Today we’ll examine China to find how policy and fundamentals can continue to foster economic growth.

Chinese equities closed out 2025 with strong annual gains. The MSCI China Index surged 31 %, while Hong Kong’s benchmark Hang Seng Index rallied 28 %. The gains caught many market participants by surprise, given ongoing U.S.- China trade tensions.

The following factors will likely shape equity market returns in 2026.

Chinese policymakers outlined their roadmap for 2026– 2030 in the 15th Five-Year Plan announced in October 2025. Regarding economic growth, the plan aims for China to reach the level of moderately developed countries by 2035.

This implies nearly a 50 % increase in GDP per capita to US$20,000 from the current US$13,300 level. Policymakers specified that China will achieve an annual average economic growth rate of 4.17 % over the next decade in official

Securing higher growth at the outset of the 15th Five-Year Plan period would allow the target to ease in subsequent years.

Pursuing stronger growth in the early phase may also be a positive indication, bolstering household and business confidence.

Pursuing stronger growth in the early phase may also be a positive indication, bolstering household and business confidence.

But what about long-term growth challenges?

Setting ambitious growth targets is inspiring, yet investors may question their achievability.

China continues to face multiple long-term growth challenges, for example, property market correction, weak domestic consumption, deflationary, and geopolitical tensions.

While these issues are unlikely to resolve quickly, their broader economic and equity market impacts require careful analysis.

Let’s examine the property sector: Residential property prices and investment remain in a downturn, and developers continue to face distress. 2/3 of China’s top 50 developers have defaulted on bond payments in recent years.

However, the impact on the economy and equity market should be less severe than years ago.

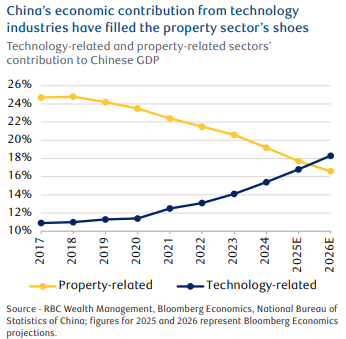

At the peak in 2018, property and related sectors contributed 25 % of China’s GDP. This has fallen significantly. The property sector now accounts for just 1.4 % of the MSCI China Index, limiting its direct equity market impact.

Policymakers have also reduced emphasis on the property sector, ranking it last among eight economic priorities for 2026.

Recent stimulus measures (trade-in subsidy program for consumer goods) suggest that subsidy amounts will be more restrained than last year.

So, will the government implement meaningful action?

Policymakers are now focusing on reducing income inequality and preventing a resurgence in rural poverty. Recent labor market weakness has suppressed wage growth for migrant workers, and the growth in migrant worker numbers has slowed significantly since 2023. The rural poverty rate could increase if migrant workers lose their jobs in the city and move back to rural areas.

Expect more targeted measures aimed at strengthening the social safety net for lower-income groups, rather than broad-based consumer subsidies. Potential new initiatives, such as reducing maternity-related costs, may also be introduced.

Technology have emerged as the clear growth engine.

Following recent breakthroughs in electric vehicles, innovative drugs, and AI, technology has emerged as a new driver of China’s economic growth. Policymakers aim to deploy technology economy-wide to enhance productivity, enable scalable commercial applications, and generate new demand. Consider that Chinese deployment of robotics in manufacturing is 12x greater than the U.S. when adjusted for income.

To achieve these goals, the central government may assume a greater role in directing technology and industrial policy. This could reduce local protectionism, market segmentation, and overcapacity issues.

The renminbi has begun 2026 with a notable rally, appreciating nearly 1 % against the U.S. dollar over the past month and strengthening past CNY 7.0 for the first time since 2023. The People’s Bank of China may tolerate further renminbi appreciation against the dollar as the U.S.-China trade truce looks more durable this time.

If growth concerns ease and depreciation risks subside, the central bank is likely to reduce currency market intervention.

After a year dominated by U.S.-China trade tensions, China’s economic trajectory appears to be back under its own control. The latest trade deal between the two countries, reached in October, appears more durable and is likely to set the stage for a more sustainable Chinese equity market rally.

The MSCI China Index now trades at a more reasonable valuation, with a 12-month forward price-to-earnings multiple of 12.7x, (11.6x historical average). Valuations of China’s AI and internet leaders also look discounted relative to their U.S. peers.

As investors increasingly question whether U.S. AI companies are overvalued, this may lead to greater interest in Chinese AI – providing support for the broader equity market.

If you have any questions or comments, please do not hesitate to let me know.

Many Thanks,