Good day everyone.

Last week equity markets displayed some significant volatility, with the VIX (a volatility index) reaching levels not seen since Covid in March of 2020. While I continue to have high conviction in your portfolios , and for most of us this is not our first rodeo, I do acknowledge that these periods can be nerve racking. As such, Kelly Bogdanova from the Portfolio Advisory Group at RBC Dominion Securities, has published a nice article outlining where we are and how we think markets will unfold in the near term. The full article (PDF) is attached for you, and for those of you looking for a shorter read I’ve abbreviated the key points below for your convenience, along with a few charts.

Enjoy.

Shock and Tariff

Big tariffs are indeed a big challenge, both for economies and stock market investors. As of this writing, the S&P 500 Index is roughly flat during intraday trading on Monday, and has fallen 13.6 percent year to date and 17.2 percent from its all-time high in February.

During such periods of extreme volatility and steep drops in stock prices, there is a reasonable temptation to make drastic asset class or sector changes to investment portfolios. We think it’s best to avoid this.

The U.S. stock market and other major markets have ultimately overcome many challenges in the past—including extreme challenges—and we believe they will this time too.

From our vantage point, some of the best companies in the world are headquartered in the United States. We believe they will be able to adapt to Washington’s policy decisions.

Importantly, we believe Washington’s policy decisions will adjust to the realities on the ground, so to speak. In other words, we think Washington will be forced to contend with the realities of the market selloff, the associated economic risks, and public opinion—the latter of which should not be underestimated. The U.S. investor base is broad, and investors vote.

Is this correction different?

This correction is absolutely different, in our opinion, especially considering the global paradigm shift. Also, the plunge has been sharper and quicker than the average historical correction.

U.S. officially hiked tariffs on April 2 to a level not seen in more than 100 years, exacerbating stagflation and recession risks for the U.S. economy and generating significant uncertainties about medium- and long-term trade relations.

But we think it’s important for investors to keep in mind that stock market corrections are inherently almost always “different” from those in the past.

- Since 1928, the S&P 500 has experienced 103 corrections of 10 percent or more and 27 corrections of 20 percent or more.

- In the modern era since 1980, the average maximum peak-to-trough decline in the S&P 500 each year was 13.9 percent, as the chart below shows. In other words, corrections have been commonplace.

- During this modern era period, the S&P 500 declined by 15 percent or more peak to trough during 16 of the 45 years through 2024. In nine of those years it declined by 20 percent or more peak to trough.

- Nevertheless, since 1980, the S&P 500 traded higher for the year in 35 of the 45 years

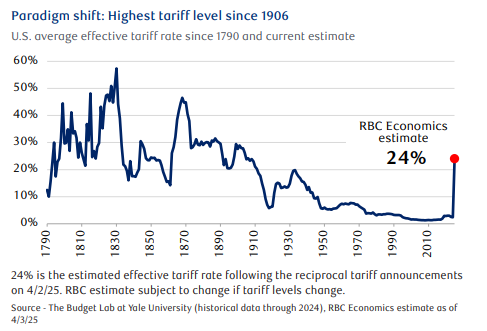

Is this a global paradigm shift?

Following the significant tariffs announced in the White House Rose Garden on April 2, RBC Economics estimates that the effective U.S. tariff rate surged from 2.4 percent in 2024 all the way up to 24 percent. If this elevated level stays in place, this would be the highest effective tariff rate since 1906, according to The Budget Lab at Yale University.

We believe the seeds of deglobalization and trade fragmentation along the shift toward a multipolar world were sown years ago. But Trump has stepped down hard on the gas pedal and has accelerated the process.

We think there is wiggle room for near-term U.S. tariff policy. Kevin Hassett, director of the White House National Economic Council, said that more than 50 countries have already reached out to negotiate tariff levels.

We’d be surprised if Trump didn’t adjust his tariff policies in the coming weeks or months, including by at least telegraphing some progress on tentative trade deals.

Clearly the profit outlook is murky. How should investors be thinking about this?

One of the biggest unknowns for equity markets is how tariffs will impact corporate profits in the near and medium term. This is important because profit growth is the mother’s milk of stock markets. What we have now is an abundance of uncertainty about profits.

RBC Capital Markets Head of U.S. Equity Strategy Lori Calvasina, estimates S&P 500 profit growth of about 4.5 percent from the 2024 level—below average although not bad given the circumstances. Calvasina has also lowered her 2025 year-end S&P 500 price target to 5,550 and noted that the situation had morphed from a “garden variety” correction to a “growth scare,” which is typically more forceful.

Growth scares occur when recession fears rise and begin to be priced into the market—but a recession doesn’t actually pan out when all is said and done. Thus far, RBC’s economists are not forecasting a recession, but they acknowledge the risks have risen.

Regarding this market shock, our advice to long-term investors is to take some deep breaths and count to 100, so to speak, before making big asset allocation and sector decisions. Stock market corrections—especially those tied to extreme circumstances—are admittedly difficult to endure. But we are investing in companies, not Washington policies, and historically companies have proven to be far more adaptable and resilient than is often given credit.

As always, please don’t hesitate to reach out to me should you have any questions or concerns.

All the best, Evan