Western media have been focusing their geopolitical coverage on a potential “imminent Russian invasion of Ukraine”—repeating and amplifying strong statements and warnings of leaders in the U.S. and other countries, and setting and then resetting potential “invasion” dates.

This has impacted energy markets for the past two months, boosting crude oil and European natural gas prices. More recently, financial markets have started to take notice, as war-related headlines have contributed to equity market volatility.

We think the issues at stake are much greater, wider, and deeper than the conflict between Russia and Ukraine, and go back decades.

From our vantage point, the crux of the dispute is between the U.S./NATO and Russia. It’s about spheres of influence between major military powers, NATO’s expansion eastward and involvement in the former-Soviet space since the end of the Cold War, deployments and flight times of advanced missile systems, locations of short- and intermediate-range nuclear weapons, energy sector competition, and more. We think the ultimate outcome of the dispute could establish European security parameters for decades to come.

There are certainly scenarios in which Russia and Ukraine could clash militarily—we address the most likely one below, in eastern Ukraine.

Regardless of what occurs in Ukraine, Russia is focused on the bigger issues surrounding its conflict with the U.S. and NATO as it pertains to security in Europe, as evidenced by the formal security proposals Moscow gave to those two parties in December 2021, and the diplomatic full-court press that has taken place since then.

Diplomatic initiatives and dialogues are ongoing between the U.S./NATO and Russia, and leaders from the UK, France, Germany, Hungary, and Turkey have also engaged. Meaningful progress has not yet materialized.

The Russian ruble has become a proxy for the current geopolitical risks

The ruble has been weak recently, and is at the upper end of the broad range that has been established since late 2014 when tensions began to escalate with the U.S. and sanctions started being imposed with greater force.

The chart shows the cross exchange rate for the U.S. dollar to the Russian ruble (USD/RUB) from 2010 to present. From 2010 through much of 2014, the Russian ruble traded in a range of about 27 to 34 against the U.S. dollar, as measured by the USD/RUB cross exchange rate (the lower the level, the stronger the ruble; the higher the level, the weaker the ruble). However, when geopolitical tensions began to heat up between the U.S. and Russia regarding Ukraine, the ruble weakened significantly. From late 2014 to date, it has traded in a broad range of 50 to almost 83. With the latest bout of geopolitical tensions, it is trading at almost 77, the higher end of that range.

Note: The higher the level in the chart above, the weaker the ruble.

Source - RBC Wealth Management, Bloomberg; data through 2/14/22

Russia recently said its primary concerns about security guarantees are still not being addressed: the non-expansion of NATO, the non-deployment of strike weapons systems near Russia’s borders, and a return to the 1997 configuration for the deployment of foreign forces, equipment, and weapons on the territories of countries that were not NATO members at that time.

While we see scope for a few more brief rounds of discussions—Russia is currently in the process of finalizing another substantive diplomatic document for the U.S. and NATO—the clock is ticking on the diplomatic front.

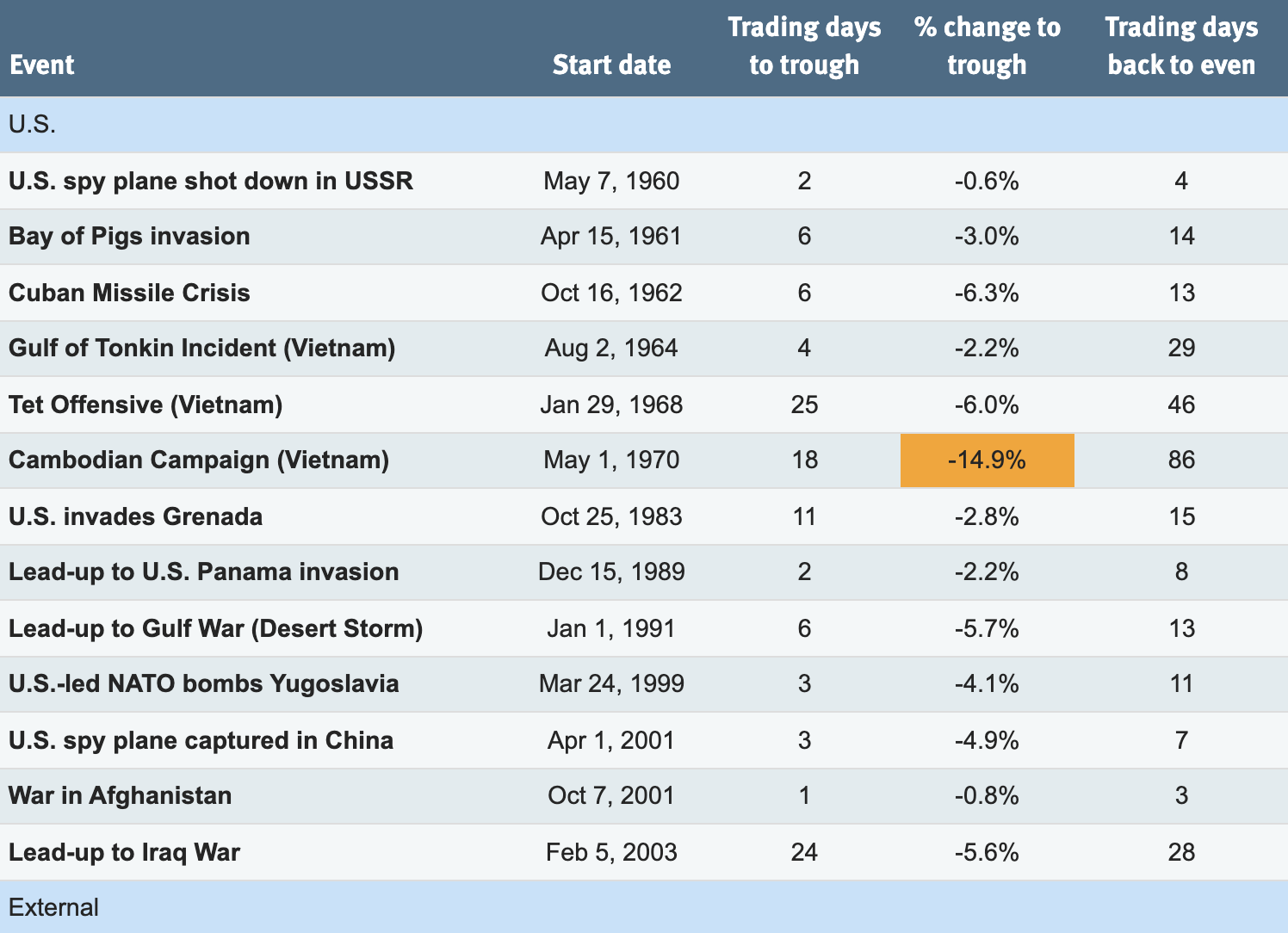

Markets tend to bounce back even in the face of serious hostilities and wars

Before looking at one of the specific military risks in Ukraine surrounding this complex geopolitical situation and related sanctions risks, it’s important to consider the market’s past performance during previous wars and high-stakes confrontations.

Historically, military clashes have had limited impact on equity markets both in magnitude and duration—even when the U.S. and Soviet Union were embroiled in the Cuban Missile Crisis.

The S&P 500 fell 6.2 percent, on average, in 18 major post-WWII military conflicts or hostilities that we evaluated. That nearly matches the decline the market suffered when U.S. President John Kennedy and Soviet Premier Nikita Khrushchev were at the brink of war.

While that level of decline is nothing to dismiss, it’s well within the bounds of a typical, modest pullback in many scenarios that often confront markets, including those that have nothing to do with military risks.

Our study of previous geopolitical conflicts indicates the market’s reaction lasted an average of only 30 days before it was able to climb back to even. This occurred despite the fact that many of the actual events lasted longer—sometimes much, much longer.

S&P 500 responses to select acts of war or hostilities since World War II

* Other economic and monetary policy factors negatively influenced the number of days it took the market to get back to even; this is not counted in the average number of trading days back to even.

Source - RBC Wealth Management, RBC Global Asset Management, Wikipedia, National Security Archive at George Washington University, U.S. Naval Institute; data attempts to capture any pre-event impact

At times equities weakened during the run-up to a geopolitical conflict as tensions mounted, and at other times the weakness began with direct military clashes. In most instances, markets recovered soon after hostilities began.

However, as the table above shows, four prior events were more difficult for the market to absorb, with the S&P 500 declining in the low-to-mid-double digits. In these instances, which are highlighted in orange, two of the four acts of war were in the Middle East: in 1990 when Iraq invaded Kuwait and seized its oilfields, and back in 1973 during the Yom Kippur War and Arab oil embargo.

What’s notable about these two events, as it pertains to today’s geopolitical risks, is that those conflicts impacted global energy markets. The geopolitical risks surrounding the U.S./NATO and Russia conflict do not directly put oil and natural gas supplies at risk at this stage (unless the West sanctions Russian oil and gas, or Russia restricts supplies in counter-sanctions). But European natural gas prices could be vulnerable to further increases if the West follows through with its threat to stop the Nord Stream 2 pipeline from becoming operational should Russia and Ukraine clash directly.

In general, when it comes to wars and serious geopolitical disputes, our long-standing advice is that investors should assume that such events can push the equity market into a temporary five percent to 10 percent pullback or, in rarer cases, into a longer-lasting correction of greater magnitude—especially when energy markets are widely affected such that they put medium- and long-term economic growth at risk.

Donbass: The region that could be a flashpoint

Currently, the area of greatest tension within this wider U.S./NATO and Russia dispute is the Donbass region of eastern Ukraine, where the Armed Forces of Ukraine and the military forces of the self-proclaimed Lugansk and Donetsk People’s Republics (LDPR) have been facing off for nearly eight long and painful years. If fighting escalates in Donbass (or occurs anywhere else in Ukraine), we think equity markets would be vulnerable to at least a short-term pullback.

Donbass is a dispute in which the U.S., other NATO countries, Russia, and Belarus have had vested interests from day one.

The internal conflict began soon after the Euromaidan (Maidan) protests and related events in February 2014 led to the ousting of Ukraine’s president and administration, which were friendly toward Moscow. Russian-speaking Ukrainians in the Donbass cities of Lugansk and Donetsk and surrounding areas opposed the abrupt change in government and the new direction of the country. Following self-determination referendums, they declared their independence from Ukraine in May 2014. Their independence was not recognized by Ukraine, Western nations, Russia, nor Belarus; however, a process has recently been put in place by which Russia could formally recognize them.

One side of the dispute (including every Ukrainian leader since the uprising and Western officials) considers Maidan to be a “revolution of dignity” and an important pivot by Ukraine toward independence, democracy, freedom, and liberal Western values and culture, with the potential for further EU and NATO integration down the line upon implementing various reforms. Ukrainian nationalism has been encouraged and promoted during the post-Maidan period.

The other side (including LDPR and Russia) considers Maidan to be a Western-backed coup d’état aimed at turning Ukraine into an externally controlled state in order to disrupt fraternal relations between Russia and Ukraine, suppress Ukraine’s large Russian-speaking population, and upend Ukraine’s historical culture—with the ultimate goal of destabilizing Russia’s national security due to the involvement of NATO and some of its member states in post-Maidan Ukraine.

At times the fighting in Donbass has been full on, especially in 2014 and early 2015. At other times it has been less intense but with regular shelling of villages and drone and sniper attacks, and there have also been periodic cease-fires, albeit not very effective ones. The UN estimates up to 13,300 people have died during the clashes since they began in April 2014, with at least 25 percent being civilians, including children and the elderly. Currently, a state of cease-fire technically exists, but there are regular violations and the situation is now extremely tense.

In February 2015, Ukraine, LDPR, Russia, and the Organization for Security and Co-operation in Europe (OSCE) jointly signed the Minsk agreements, which lay out a step-by-step process to end the fighting and restore the non-recognized republics as part of Ukraine, with special status. But none of the steps have been implemented thus far. The likelihood the Minsk agreements will remain in force has diminished in recent months. Progress at the most recent negotiations in the Normandy Four format (France, Germany, Russia, and Ukraine) on February 10 was nonexistent.

Currently, an estimated 130,000 Ukrainian troops, including combat-ready formations with heavy artillery and tanks—with nationalist battalions among them—are deployed near the contact line (demarcation line) that runs between Ukraine- and LDPR-controlled areas of Donbass. Weapons from NATO countries continue to flow to the Armed Forces of Ukraine. At least 43 cargo flights landed in Ukraine with weapons and other military equipment from January 15 through February 13, according to flight monitoring systems.

On the other side of the contact line, the Armed Forces of Donbass (LDPR’s joint military) now have 150,000 troops available. This contact line is only 100 kilometers west of the Ukrainian-Russian border. Russian troops and heavy equipment are located on Russian territory about 200–400 kilometers east of that border. (Additionally, Russia is conducting major military exercises in other parts of its territory, in the Black Sea and Sea of Azov, and in Belarus with the Belarusian Armed Forces. Exercises in Belarus are scheduled to end on February 20, and some of these troops have already begun their pre-scheduled process of returning to their permanent deployment locations in Russia.)

If the major population centers of LDPR, including the cities of Lugansk and Donetsk, come under threat from an offensive by the Ukrainian Army or nationalist battalions, one of the two LDPR leaders recently told Reuters he may ask Russia for military support. Roughly 3.66 million people live in LDPR, 860,000 of whom have become Russian citizens since April 2019 when a special simplified procedure was established, and more are in the queue.

The West promises punitive sanctions, but there are mixed signals

Officials in the U.S., other Western countries, and EU structures have repeatedly stressed that any actions by the Russian military in Donbass or anywhere else in Ukraine—even if limited—would be considered an “invasion” of Ukraine, and would trigger harsh, punitive economic sanctions against Russia.

Thus far, the hundreds of sanctions—some small, others large—that the U.S. has imposed against the Russian state, its businesses, and certain citizens since 2014, and the related sanctions by the EU and UK, have constrained the Russian economy and weakened the ruble notably. But overall, they have had a limited detrimental impact as Russia has achieved greater self-sufficiency and development of certain sectors during this time, especially in agriculture.

If the situation in Ukraine escalates militarily and Russia intervenes, U.S. senators are promising a much bigger response—legislation vividly characterized as the “mother of all sanctions” or “sanctions from hell” with the goal of isolating and effectively blockading the Russian economy.

The mere threat of this and the heightened tensions in Donbass dented the Russian stock market. Its main index, made up largely of natural resource companies and banks, plunged 25 percent from its October 2021 peak to its January 2022 trough—despite the fact that crude oil and natural gas prices rallied sharply during the same period.

Russian equities have corrected sharply since geopolitical tensions began to heat up

S&P 500 and MOEX Russia performance since 2019 (%)

The chart shows the performance of the S&P 500 and MOEX Russia indexes since January 1999. The two largely moved in tandem, and both were up by about 75% in early October 2021. Soon thereafter, MOEX Russia began to decline as geopolitical tensions began to heat up and then dropped further in early 2022. While the S&P 500 has also pulled back in 2022, its recent decline has been more moderate. Taking into account these moves, the MOEX Russia index is now up 46.9% as of February 14, whereas the S&P 500 is up 75.6%.

Source - RBC Wealth Management, Bloomberg; indexes measured in local currencies; data through 2/14/22

Thus far, there have been mixed signals about just exactly which types of sanctions the West would impose—with some officials threatening to cut off Russia from the international financial payments network known as SWIFT, and others saying that move would be too risky for the global financial system and Europe’s economy. Recently, Western officials have delivered a more consistent message about potential harsh sanctions on Russia’s largest banks, including restricting them from dollar-based transactions.

There have been similar mixed messages related to Russia’s oil and gas and agriculture sectors, with some preferring to avoid sanctioning these areas due to the potential boomerang effect on Western economies, particularly during this inflationary period.

Most Western officials, including more recently some German officials, have threatened that the Nord Stream 2 pipeline would not be allowed to become operational if Russia intervenes militarily in Ukraine. However, the EU’s chief diplomat Josep Borrell recently said that even if the pipeline were to be halted due to a war between Ukraine and Russia, “it doesn’t mean that Nord Stream 2 will stop working forever.” Russia points out that the construction of the pipeline itself has already been paid for due to relatively high gas prices. Furthermore, in recent years Russia has signed contracts with China that can supply more pipeline gas than Nord Stream 2, and another potential pipeline project is being considered that is almost as large as Nord Stream 2.

Suffice it to say, we think it’s safe to assume that a package of punitive sanctions from the West would be just that—punitive—and would damage the Russian economy, at least in the short run.

Russia would likely respond to sanctions symmetrically and asymmetrically

For financial markets, we think widespread sectoral sanctions raise uncertainties and risks because of the intricate linkages in the global financial system and supply chains, and due to Russia’s dominance in natural resource and agriculture markets.

While Russia’s economy is no match for that of the U.S. or Germany, and is smaller than Italy’s, it is the fifth-largest in Europe based on GDP in U.S. dollars. On a purchasing power parity basis—which incorporates currency exchange rates—it is the sixth-largest economy in the world, according to the World Bank.

Russia’s economy is the 11th-largest in U.S. dollar terms, but the sixth-largest in PPP terms

Note: Ranking based on 2020 GDP data. Purchasing power parity takes into account the influence of exchange rates.

Source - RBC Wealth Management, World Bank

In addition to consistently being a top-three global producer of crude oil, related petrochemical products, and natural gas, Russia is among the three leading producers of wheat, barley, aluminum, gold, platinum, diamonds, and wood products. Moreover, it is a top-six producer of titanium, iron ore, steel, and coal, as well as potash, nitrogen, and phosphate used for fertilizer production. It also has large reserves of rare-earth minerals.

In the past, Russia has responded to Western sanctions by symmetric and asymmetric means. Thus far, there have been little-to-no hints from the Russian government about counter-sanctions or actions it could potentially impose, although on multiple occasions officials have stressed that they view Russian companies’ commercial energy supply contracts with Europe as nearly sacrosanct.

These contracts are long-term in nature and are not highly impacted by fluctuations in European natural gas spot market prices, but some do have exposure to market-based crude oil prices. The contracts are important to Russia’s economy and, after all, Russia’s grievances are mostly with the U.S. government and the NATO military bloc, not individual Western and Central European countries or their European commercial partners. Countries that do not have long-term contracts with Russia, such as Poland, would be at the mercy of natural gas spot market prices.

Overall, European economies could be more detrimentally impacted by Western sanctions and Russia’s counter-sanctions than those in North America due to Europe’s stronger trade and investment ties with Russia. RBC Capital Markets points out, however, that Europe’s trade exposures—goods exports (shown in the first chart below) and services exports—are not particularly large. Foreign direct investment by the euro area into Russia is also relatively moderate, as shown in the second chart below.

Central European goods exports are most exposed to Russia, but even this exposure is not significant

Major economies’ goods exports to Russia (as a percentage of exporter GDP)

Among the major economies with goods exports to Russia, the Czech Republic is most exposed, followed by Hungary at 1.5% and 1.4% of exporter GDP, respectively. The euro area as a whole has 0.5% exposure. Among the other 12 countries listed, the exposures are as follows: Poland 0.9%, Turkey 0.8%, Korea 0.7%, Ireland 0.7%, Germany 0.6%, Austria 0.6%, Italy 0.6%, Malaysia 0.5%, Belgium 0.4%, Netherlands 0.4%, Sweden 0.4%, and France 0.4%.

Source - RBC Capital Markets, Bloomberg, Haver Analytics, International Monetary Fund; data based on the sum of Q4 2020 to Q3 2021

The euro area’s direct investment into Russia is moderate

Major economies’ foreign direct investment (FDI) into Russia (stock, as a percentage of country investor’s GDP)

The chart illustrates the countries and region with the highest levels of foreign direct investment in Russia. The order is as follows: Netherlands 4.0%, euro area 2.1%, Switzerland 1.8%, Austria 1.4%, UK 1.3%, Ireland 1.2%, Singapore 1.1%, France 0.8%, Hong Kong 0.5%, Sweden 0.5%, Germany 0.5%, Hungary 0.3%, Belgium 0.3%, Turkey 0.2%, and Italy 0.2%.

Source - RBC Capital Markets, Bloomberg, Central Bank of Russia, Haver Analytics; data as of the end of June 2021

Russia’s pivot toward Asia likely to accelerate, regardless of what happens with the West

In a scenario of harsh sanctions, the level of isolation that Russia might face is uncertain because in recent years the country has pivoted its economy more toward Asia, particularly China. Some prominent Russian economists believe punitive sanctions would hasten the country’s long-discussed internal development plans, including the building of new southern Siberian agglomerations (scientific-industrial and economic centers) and development of its Far East region. In other words, if severe Western sanctions are imposed, Russia’s internal development and Asia pivot would likely accelerate sharply.

Given Russia’s low government debt and significant reserves, it has the financial wherewithal to pull off such a development strategy, but it would require significant and laborious restructuring of its current economic policies and, perhaps, a reconfiguration of its central bank mandates. The proposals are already in the works—and a number of key officials and thought leaders recommend this direction regardless of whether ties with the West are damaged further.

Along the lines of an eastern pivot, one thing to pay attention to is China’s reaction to the ongoing U.S./NATO and Russia geopolitical dispute, and how it would respond if sweeping Western sanctions are imposed against Russia.

On February 4, following discussions between President Xi Jinping and President Vladimir Putin ahead of the Beijing Olympics opening, China’s official readout of the meeting stated, “The two sides need to keep up their close high-level exchanges, follow their four-point agreement on firm mutual support, strongly support each other in upholding sovereignty, security and development interests, effectively counter external interference and threats to regional security, and maintain international strategic stability.”

Equity market vulnerability is typically limited and short-lived

The risks in Eastern Europe, and those associated with Ukraine more specifically, become more understandable when viewed through the wider lens of the ongoing geopolitical dispute between the U.S./NATO and Russia.

This is not a conflict that developed just recently or even in the past few years. It began decades ago, while NATO expanded eastward and became more involved in the post-Soviet space. Things are now coming to a head.

There is still scope for a diplomatic resolution, and all parties are engaged including European nations, which, in addition to Russia, have the most at stake. But we think time is of the essence. Russia has repeatedly stated it is not interested in lengthy negotiations that fail to address its primary security concerns.

As we have demonstrated, there are risks that fighting could break out in Ukraine before a diplomatic resolution occurs, particularly in the Donbass region, with tensions between the Ukrainian Army and LDPR close to a boiling point.

Because of these uncertainties, we think equity markets remain vulnerable to heightened volatility and downside, and energy markets susceptible to upside pressures, as events unfold. But if history is a guide, the risk associated with wars and geopolitical conflicts for equities is usually limited in magnitude—to around five percent to 10 percent downside for major developed markets—and typically plays out over a brief time frame. Somewhat deeper corrections have been associated with events that meaningfully disrupted energy markets, weighing on economic growth.

At this stage, we do not recommend adjusting long-term portfolio allocations due to these geopolitical risks, which seem to be shorter-term in nature and could be resolved in coming weeks or months, one way or another. But investors should be mindful that the broader U.S./NATO-Russia dispute, and related events in Ukraine, could create volatility or downside for equities over the near term.