Given that so many people are talking about it, I thought you may find of interest why I anticipate a near term levelling off or possibly decline in the coming months in the price of precious metals (and am reducing their allocations in my portfolios from 10% to under 5%).

The reason is simple – If someone is looking to maintain the purchasing power of their savings, but does not want to take the risk that comes with investing in stocks or corporate bonds, they only really have a few options. They can hold/deposit their cash for a small interest payment or buy government bonds.

However, if the interest paid on these savings or on the bonds is lower than the rate of inflation, than the purchasing power of their savings declines. Why? Because if the purchasing power of cash declines by 2% a year, but you only receive 1% interest payment on your savings, you are de facto losing 1% of your purchasing power a year.

When that is the case, the savvy investor knows that it is preferable to own gold, which is widely believed to maintain its purchasing power in all economic environments (a zero percent return is better than a negative return).

So what do investors anticipate when it comes to future rates of inflation? For the past few decades, according to research by the Federal Reserve, investors generally anticipated future inflation rates of 1.5%-3% on average per year.

Source: https://fred.stlouisfed.org/

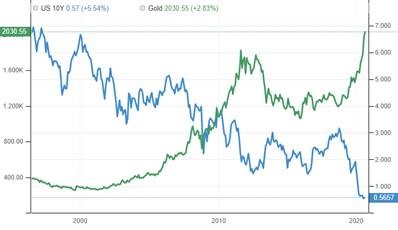

So whenever long term returns on government bonds went below anticipated future rates of inflation, investors understood that it was more worthwhile to hold gold over cash or bonds. The chart below shows that gold prices began an accelerated increase when bond yields got close to the 3% level. Gold prices soared when government bond yields hit 1.5% when inflation was expected to be around 2.5%-3%. This means that the market anticipated a negative 1%-1.5% real return on 10-year government bond in tandem with the peak in gold prices between 2010-2012.

Source: https://tradingeconomics.com/

The same movie just played again over the past few months. In particular though, in June 2020, when it became clear world economy would not enjoy a quick return to economic normality, the yield on the US 10-year government bond dropped to 0.5%, a level never seen in history. However, inflation expectations haven’t shifted much from the average we have seen over the past few decades of around 1.5%-2%. This means that the real return for investors in 10 year US government bonds was anticipated by the market to be negative -1.0%, or a loss of 1% in purchasing power every year for the next 10 years. This helps clarify, in my opinion, why gold prices soared when they did.

However, as economies begin to get closer to normality and the enormous government stimulus programs continue to support businesses and consumers over the coming months, I believe that there is likely to be good enough economic data that will bring the 10-year yield up significantly from its historic lows. And if that’s the case, we will likely see gold (and silver) prices fall as a result.

However, it doesn’t mean that we have seen the top in precious metal prices. I believe though that in order to see precious metals prices move significantly higher from here, we will need to see the Federal Reserve publicly commit to keep long term interest rates below long term inflation expectations. That will be the signal to begin buying gold and silver again. Until then, I believe that we have likely seen or are likely to see the top in prices very soon.

I hope this makes sense. Happy to chat further on this topic. Feel free to email me or call: 416-699-4057