Good Morning,

Potential changes to U.S. government policy are an increasing area of investor focus, but it can be easy to lose sight of the forest for the trees.

With the incoming Trump administration and potentially new policy initiatives, let’s discuss how to approach analyzing these measures.

Here is a break-down of Trump administration proposals:

- How much of the economy does the proposal touch ?

- What sort of change is being proposed—is it different from current policies or is it just a difference in degree from what has already in place ?

- How durable is the impact ?

- Are there offsetting forces?

- Is the administration able to modify policy parameters based on the policy’s effect?

The proposals that get the biggest headlines—such as tax cuts and tariffs—may not be that consequential. Others, meanwhile—such as the Department of Government Efficiency (DOGE) and immigration policies—could have a bigger short-term economic bite.

President-elect Donald Trump’s proposed tariff regimes are certainly broad. They will likely apply to every import into America. Retaliation by trading counterparts means that U.S. exports will likely be impacted as well, so tariffs are certainly meaningful in scope.

But they’re hardly new.

At its core, a tariff is just a tax designed to change consumer behavior. Anyone who has ever bought a pack of cigarettes or a bottle of wine is quite familiar with the concept. The difference between a tariff and other forms of behavior-modification taxes is simply the political goal—import substitution versus public interest. Nor are any changes likely to be written in stone.

Even on the campaign trail, Trump was floating wide-ranging tariff proposals. Since Republicans control the machinery of lawmaking, it seems very likely that the White House will have both the ability and willingness to modify tariff levels as conditions change on the ground.

As I have discussed in the past, tariffs don’t appear that risky—they’re a well-known tool that is easy to modify, offsetting the breadth of their application.

Debt-funded tax cuts are a similar case.

Higher budget deficits are very likely to add to inflation in the near term, and unlike tariff levels, tax rates are difficult to change on the fly.

That said, it is extremely difficult to contend that a budget deficit is something new for the U.S. economy. More importantly, fiscal policy doesn’t exist in isolation.

The U.S. Federal Reserve can help offset any inflation with higher interest rates, and the U.S. economy also dynamically adjusts to rising prices, with consumers and producers changing behavior in response.

These adjustments won’t be painless for the economy or investors, but they are part of the normal evolution of background macroeconomic conditions.

Because of familiarity and ease of offset, budget deficits are likely manageable.

Two areas of policy change that look potentially more challenging in the short term are immigration and the DOGE. If the Trump administration reduces the undocumented population of the U.S., it wouldn’t be unprecedented.

Pew Research Center estimates show multiple years of decline in the recent past. The largest prior episode coincided with declining U.S. labor demand because of the global financial crisis.

Policies that prioritize immigration enforcement over labor supply are rare, particularly at a time of approximately 4 % unemployment.

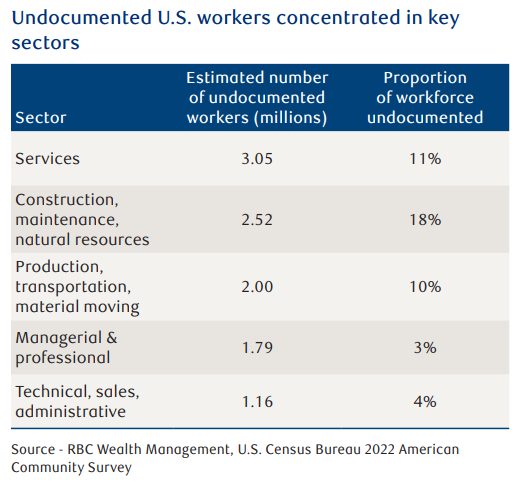

There are also few natural economic offsets if the administration were to dramatically reduce the roughly 5 % of the workforce that is undocumented. Given the existing lack of available workers, wages would likely rise, an important inflationary precursor.

With nearly 18 % of the construction and agricultural supply chain workforce lacking work authorization, according to U.S. Census Bureau data, there are risks of disruptions in the housing and grocery sectors.

Fed interest rate hikes could help with some of the wage-driven inflation, but they are largely ineffective against supply-driven price hikes. It would be politically difficult for the administration to reverse course.

Fed interest rate hikes could help with some of the wage-driven inflation, but they are largely ineffective against supply-driven price hikes. It would be politically difficult for the administration to reverse course.

All in all, this makes immigration an area to watch for investors under our framework—a novel proposal, with high impact on key sectors, and with limited available course corrections.

If the DOGE succeeds in increasing government efficiency—achieving the same outcomes using fewer resources—that’s almost certainly both a long- and short-term economic win – at least according to Trump !

In all seriousness, there are few economic concepts more powerful than efficiency. Based on public comments, it strikes us that the DOGE may not be looking to keep outcomes constant and is instead looking to cut government programs and employees. Whether that will pay off in the long run depends on the details, but in the short term, it looks to be an area for investors to watch.

Large cuts to government services, if that is what happens, are rare in the U.S., and they would touch a sector that directly contributes roughly 20 % of U.S. GDP and indirectly impacts most of the economy.

Even within the Trump administration’s likely policy mix, there are forces that could pull in different directions.

Shrinking the government is likely to limit short-term growth and could help with inflation, while debt-funded tax cuts likely provide a fillip to economic activity. More broadly the new administration as likely to propose and execute on a wide range of different policies.

A useful framework to approach these changes is looking at the magnitude and durability of their impacts. Time will tell if they will be potential game changers.

As always, please do not hesitate to reach out if you have any questions.