The last two-week period in markets has been one that has been characterized by a spike in volatility and the panic that typically comes when equity markets correct themselves. The main driver behind this recent bout of volatility has been concerns that the U.S. economy is nearing recession, and it is important to note that at present economic data out of the US is indicating a slowdown in growth – not outright recession. There are several reasons for why the panic that recently set in is likely unfounded and has dissipated throughout the week:

-

Corporate earnings in the U.S have overall been relatively strong. Aside from several earnings and revenue misses (i.e., Disney and Intel), most S&P 500 companies’ earnings in Q2 have held in line with an economy that remains growing – albeit at a slower pace.

-

Analysts’ estimates have remained relatively close to the reality in the economy. Moreover, the expectation for the broader equity market is for revenue growth to continue to persist.

-

Across the board, management teams in their Q2 calls to investors have maintained a balanced tone highlighting the headwinds their businesses face but have also not sounded the alarms on any significant macro economic concerns.

-

Earnings growth rates are also expected to become more balanced, which means that non-Magnificent 7 stocks are finally expected to improve after a long period of weakness. There remains substantial value in positions outside of the AI/tech trade.

-

The Chicago VIX Index (commonly known as the ‘fear gauge’) spiked on Monday rising four-fold from where it was at the beginning of July. It is important to note that volatility in the U.S. market has been extremely low for the last several months going back all the way to November 2023. From a technical perspective, a spike in the VIX of this magnitude is a contrary indicator for market performance. Historically the market has rallied after such a period of volatility.

I strongly recommend taking the time to review our most recent piece on this front Stock market selloff: A "growth scare," or more? The piece delves deeper into the concerns that drove this most recent sell-off and the arguments for why maintaining a neutral strategy in your portfolio is ideal. For the long-term investor there are opportunities to enter positions at a relatively attractive cost base, for those of you who still have some cash on the sidelines.

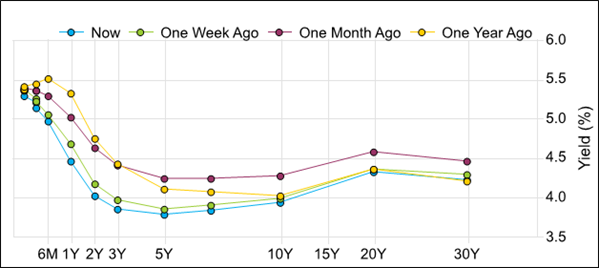

It is also important to appreciate that fact that a well-balanced portfolio has likely protected you during this recent period of volatility. Fixed income markets have been equally impacted however with an inverse effect, as yields on bonds across the curve. For example, U.S. government short- and medium-term bond yields have declined to their lowest level in over a year (see below)

Government Yields - US Report as of 09 Aug '24

Sources: FactSet Interest Rates, Tullett Prebon Information, *SWX Swiss Exchange

This decline in yields has resulted price increases across the curve for existing bonds both in the U.S. and abroad. For those of you who hold short-term bonds in your portfolio you would have noted the value of these positions have increased meaningfully over the last month.

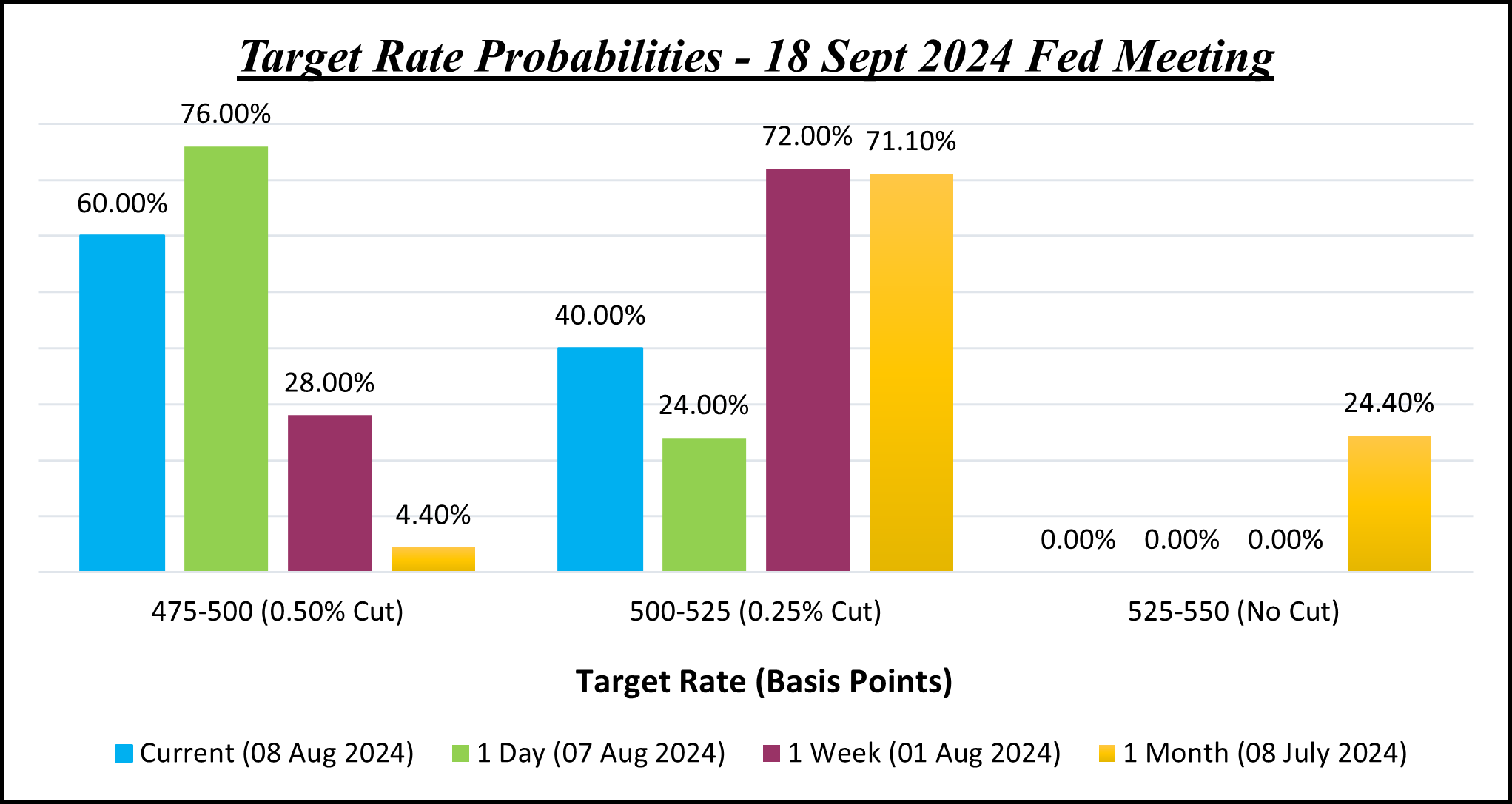

Finally, another indicator as to the direction of rates and the overall concern for the U.S. economy is the expectation for rate cuts by the Fed in September. It is important to note that the Fed has yet to cut rates, which is an impactful monetary policy tool for spurring economic growth. However, on Monday the probability of a 0.50% rate cut in September grew to 100% - a month ago that probability was sitting at 4.4%. The reason for fixed income markets anticipating a larger rate cut was concerns over the U.S. economy. Fast forward to Friday and the market is now pricing in the probability of a 0.50% rate cut in September at 60.00% and this has consistently declined since Monday, as fixed income markets begin to price in a higher probability of a 0.25% rate cut in September instead – a key indicator that markets see the initial concerns from last week were likely overexaggerated.

Source: FactSet

| Summary Though the U.S. economy is undeniably slowing down, a decline in the strength of the labour market was exactly what the Federal Reserve was looking for when it came to ensuring inflation maintained it’s downward trajectory. Market volatility such as this is precisely why a well diversified portfolio will always keep you protected from significant downside risk in the short-term. For those of you who may have significant concentrations in AI and tech stocks, over the next several weeks repositioning your exposure to other sectors would be ideal. It’s important to note here that AI/tech trade is far from over, and we currently see these positions as being oversold – but any cash on hand at this time I recommend be allocated to positions that remain value buys and will benefit from the anticipated balancing of earnings growth in U.S. equities. For more on what we expect in the week ahead, please read our most recent Forward Guidance: Our Weekly Preview - RBC Economics If you or anyone you know would benefit from having a review of their portfolio and would like to understand the strategies we implement here at RBC Dominion Securities, please connect with us here. |