With the Middle East in a serious crisis, it’s worth examining how prior military conflicts impacted global stock markets, and what this means for investors today.

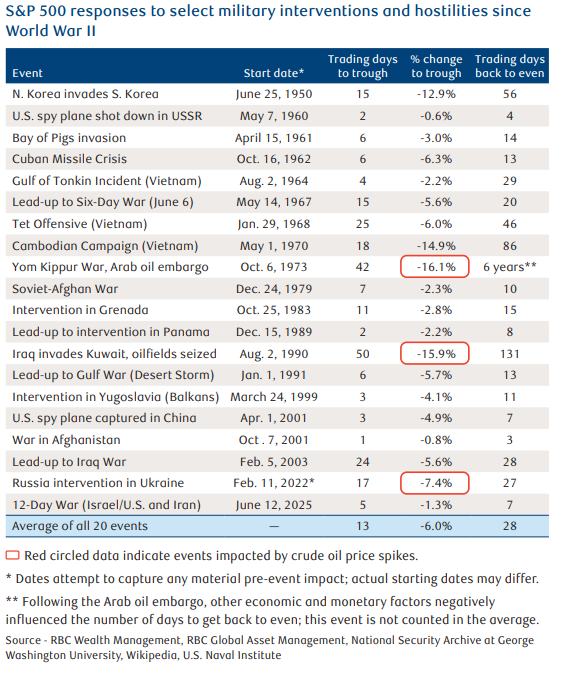

In 20 major post-World War II military interventions and hostilities the following has occurred:

- S&P 500 fell 6 %, on average, from the initial market impact to the trough level.

- In 19 of the 20 events, the market took an average of 28 days to return to where it had been prior to those events.

- The data is consistent, whether conflicts lasted months or years

The duration of a particular conflict historically has not had much bearing on market performance. However, one must dig deeper to find other clues.

Energy

Market performance can leave long lasting effects, especially when energy supplies were disrupted.

Two events that prompted oil shocks resulted in double-digit stock market losses:

- 1973 Yom Kippur War and Arab oil embargo

- 1990 Iraq invasion of Kuwait and seized its oilfields.

The S&P 500 traded down by 16.1 % and 15.9 %, respectively.

During the third oil shock related to a military operation— the beginning of Russia’s intervention in Ukraine—the stock market declined 7.4 %.

Nuances associated with two of those events:

- The Arab oil embargo in October 1973, which lasted five months and occurred when the U.S. economy was much more dependent on oil imports than today, kicked off a lengthy recession and an inflation surge that lasted for many years later. There were also fiscal policy and Federal Reserve monetary policy mistakes during this period. The S&P 500 took six years after the onset of the Arab oil embargo for the market to return to even in 1979, and it didn’t move meaningfully higher until the 1980s. Many investors gave up and exited equities altogether in the 1970s—missing substantial market gains from the 1980s onward.

- Russia’s military operation in Ukraine, WTI crude oil was above $90 per barrel for six straight months in 2022, peaking at nearly $124 per barrel. The U.S. stock market selloff was less severe during this episode, as Russian crude oil supplies would not be meaningfully hindered.

Economy

Economic and corporate earnings trends are key for stock market performance over the mid and longer term, and military interventions can impact these trends in rare cases. The good news is, heading into this Middle East crisis, leading U.S. economic indicators were not hinting of U.S. heightened recession risks.

Consumer spending, service sector, and employment trends have been relatively fine, although there are fragilities for the latter under the surface.

The fourth quarter of 2025 corporate reporting season has shown respectable earnings, revenue, and profit. Forward consensus earnings estimates have risen further.

RBC GAM: The conflict has “Introduced a new meaningful economic risk and, while these kinds of military actions don’t usually have lasting economic significance, we acknowledge that the range of potential outcomes for the economy and markets has widened. Iran and the Middle East are a key source of energy for the world, and should the conflict be sustained or even escalate, restrictions to oil supply and/or higher crude prices could hinder economic activity and/or weigh on investor sentiment.”

The RBC Capital Markets commodity strategy team has cautioned that in a prolonged scenario, oil prices could reach above $100 per barrel, and global natural gas prices could climb to their highest since the first quarter of 2023.

For the U.S. stock market, RBC Capital Markets equity strategy team makes an important caveat about energy prices: “…the key issue is not whether there is a short-term spike in oil prices.

What’s more relevant to stocks is whether a sustained impact to oil prices is seen, which is what we think would have more of a potential to damage confidence at various levels.”

If a lengthy oil shock occurs and stokes inflation, large portions of the American population do not have much room to absorb it.. Many households are still struggling with the 26 % cumulative increase in consumer prices that has occurred since January 2020, right before COVID hit.

It’s prudent for investors to assume that military and geopolitical risks can push the U.S. equity market into a temporary 5 % to 10 % pullback or, in rarer cases, an even longer-lasting correction of greater magnitude.

With the S&P 500 currently near its all-time high, such selloffs need to be put into perspective.

While the average 6 % decline of the past 20 episodes should not be dismissed, it’s well within the bounds of a typical, modest pullback in many scenarios that often confront markets—including scenarios that have nothing to do with military clashes.

Brief midyear pullbacks are common, even when the market ends up performing well for the full year.

The S&P 500 declined by 10 % or more at some point during the year in more than half of the years since 1980.

U.S. Mid-Terms

In the 23 midterm years since 1934, the S&P 500 has experienced a noteworthy downturn with an average peak-to-trough decline of just over 20%—typically followed by a robust rebound that usually went on to set new highs.

It continues to be sensible maintaining U.S. equities at the Market Weight level (long-term strategic allocation level) in portfolios as long as indicators are signaling that the U.S. economic expansion should persist, and S&P 500 profit growth is not materially threatened.

However, one must be mindful that this Middle East crisis is highly fluid and unpredictable, and events could escalate further. it’s prudent to expect and plan for some potentially unnerving market volatility this year

If you have any questions or comments, please feel free to let me know.

Many Thanks,