North American equity markets continue to carve out new highs, even in the face of new uncertainties.

President-elect Donald Trump recently proposed significant tariff increases: 25% on imports from Canada and Mexico and an additional 10% on Chinese goods.

Countries generally use tariffs to protect domestic industries by raising the cost of imports and encouraging consumption of locally produced goods.

Tariffs also provide a source of government revenue. However, in practice, the benefits to the country imposing the tariff are often offset by several forces.

Domestic businesses that rely on foreign inputs to produce their own goods may face higher costs. Retaliatory tariffs can harm exporting industries.

In the end, consumers usually bear the brunt of the costs through higher prices.

Let’s consider Crude Oil. Oil accounts for nearly 1/3 of Canada’s exports to the U.S., and energy makes up a significant portion of the Canadian equity market. While tariffs would obviously hurt the Canadian economy and its stock market, Canadian oil represents around 20% of U.S. oil consumption, and without clear alternatives, oil prices in the U.S. would likely rise, ultimately negatively impacting its own domestic economy.

Let’s consider Crude Oil. Oil accounts for nearly 1/3 of Canada’s exports to the U.S., and energy makes up a significant portion of the Canadian equity market. While tariffs would obviously hurt the Canadian economy and its stock market, Canadian oil represents around 20% of U.S. oil consumption, and without clear alternatives, oil prices in the U.S. would likely rise, ultimately negatively impacting its own domestic economy.

The trade-offs of imposing tariffs suggest this development may be part of an early negotiation strategy. Notably, President Trump proposed these tariffs with the explicit aim of pressuring Canada and Mexico to enhance their border security.

In 2019, Trump threatened to escalate tariffs on Mexican imports unless the country took measures to curb illegal immigration. Mexico responded by deploying additional border troops, thereby avoiding the tariffs. A similar scenario may lie in front of us.

Markets have largely shrugged off the tariff threats. The Canadian stock market has marched higher, while the Canadian dollar has pared back some of its losses following the announcement.

Source: The Economist

Still, the Canadian Dollar remains near multi-year lows, reflecting stronger U.S. economic growth and expectations that U.S. interest rates will eventually settle at higher levels than in Canada.

Canadian equities proved resilient during Trump’s first term despite the imposition of steel and aluminum tariffs. Between 2018 and 2019, Canadian stocks outperformed other non-U.S. developed markets, as tariff-exposed industries represented only a fraction of the market.

The Canadian equity market may be more insulated from the impact of tariffs than its own economy.

Sectors such as financial services, software, and food retail are not directly exposed to tariffs as they do not rely on physical exports. An increasing number of Canadian companies that make up its stock market have diversified their businesses internationally, reducing their sensitivity to economic developments at home.

Sectors such as financial services, software, and food retail are not directly exposed to tariffs as they do not rely on physical exports. An increasing number of Canadian companies that make up its stock market have diversified their businesses internationally, reducing their sensitivity to economic developments at home.

This stands in contrast to the thousands of small and medium sized private businesses that make up its economy and may be more directly exposed to domestic issues in Canada.

In closing, while the proposed tariffs are not a completely empty threat, any impact may be less punitive than some may expect.

This development has served as a reminder that the new U.S. administration may introduce greater unpredictability, potentially adding to market volatility from time to time.

This may create risks to consider going forward but can also create opportunities as short-term dislocations arise.

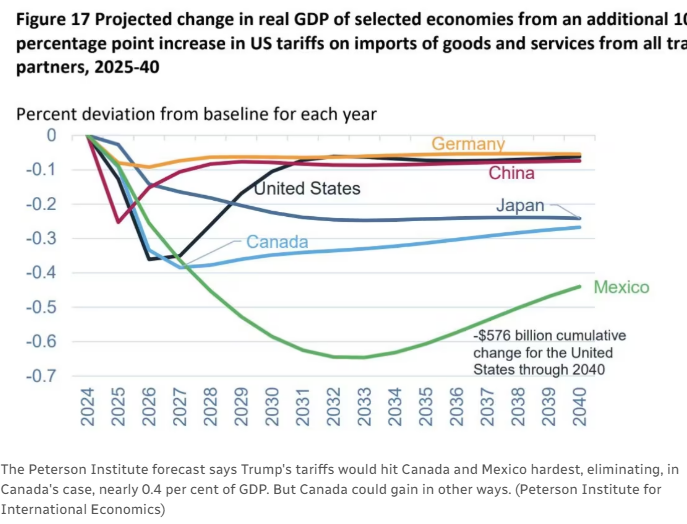

Source: CBC

Irrespective of how things ultimately unfold, 2025 promises to be interesting.

As always, please let me know if you have any questions or comments.