In what follows, we outline a range of scenarios and how we’re thinking about the current oil price shock.

1. Higher oil will drive up inflation but the magnitude depends on the persistence of the shock

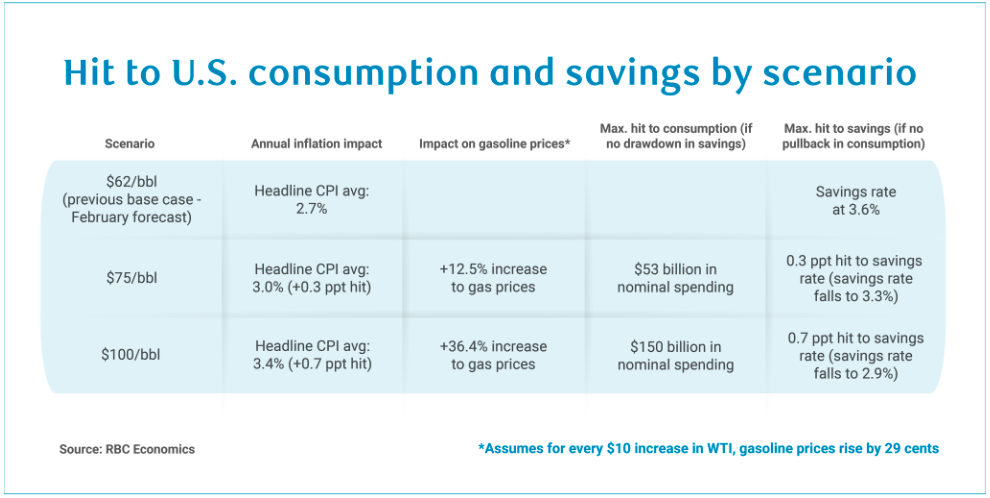

Headline inflation has now exceeded 2% for nearly five years while tariff pressures already threaten to keep it above target. Higher oil prices would compound this challenge, pushing inflation further away from 2%. As our Head of Global Commodity Strategy and MENA Research, Helima Croft, has emphasized, “[…] Duration will be the determining factor of the ultimate price trajectory for energy.” Over the past few days, we have witnessed $100/barrel realities and immense volatility. If prices were to return to $100/barrel and settle there, this would drive headline inflation meaningfully higher, by our own calculations, to above 3.5% by Q2 and remaining at that level throughout the year. This would add 0.7 percentage points to our forecast for headline inflation.

Even in a $75/barrel scenario, this would reflect a >20% increase from our base case assumption, driving headline inflation above 3% and keeping it there throughout the year.

2. Higher gasoline prices will weigh on consumers – with lower-income earners hit the hardest

For every $10 increase in oil prices, gasoline prices rise by just around 30 cents/gallon. Should WTI settle at $100/barrel (up ~$40 from our February base case assumption), this would mean a $1.20/gallon increase in gasoline prices – a 36% increase from our base case scenario (of $62/barrel average in 2026). Even a more modest $75/barrel would mean a 13% increase in gasoline prices. In this range of scenarios, the hit to nominal consumer spending could be between $50 and $150 billion for the year depending on where WTI settles . To this end, we are assuming the impact of higher energy prices, in the near-term, could produce a slight drag on consumption with a more meaningful impact on lower-income consumers. We expect that, in the near-term, the drag to consumption would be offset by higher revenues from the energy sector, suggesting the impact to GDP would be net neutral, for now. But whether the hit to consumption outweighs energy sector revenues is dependent on how long oil prices remain high and at what magnitude.

We have previously acknowledged that OBBBA will add to consumer spending capacity to varying degrees. These higher energy prices could offset the positive impact of OBBBA, nearly entirely. It is important to acknowledge that lower income consumers, who will be most exposed to higher energy costs also stand to benefit the least from OBBBA. Higher energy prices will evidently further exacerbate the K-Shape economy.

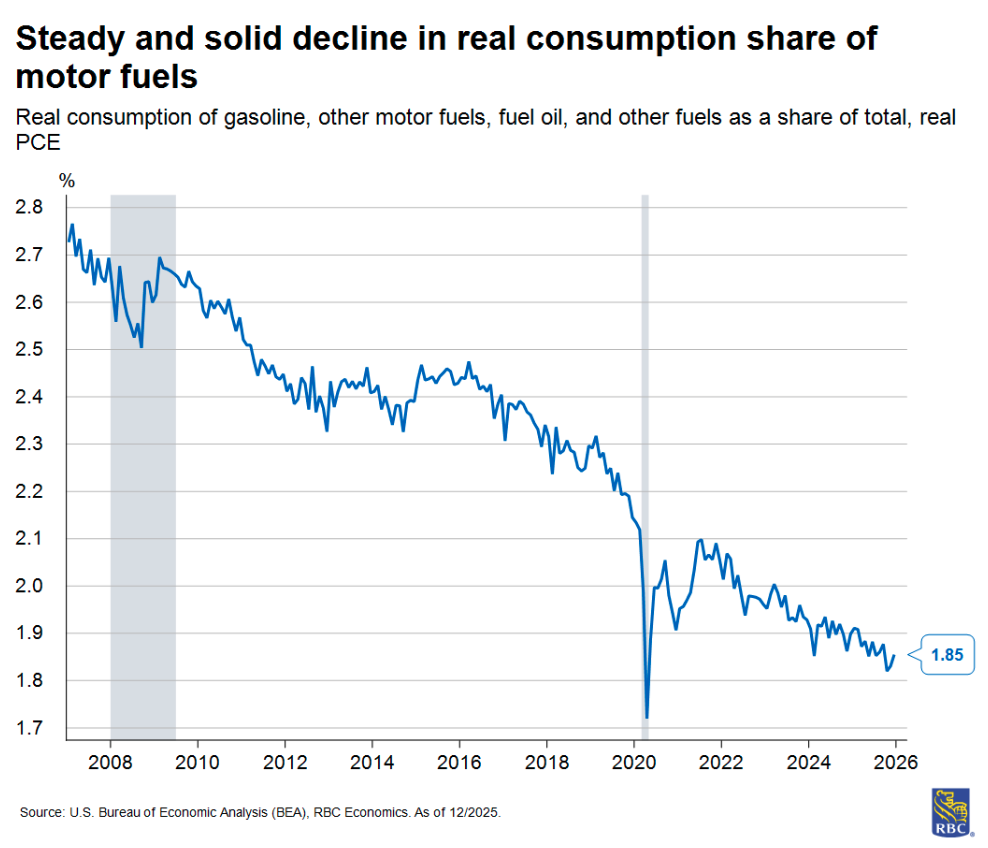

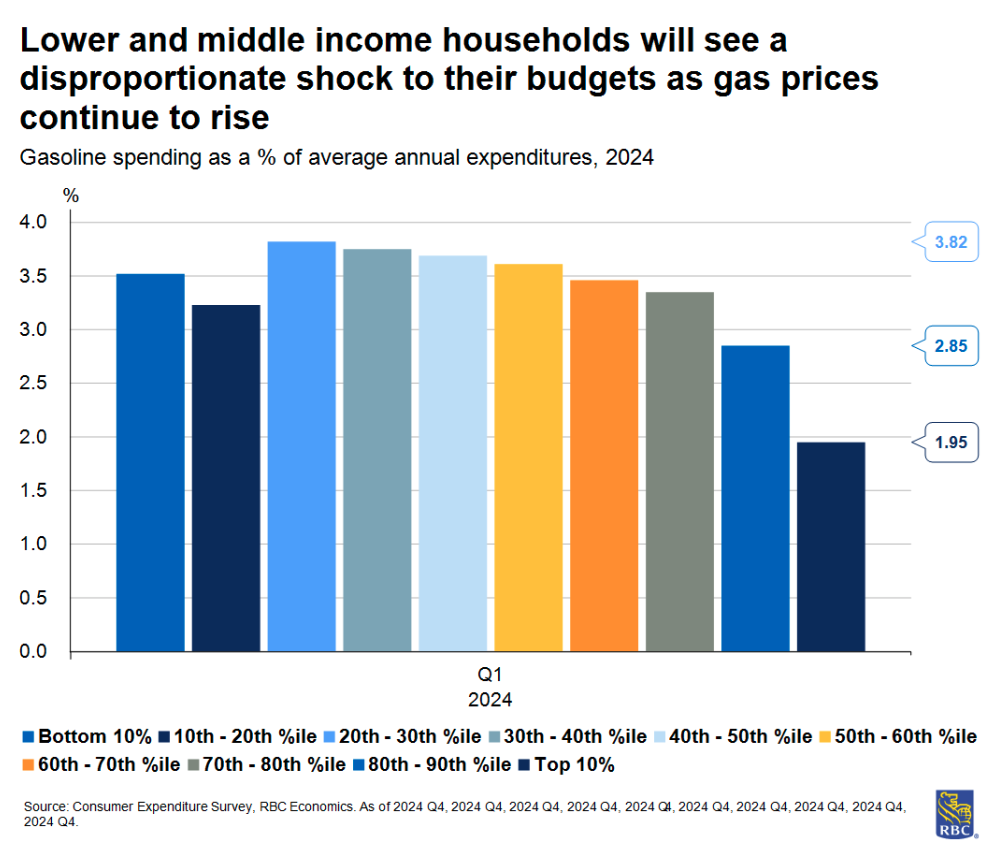

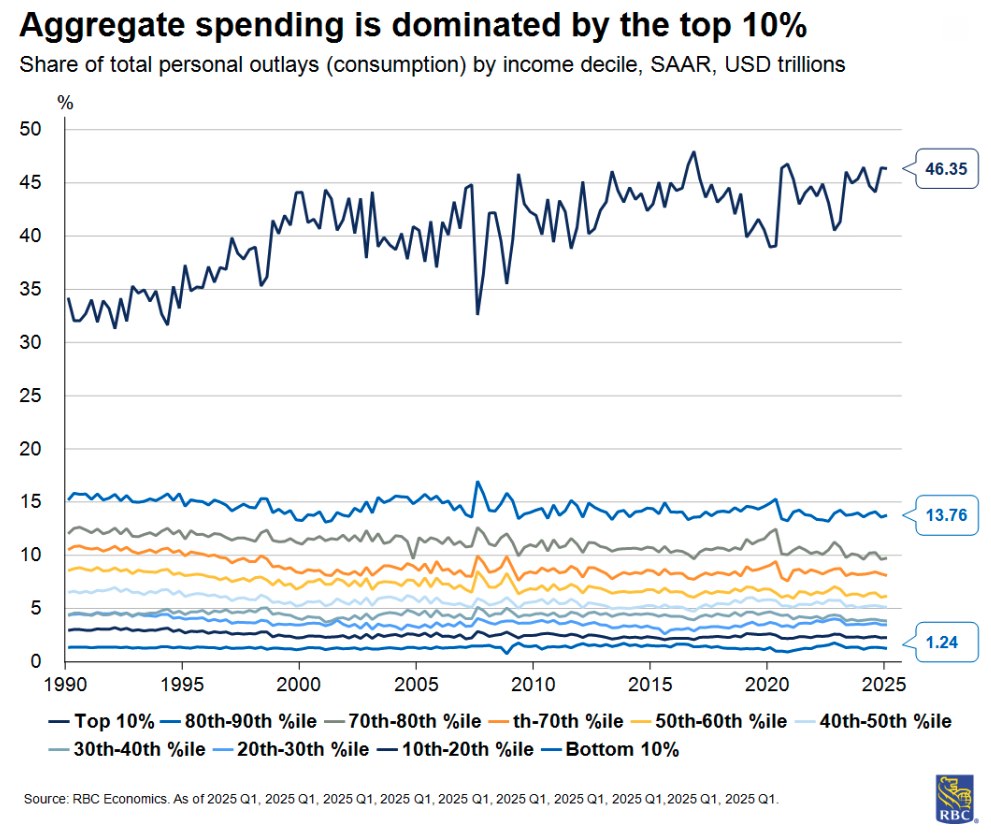

Households devote a relatively small share of their total consumption to energy products, and it has been continuously shrinking for decades. Until the 70s, energy products represented 6 to 7% of real consumer spending, which is why the 1973-74 and 1979 oil crises were extremely consequential for households in the US. But as of late, energy products represent a much smaller share of consumption, though the figure is larger for lower income consumers. The bottom 60% of income earners devote close to 4% of their take-home pay to gasoline, whereas, for the highest 10% of earners, the share is only about 2%. Still, higher energy prices will impact other consumer goods (and even services) as well. Higher gasoline prices will weigh on transportation costs, and these will be passed off to consumers. Since groceries represent nearly 10% of consumption for the bottom 60% of consumers, higher grocery prices will be consequential and this is at a time where we already expect to see little relief on the grocery front, since the USDA farmer prices’ paid index signals price pressures are coming through the pipeline.

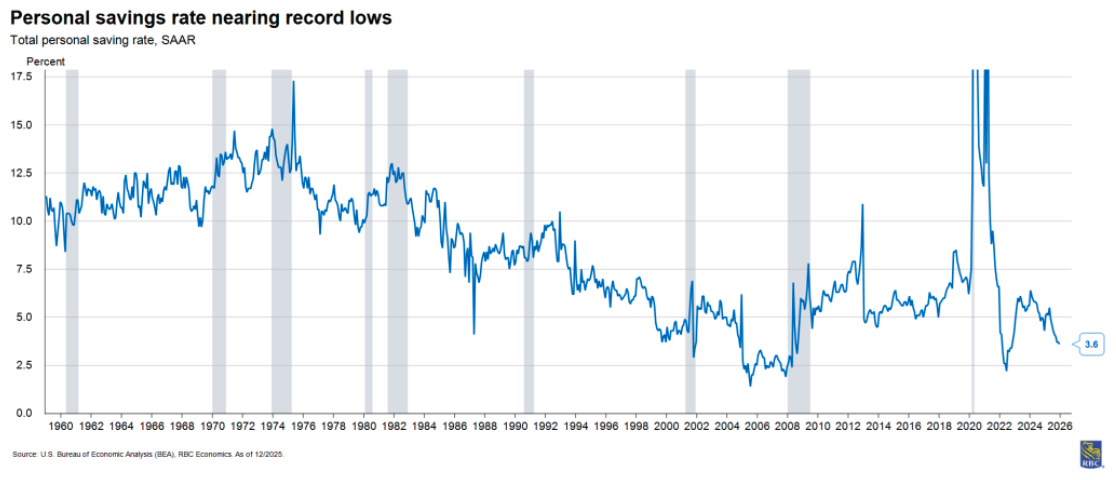

The question is, will an erosion in consumer spending materialize? In the face of higher energy prices (and in the absence of offsetting increases in wages), consumers have choices. They can either 1) opt to deplete savings (this is more realistic among middle-and-high income earners), 2) increase credit utilization and tap into buy now pay later alternatives (we are likely to see this among low-to-middle income earners) or 3) pare back discretionary spending since consumers must devote a greater share of their take-home pay to essentials. We expect 1) or 2) are more likely in the short term but a longer-duration oil price shock could mean real consumer spending takes a hit.

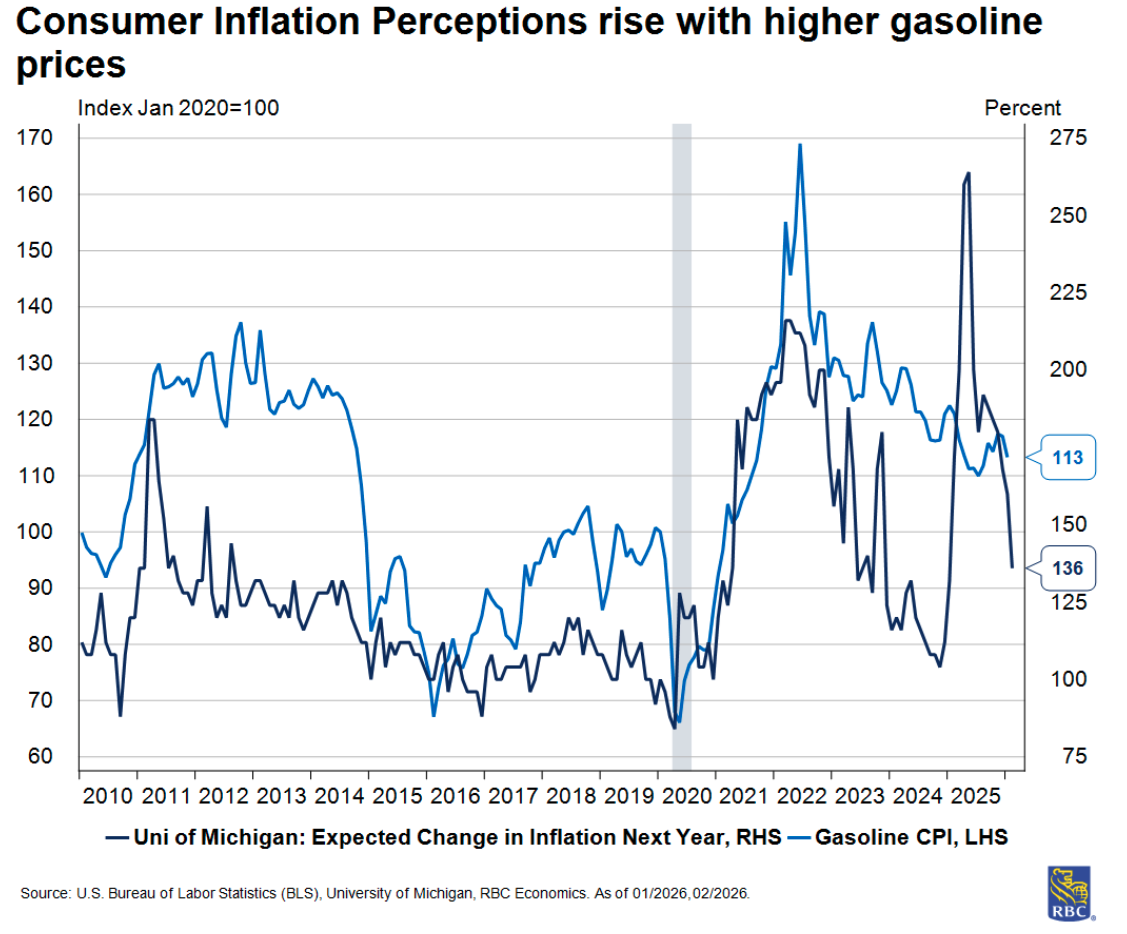

3. Perceptions of inflation will be the biggest issue

Monetary policy is not an appropriate tool to combat an oil price shock, which is why the Fed focuses on core inflation, specifically, core PCE. But perceptions of inflation will matter. Perceptions of higher inflation are problematic both for the Fed and consumers– this can instigate upward pressure on wages which drives services sector inflation higher (as labor-intensive sectors). This is the key risk as far as inflation is concerned, and whether it materializes depends, again, on the duration of the oil price shock

4. Higher oil prices solidify our view that the Fed will remain on the sidelines in the near term

We expected that the Fed will remain in “wait and see” mode through 2026 and, if anything, higher oil prices solidify this view. The Fed will be unable to meaningfully lower inflation resulting from higher commodity prices through monetary policy. The bigger risk will be whether we see a material deterioration in real consumer activity. Of course, the probability of this reality increases along with the duration of higher energy costs. And weaker demand could potentially spill over into the labor market in the medium term, exacerbating the cyclical weakness that we have been experiencing.

About the Authors

Mike Reid is Head of U.S. Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC Capital Markets. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an Economist at RBC Capital Markets, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.