The last five years have felt like a blur.

From global lockdowns, government stimulus, green initiatives, 40-year highs in inflation, rising interest rates, , growing geopolitical uncertainties, and the rise of artificial intelligence (AI), along with a myriad of other notable events – we have seen it all.

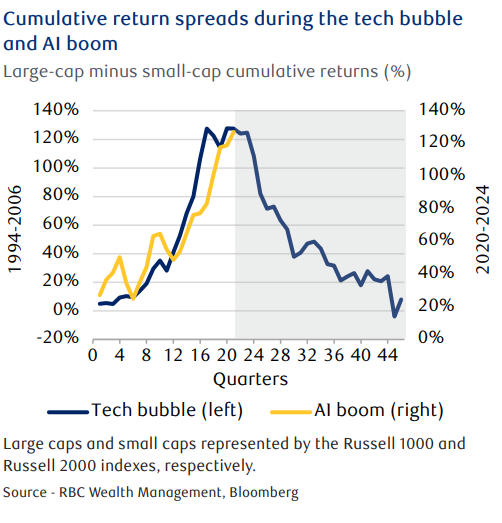

These unprecedented events have helped to decouple large- and small-cap return profiles—much the same as during the tech bubble boom in the early 2000s—helping to shape an unusual and powerful tailwind for large-cap stocks.

This dynamic has now built large-cap versus small-cap cumulative returns over recent years into the gap as seen in the chart at left.

This dynamic has now built large-cap versus small-cap cumulative returns over recent years into the gap as seen in the chart at left.

This chart may be a bit misleading as we have seen near all-time highs in market concentration across a very narrow subset of names driven by the AI boom—these are chiefly known as the “Magnificent 7.”

Even when excluding the Magnificent 7 from the large-cap index returns, large-cap stocks have still outperformed their small-cap couterparts.

This is reminiscent of the outperformance of large caps during the early 2000s—driven in large part from a lack of earnings power which helped drive the collapse of the trade.

Large-cap earnings today have continued to deliver with no signs of investor appetites for AI or other related investment abating anytime soon.

This does not mean that cumulative return spreads reset in a similar way to last time over the next several years, but they are likely to be spurred on by other less obvious drivers in addition to elevated investor expectations.

Mergers and acquisitions (M&A) along with initial public offerings (IPO) have historically been key drivers for overall small-cap index performance outside of earnings.

Large-cap company balance sheets hit an all-time record last quarter coming in at nearly $2.5 trillion with Financials sector companies holding nearly 50 % of the total and Technology, Consumer Discretionary, Communication Services, Health Care, and Industrials names making up the bulk of the remainder.

Despite large-cap company balance sheets being flush with cash, last year was the worst on record for small-cap M&A going back several decades.

According to Bloomberg data, 2024 closed out the year with just 52 deals in the small-cap space for a cumulative total of $113.7 billion - worse than during the 2008 financial crisis where just 61 deals were closed.

According to Bloomberg data, 2024 closed out the year with just 52 deals in the small-cap space for a cumulative total of $113.7 billion - worse than during the 2008 financial crisis where just 61 deals were closed.

Since the U.S. Federal Reserve started raising rates at the beginning of 2022 we’ve seen rate-sensitive sectors like Financials, Communication Services, and Real Estate have substantially fewer deals overall, verifying the close tie between monetary policy and overall corporate risk-taking.

As for small-cap IPO activity—which also points to investor risk appetites—2024 marked the return to a “new normal”; the year averaged just 31 deals and a scant $7 billion per quarter in value.

While up from 2023’s lackluster $7.7 billion in total for the year (the smallest amount raised in over three decades), pre-COVID-era small-cap listings were typically in the 60–100 count and $15 billion–$20 billion total ranges per year.

2024 marked an about-face in monetary policy as the Fed started a fresh  round of easing after a few years of tighter policy decisions.

round of easing after a few years of tighter policy decisions.

These changes helped spur the beginnings of “green shoots” in the small-cap IPO space. 2025 could continue that trend and serve as a turning point as large caps look to spend cash hoards and as more deal-friendly administrators take the wheel.

The incoming Trump administration figures are likely to be in place, providing needed tailwinds to both deal activity (M&A) and IPOs.

Tailwinds to small-cap stocks closing the gap to large include extremely elevated consensus earnings expectations for large caps (particularly amongst AI-related names), election risks fading.

More M&A-friendly regulators set in place, easier Fed policy to reignite corporate risk-taking, and record cash hoards being put to good use.

After years of underperformance relative to large-cap counterparts, small caps seem poised to return to form.

As always, please let me know if you have any questions or comments.