A number of events are likely to occur in Q1 2025 that could be well received by equity markets if their outcomes are better than anticipated.

Let’s examine in greater detail:

U.S. tariffs: Threat or Reality ?

Tariffs threatened by U.S. President-elect Donald Trump on the EU could be a significant headwind to a region saddled with meagre economic growth.

RBC Global Asset Management Inc. Chief Economist Eric Lascelles estimates that two years after the implementation of a 10 % blanket tariff, eurozone GDP would be 1 % smaller than it otherwise would have been. 2025 consensus GDP growth eurozone forecasts have been downgraded marginally to 1 % from 1.2 % since the U.S. elections in November.

Trump’s approach suggests that there may be room for negotiations.

By giving the U.S. some concessions, such as increased defense spending or purchasing more U.S. oil and liquified natural gas, the EU may be able to avoid the worst-case scenario of an escalating trade war or see only certain sectors affected by tariffs.

Given investors’ anxiety regarding the impact of tariffs on the region, such relatively favourable outcomes would likely be a relief for markets.

German federal elections: The Splintered Coalition

Germany is the largest economy in Europe. The elections to be held on Feb. 23 are important given the German economy has sputtered since the end of the pandemic.

Due to little ideological overlap, the three-party coalition that governed the country since 2021 proved ineffective at redressing the situation. The coalition eventually collapsed, unable to strike an agreement to provide the fiscal stimulus the economy sorely needed.

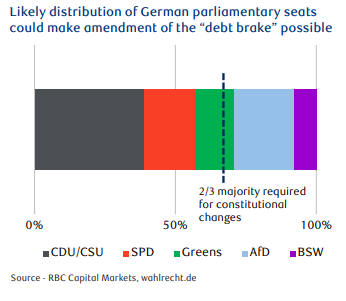

Additional spending has not been possible due to the “debt brake,” the measure enshrined in the German constitution that limits the deficit to a stringent 0.35 % of GDP per year. Modifying this rule requires a high two-thirds majority in parliament— unachieved to date.

Polls are indicating change is coming.

The centre-right conservative alliance of the Christian Democratic Union of Germany (CDU) and the Christian Social Union in Bavaria (CSU) is likely to garner the most votes but fall short of a majority. A coalition with the centre-left Social Democratic Party (SDP) as a junior partner is the consensus outcome—such a coalition has governed effectively in the past.

A CDU/CSU-led government would have little alternative but to modestly loosen its fiscal stance.

A CDU/CSU-led government would have little alternative but to modestly loosen its fiscal stance.

It also foresees some additional defense and infrastructure spending under this outcome.

Reforming the debt brake may no longer be off-limits, particularly if the three traditional parties (CDU/CSU, SDP, and the Greens) achieve a two-thirds majority, as predicted by current polls.

All three parties seem open to the possibility of reform. Politicians see the constitutional rule as outdated. Germany’s Debt sits at 60% of GDP— which is very low in by international standards.

The CDU/CSU platform calls for a decrease in the business tax to 25 % from 30 %, to be at least partly financed by pruning unemployment benefits. Some de-regulation may be possible, along with a potential return to nuclear energy production through reactivation or the establishment of new reactors to alleviate energy cost pressures.

To summarize, an end to the paralysis that characterized the previous coalition government, a more pro-business government, and modestly accommodative fiscal policy would be beneficial to the economy. These policies, if implemented, would likely please equity markets.

Investors should be mindful that large-scale fiscal stimulus remains unlikely, as the CDU/CSU is, after all, a conservative party in the European context.

China: How Strong Will Demand Actually Be ?

A healthier Chinese economy would improve Europe’s prospects given China is a key export destination for European goods. Many European companies have operations there.

While official announcements in China over the past few months have largely underwhelmed recent ones have suggested a “more proactive fiscal policy,”

In December, Beijing pledged to stabilize the property market in 2025. This suggests that investors should remain confident that an expansionary policy is coming. China likely still has policy space to provide significant economic support.

The market expects policy announcements at the March 2025 “Two Sessions,” the annual key political discussion for major policy decisions. A large stimulus announcement would boost Europe’s fortunes.

Looking Ahead

There are notable near-term headwinds to European equity index outperformance. They range from a lack of competitiveness and meagre economic growth to geopolitical risks.

Given investor sentiment is downbeat and low valuations already seem to reflect many of these headwinds, a positive outcome from any of these events could provide opportunities for investors.

A ceasefire agreement between Russia and Ukraine and a deeper European Central Bank rate-cutting cycle would also be perceived positively.

Our investment strategy has been to focus on world-leading companies that benefit from and drive global structural trends, particularly in niches such as semiconductor manufacturing equipment, electrical and mechanical engineering, industrial gases, and health care.

As always, please let me know if you have any questions or comments.