the Fed has turned the money taps off again. Right about where the stock market started to flounder. Money is getting tighter after being spread around by a Fed-fueled fire hose earlier.

As we all know, this can change with the stroke of a pen, but for now be aware things have gotten more BEARISH and invest accordingly.

SPACs

Leading off this editorial, I featured the main bubbles of each financial mania since 1987. Behind each bubble, there were sub-bubbles.

For example, the mortgage collapse of 2008, featured the collateralized mortgages and debt obligation products featured in “The Big Short” book/movie.

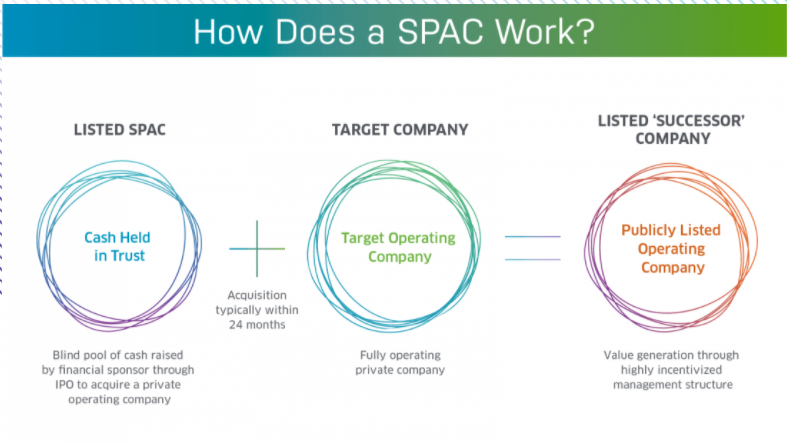

Well, 2020 has its own version of collateralized loans and mortgages and they are called SPACs.

Special Purpose Acquisition Companies (SPAC) have become a sight to behold and may be one of the highlighted areas of analysis in this bubble’s aftermath.

The easiest way to understand the concept of a SPAC is to see its purpose. The SPAC makes it easier (less scrutiny and red tape) for an early stage company to go public.

When the financial markets are bubbly everyone wants their Initial Public Offering done as fast as possible to cash in on the euphoria. SPACs allow this to happen.

Often these companies purchased by SPACs are only ideas. Not only do they have no earnings…they often have no sales either.

This is not a comment on “good” or “bad”. This is a comment on “where we are in the financial market cycle.” SPACs are not popular when markets are boring.

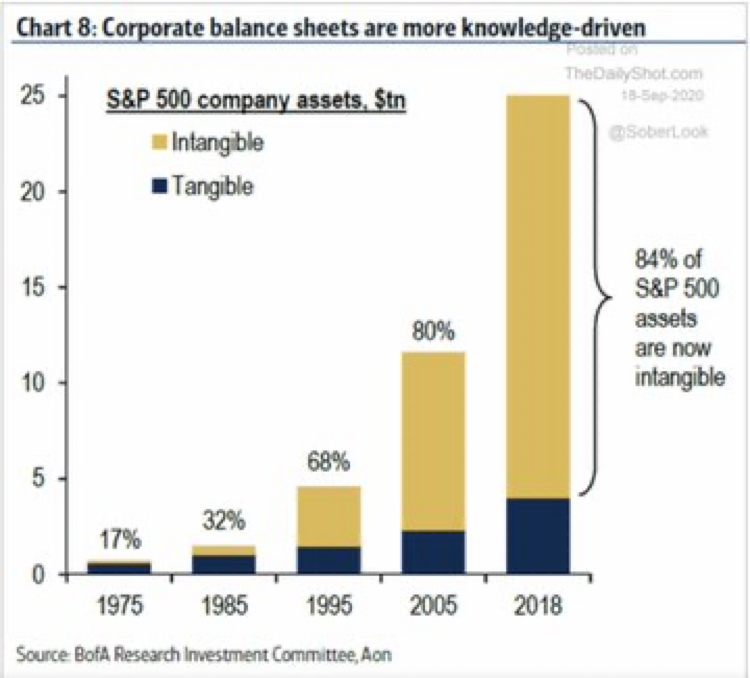

One other image I will leave you with is the following graphic.

Imagine, 84% of corporate assets are intangible. No wonder why it is difficult to evaluate companies on traditional metrics. It also makes sense why AMAZON or TESLA can be valued so radically different in a short period of time.

Tying this together with SPACs, it has never been more profitable to have a great idea. People will pay not only for what has PROVEN to be profitable, but for an idea that might just create sales.

This is just another sign of a bubble economy and cheap money.

And with that we count down another week looking out to the US election.

Please share your comments and feedback, and have a great rest of your week.