A Plan to Play Offense

There was a time when staying informed to the business news could be done by reading a reputable newspaper once a day.

To be fair, one can still do this if the goal is to just stay informed, but as the world moved faster and markets became more complicated, more up-to-date news flow was required.

Business television was the next step. A continual stream of comments came at the viewer that were much more aligned to real time than the newspaper was.

Unfortunately, business television became a grandstand for influential people to “talk their own book” to the point that only one in ten interviews was really worth listening to. Not to mention the political spin, which overtook business television making it less informative too.

Now we have media choices like Twitter, ZeroHedge, RealVision, and a host of others that we can personally control the flow of information. The negative part of this process is that we usually control the information flow to suit our own opinions.

That’s why I loved this headline from back in March.

In times of turmoil, maybe this is closer to the truth; who knows?

So if the Pros don’t know what is going on what good are they to you?

As investors, we must have a plan and a process.

- The Plan should be your personalized set of goals and objectives.

- The Process must be robust and consistent no matter the market conditions.

Let me outline my process:

- Overall valuation is the over-riding key to asset mix. The more expensive an asset class is, the less I want to own of it.

- Technical overlay dictates medium term exposure. Using charts to give a disciplined approach to entry and exit points in an asset class.

- Long term investment opportunities. In times of upheaval, carefully finding disciplined entry points to beaten up assets.

The present BEAR market is creating a situation where long term investors need to have their “Spidey-senses” on full alert. Upheaval always creates opportunity, as long as one controls the risk when adding funds to a volatile market.

Let’s transition to the markets for this holiday shortened week.

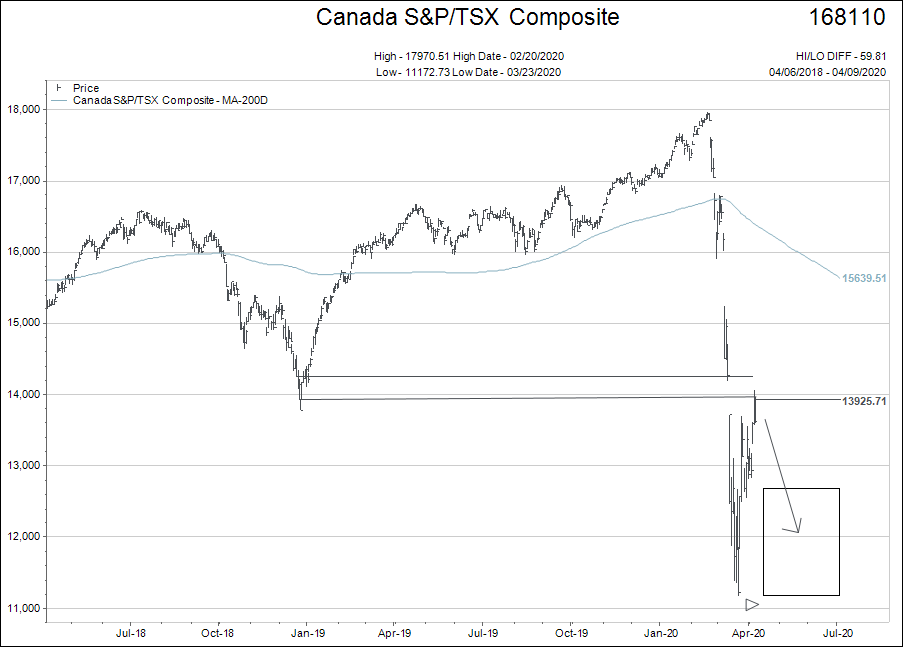

I am going to focus on the Canadian stock market for the rest of this comment. We could do exactly the same analysis for the US, but since our main goal is to add dividend paying Canadian companies to portfolios during this upheaval…I am going to stick with the TSX as my example.

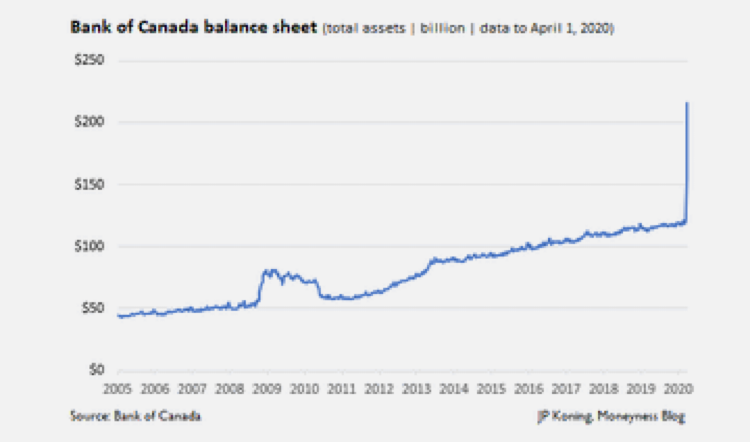

The chart above shows how historically remarkable the past 30 days have been from a Canadian monetary perspective. The Bank of Canada added 45% or $100 Billion to its balance sheet in a little more than a month.

Make no mistake about it. Without this effort, Canada would have been in a depression right now. I have no qualms with what the Bank of Canada is doing.

Unfortunately, as the Bloomberg headline said above, “We don’t know what is going on.” Will the central bank’s efforts be enough to stave off a sharp economic contraction? Will a vaccine be found and stimulate a quick rebound in confidence? Will we have an economic depression anyway?

Investors need discipline to help them navigate the unknown.

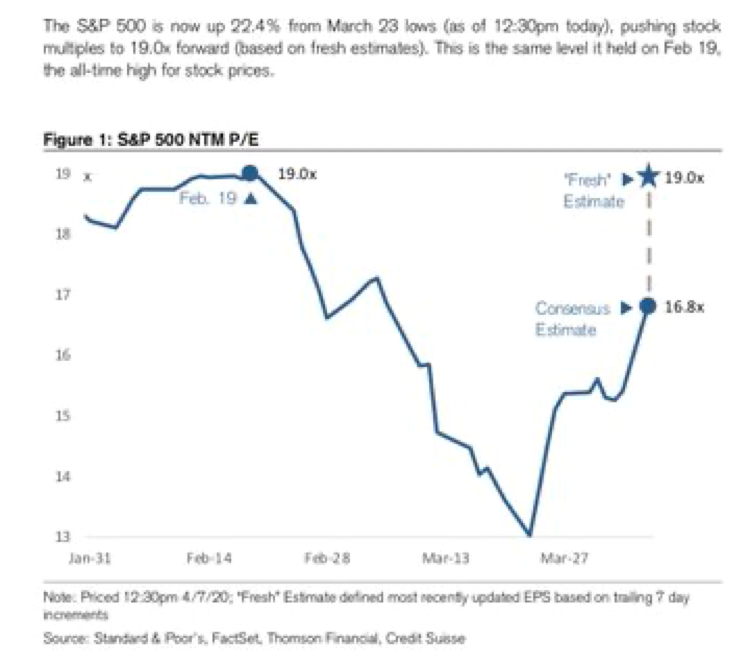

The fundamental case for stock market valuations is blurry given the massive shift in economic conditions. Below is the only chart I have seen where somebody has HONESTLY taken a stab at US earnings looking out a year. I have seen some Wall Street produced stabs, but they are ridiculously over-optimistic trying to be market supportive.

The “Fresh Estimate” is attempting to real-time the drastic changes in corporate America.

What this is saying is that in February, S&P earnings were looking to be $194.00, but by late March the estimate had come down to $169.00.

The estimate used in this graphic is $148 which, at a 19X multiple, gives a price of the S&P500 of 2812.

In a weak business climate for the foreseeable future, a multiple of 15X would make more sense and would offer a target of 2220, right near the low levels the market traded at in March.

The point is that stocks are no cheaper than they were at the peak of the market two months ago at 19X earnings estimates and in a weak economy are priced too dearly at present.

Therefore, fundamentally, there is no rush to buy this market.

The technical side of the equation is where we define our discipline as to HOW we plan to enter this market.

With the upside bounce targets now in place, this stock market rally can stop anytime from technical perspective.

The two horizontal lines depict the nearly filled “gap” the TSX created as it dropped. Note, there is one more “gap” in the chart that may fill before this BEAR market rally fizzles out.

The rectangular box with arrow defines the area of “retest” I am expecting between here and the end of June.

To end off, I want to share one caveat to the COVID-19 induced BEAR market, and the central bank money printing actions taken to try and buy time for the underlying economy to stabilize.

The central banks continue to expand their money printing schemes further into the financial markets. On Thursday, April 9th, they announced a “special purpose vehicle” (SPV) to buy junk bonds and support that market along with earlier announcements that support the rest of the spectrum of the debt and mortgage markets: All that is left is for the US Fed to buy stocks outright off the market which I believe they will do before this BEAR market is finished.

It is hard to keep up with, but I calculate somewhere around $7 trillion have been announced by the US Fed in the past 50 days to support Wall Street.

Understand, none of this spending helps the 19 million jobs that are lost in the real economy or makes the stock market any cheaper in value. The Fed actions are built to artificially support record high fundamental valuations and the banking system…full stop.

How that plays out in the price structure of markets is anyone’s guess. All I know for sure is that by not letting markets correct, the Fed is destroying the pricing mechanism of risk assets.

None of this will be easy for investors to sort through in coming months and years.

As always, feel free to email questions anytime.

Also, if you are looking for more information on the government measures to lessen the impact of COVID-19 for taxpayers, please checkout Megan’s post from last week.