-

Overnight rate held at 0.25% (no “micro cut”)

-

QE continuing at $4 billion per week

-

Growth forecasts revised higher beyond current quarter

There was some speculation that the Bank of Canada would start the year with a “micro cut” (lowering the overnight rate from 0.25% to something like 0.1%) amid near-term downside risks from extended lockdown measures, as well as some recent tightening in financial conditions including a stronger Canadian dollar. But as we expected, the BoC opted against such a policy tweak as a more optimistic medium-term outlook combined with ongoing fiscal support reduced the need for additional monetary policy stimulus. The Canadian dollar’s rise was attributed to higher commodity prices (reflecting improving economic prospects) and a broadly weaker US dollar, though Macklem noted further appreciation could weigh on Canada's exports.

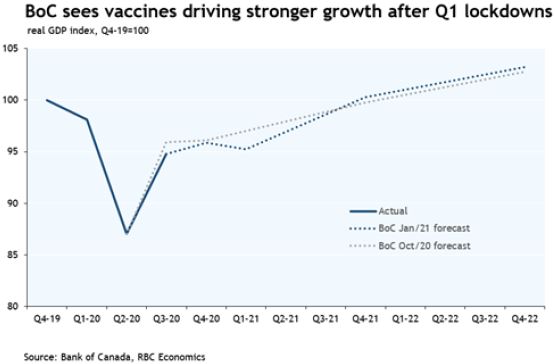

The bank’s more optimistic medium-term forecasts are the key takeaway from today’s policy statement and MPR. Compared with the BoC’s October 2020 forecasts, faster-than-expected vaccine rollout (notwithstanding recent shipment delays) and easing of containment measures is expected to result in a more significant pickup in GDP growth as 2021 progresses. Even with current lockdowns making for a sluggish start to the year (Q1/21 GDP expected to decline by 2.5% annualized) the BoC upgraded its 2021 forecast (on a Q4/Q4 basis) to 4.6% from 3.8%. 2022 growth (again Q4/Q4) is still expected to be close to 3%. These forecasts assume the most severe restrictions that have been put in place recently will be eased in February, and vaccine rollout will lead to “broad immunity by the end of 2021.” Uncertainty is still elevated but the outlook beyond the near term is now “stronger and more secure” than it was in October.

The hawkish implications of these forecast revisions were offset by the BoC lifting its assumption for potential GDP—the economy’s speed limit. As a result, the economy still isn’t seen reaching full capacity (with sustained 2% inflation) until 2023. According to the BoC’s forward guidance, rates will remain low until then. More immediately, Governing Council said the pace of government bond purchases will be “adjusted as required” as it “gains confidence in the strength of the recovery.” We continue to think reduced government borrowing in the upcoming fiscal year will mean less BoC bond-buying is needed to keep rates low. In his press conference, Governor Macklem noted any QE tapering will be gradual and the program will be needed for some time.

“Change is inevitable. Growth is optional.” ~ John Maxwell