What matters more for the market, Washington policy or corporate profits?

Washington will capture much press this year, with policy developments likely generating volatility. It is earnings trends however, that will determine the U.S. equity market’s fate over the long term.

Let’s look at the ongoing Q4 earnings season and the earnings outlook for the year.

The ongoing Q4 2024 earnings season is in good shape thus far – from the standpoint of earnings and revenue beat rates and magnitude of beats.

However, there have been some highlights and lowlights.

78 % of the S&P 500 by market value have reported results as of Feb. 13. Q4 2024 earnings-per-share (EPS) growth estimate has jumped to 12.6 % from 7.3 % since Jan. 10, according to Bloomberg.

The Bloomberg full-year consensus EPS forecasts are for $246 per share (9.4% y/y growth) in 2024 and $271 per share (10.4% y/y growth rounded) in 2025. The $271 per share 2025 estimate is lower than the $273 per share forecast right before the earnings season began. This is not an issue, as the full year forecast typically retreats at this stage of the year.

It now looks more realistic, assuming annual U.S. GDP growth holds up near the 2.2 % consensus forecast for this year or exceeds it.

Earnings reports from five of the so-called Magnificent 7 stocks—Alphabet, Amazon, Apple, Microsoft, and Tesla—have been lowlights. Meta Platforms was the exception, and the other Magnificent 7 stock, advanced chipmaker NVIDIA, is scheduled to release results on Feb. 26.

Even though earnings growth exceeded the consensus forecast for many of them, the quality of the results didn’t live up to those of previous quarters. There were blemishes in terms of revenue growth of key units, with lower-than-expected forward projections from management teams.

The results and guidance also didn’t rise to the very high expectations that had been baked into share prices and valuations. There was little room for error, and all five stocks sold off after they reported.

Each Magnificent 7 firm is very involved in the global artificial intelligence (AI) ecosystem. Scrutiny on the billions in AI capital spending that has already occurred by these companies—with more in the pipeline—will be in focus in coming quarters.

So too will competition and developments coming from China’s AI firms

Pressure continues to build for AI leaders to show investors real prospects for the return on invested capital in their AI buildouts, as price-to-earnings valuations still look elevated.

Magnificent 7 earnings trends going forward will likely help shape market performance in the near term, especially given this group represents about 32 % of the S&P 500’s market value.

With such a large footprint, when the Magnificent 7 stocks do well, they tend to boost S&P 500 returns like in 2023 and 2024. In contrast, when their shares consolidate or sell off, they can constrain or hinder the S&P 500’s progress, like recently.

With such a large footprint, when the Magnificent 7 stocks do well, they tend to boost S&P 500 returns like in 2023 and 2024. In contrast, when their shares consolidate or sell off, they can constrain or hinder the S&P 500’s progress, like recently.

Q4 2024 earnings results from the rest of the market have, on balance, been pretty good so far.

The S&P 500 excluding Magnificent 7 is moving at 7.5 % year-over-year earnings growth thus far, which is ahead of 3.7 % in the previous quarter.

Results from the Financials sector have been standouts.

We wait to hear from retailers and consumer discretionary companies for signs of stress among lower-income households and continued inflation.

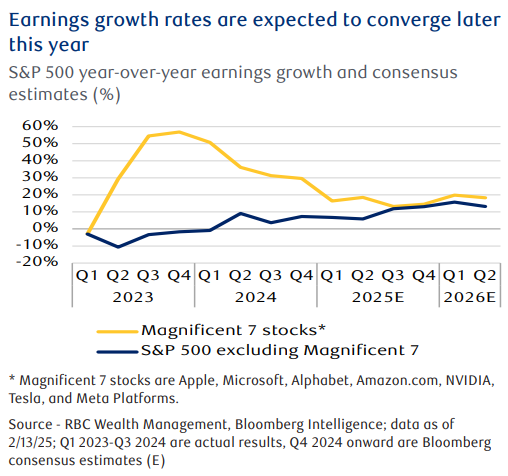

The big question is whether forecasts of earnings growth rates for the Magnificent 7 and the remainder of the companies in the S&P 500—will finally converge.

The consensus forecast is for Magnificent 7 earnings growth to continue to decline this year mainly due to challenging year-over-year comparisons. This would not be a negative development, so long as major hiccups don’t occur, and things play out as forecast.

In contrast, earnings growth for non-Magnificent 7 stocks is expected to pick up later this year.

Whether or not the current convergence forecast plays out will depend on economic developments.

If 2025 consensus GDP growth forecast deteriorates meaningfully from the current 2.2 % level, the likelihood of this convergence would diminish.

Should GDP growth and earnings convergence play out as forecast, non-Magnificent 7 S&P 500 firms will deliver meaningful share price returns as a group this year.

As always, please let me know if you have any questions or comments.