In a historic comeback, Donald Trump won the presidency for a second time.

Today we look at the key policies like taxes and tariffs that will shape the investment climate.

There is quite a bit to unpack – so let’s get to it !

While Washington can influence the business cycle for good or for bad, it doesn’t control it.

The S&P 500 rallied to another new all-time high and other major U.S. indexes jumped as well following news that Donald Trump was once again elected president of the U.S. and Senate control flipped to the Republicans.

Trump is only the second person in American history elected to two non-consecutive presidential terms, the other being Democratic President Grover Cleveland.

While vote counting is ongoing in some House of Representatives races, it’s looking to us like Republicans will retain control of the lower chamber of Congress by a slim margin, which would usher in a Republican sweep.

While vote counting is ongoing in some House of Representatives races, it’s looking to us like Republicans will retain control of the lower chamber of Congress by a slim margin, which would usher in a Republican sweep.

Decision Desk HQ, a firm leveraged by The Hill, a news agency that covers Congress closely, estimates that Republicans have an 85 % likelihood of retaining House control based on the results of very competitive races and vote counting in others as of midday Thursday.

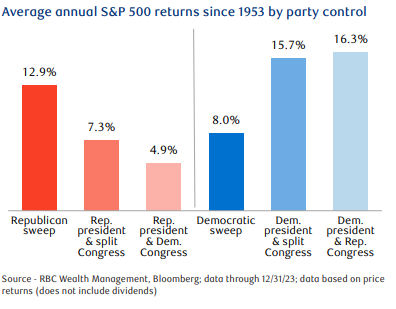

The U.S. stock market has historically performed well during a Republican sweep configuration, rising 12.9 % on average, (chart above).

The Trump Agenda:

Market participants seem optimistic about three important factors:

- Personal Tax Rates - stay low and could be lowered further.

If Republicans win control of the House, Congress would pass and Trump would sign a new tax package to extend much or all of the low-tax provisions which became law during his first term. This would impact individual income tax rates, and taxes on estates, gifts, capital gains, and dividend income, among other provisions. Trump’s additional campaign proposals for “no tax on tips” and to eliminate taxes on Social Security retirement benefits could be added to any new tax legislation that would extend the existing low-rate provisions.

- Corporate taxes to remain at 21 % rate. Domestic manufacturers taxes may drop to 15 %

Other business-friendly tax incentives could be written into the tax code if the Republican sweep plays out.

- Trump’s goal of aggressive deregulation is being embraced—for now

The market’s enthusiasm may be getting ahead of itself. Trump aimed to deregulate during his first term and achieved this in certain areas, particularly the energy sector.

The number of new regulations during Trump’s presidency was initially lower than the first three years of the Biden, Obama, and Clinton administrations, and was even slightly below the George W. Bush administration.

In the fourth year of Trump’s term, the number of regulations surged, perhaps partly due to the pandemic.

In total, his administration ended up implementing more economically significant new regulations than Obama did in his first term.

Obstacles To Cutting The Red Tape:

- Career federal agency employees, who have historically been more aligned with the Democratic Party, could slow the process or put a spoke in the wheel

- Lawsuits will likely challenge certain deregulation provisions and could come from various and well-funded interest groups, including those tied to the Democratic Party and progressive organizations

- Federal court rulings could stall or halt specific deregulatory efforts

- The Supreme Court’s “Chevron Ruling” tilts authority back to the judicial branch, specifically regarding the interpretation of unclear legislation.

Tariff worries are lurking

The U.S. equity market seems to be looking past the economic risks associated with Trump’s tariff proposals. Perhaps market participants are waiting to gauge whether the actual implementation of tariffs could be as aggressive as his original campaign proposals for 10 % across-the-board tariffs on all goods imports, including from allied countries, and 60 % tariffs on Chinese imports.

Tariffs and other trade barriers as mostly lose-lose propositions.

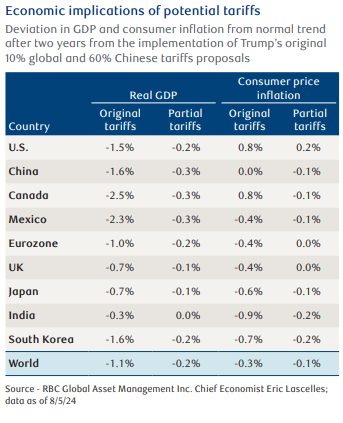

RBC Global Asset Management Inc.’s Chief Economist Eric Lascelles has pointed out that while tariffs undeniably hurt the country that has tariffs levied against it, they usually also hurt the country levying them.

Eric forecasts that the drag on economic growth and the impact on inflation could be manageable for the U.S. economy in both the “original tariffs” and “partial tariffs” scenarios.

In the original tariffs scenario (10 % on all  goods and 60 % on Chinese goods), he estimates that after two years of implementation, U.S. GDP would be 1.5 % smaller than it otherwise would have been, and inflation would be 0.8 % higher than it otherwise would have been.

goods and 60 % on Chinese goods), he estimates that after two years of implementation, U.S. GDP would be 1.5 % smaller than it otherwise would have been, and inflation would be 0.8 % higher than it otherwise would have been.

In the partial tariffs scenario, he estimates U.S. GDP would be 0.2 % smaller, and inflation would be 0.2 % higher after two years of implementation.

It is likely that worst-case tariff scenarios will not play out and the other pro-growth measures that Trump is proposing could offset the GDP headwinds from tariffs.

At a minimum, tariff policy has the potential to generate volatility for the U.S. and other equity markets in the months ahead.

How to factor industry beneficiaries into portfolio allocations

On the first day after the election, four S&P 500 sectors outperformed—Financials, Industrials, Consumer Discretionary, and Energy. Small-capitalization stocks also rallied strongly. Trump presidency/Republican sweep trade is a good thing – for now.

Is it worth making big adjustments in portfolios to tilt more toward these areas of the market?

While these areas may have further near-term outperformance, it’s important to keep in mind that over the course of a full four-year presidential term, things don’t always pan out according to the president’s policy preferences.

Presidents prefer certain industries. It doesn’t mean market performance will follow suit.

The Energy sector performed well soon after Trump was elected in 2016 and had other spurts of outperformance during his presidency, however, in the latter part of 2018 the sector began to struggle, and during his full four-year term it badly underperformed the S&P 500 .

There are other examples associated with the Biden administration as well.

Regarding Industrials, RBC Capital Markets LLC’s Head of U.S. Equity Strategy Lori Calvasina points out that she currently views this sector as being expensive from a valuation standpoint and it underperformed when Trump imposed tariffs on China in 2018.

Regarding small-cap stocks, Calvasina thinks they look “a bit stretched” at this stage, and notes that moves associated with the last two elections were short-lived.

The direction of interest rates, inflation, and Fed policy will be much greater determinants of small-cap performance in the coming months and years.

The bottom line: Other factors tend to dictate stock performance…More than who sits in the Oval Office and which political party controls Congress.

Industry and sector tilts in portfolios should be evaluated according to a range of factors, not solely political ones. Furthermore, well-diversified equity portfolios should already have exposure to these areas of the market.

Elections come and go: Don’t deviate from long-term investment plans

There is little doubt that market participants will pay more attention to Washington than they have under Biden. Trump’s policies, to no one’s surprise, will be accompanied by dramatic rhetoric and bold action.

This could generate some equity market volatility at times.

For long-term investors, the most prudent strategy with respect to elections is to:

- Give deference to the long-term investment strategy that you already have in place

- Avoid the temptation of making drastic asset class or sector changes based on the election outcome.

If you’re enthusiastic about Trump retaking the White House, don’t get out over your skis. If you’re concerned about another Trump presidency, don’t let emotions get in the way of sound investment decisions. Markets have risen under both Republican and Democratic presidents !

Ultimately, over the course of the next four years, the U.S. equity market will be impacted more by the natural ebb and flow of the business cycle, Fed policy, and innovation.

Washington can influence the business cycle for good or for bad, but it doesn’t control it.

As always, please let me know if you have any questions or comments.