Good news at last

The Pfizer/BioNTech COVID-19 vaccine announcement on November 9 was received by equity markets with enthusiasm, with the S&P 500 rallying 1.2 percent on the day, and the MSCI World Index reaching a new all-time high the day after. The results markedly surpassed general expectations, especially in terms of the vaccine’s efficacy in preventing symptoms, and some market participants seemed surprised by the timing of its availability. The vaccine is likely to be the first one to receive regulatory approval in the U.S. and Europe, which could happen within weeks.

The vaccine’s efficacy rate of more than 90 percent, far exceeding the U.S. Food and Drug Administration’s (FDA) 50 percent hurdle rate, is remarkably high for a first-generation vaccine. This could mean other vaccines using a similar technology are likely to be successful as well.

Some questions remain, including how safe the vaccine is, though this data should also be available within weeks. With time, we will find out how long the vaccine protection lasts and how efficient it is when used on the elderly, as cohorts are added to the trial.

Enthusiasm for the Pfizer/BioNTech vaccine is tempered by logistical challenges. It requires two doses to be administered three weeks apart. It also needs to be stored in dry ice to ensure a temperature of minus 70 degrees Celsius (-94 F) or below—a challenge for governments considering rolling it out, particularly for developing countries and those in temperate regions.

Once safety data is released, emergency use filing can be done in the U.S. and Europe. After receiving the full efficacy data in December, the FDA can approve the drug. Pfizer/BioNTech expects that 50 million doses can be available by year-end and 1.3 billion doses next year (i.e., 750 million vaccinated). For context, the EU has ordered 300 million doses, the U.S. 100 million, and the UK 30 million.

The possibility of vaccines taming the pandemic is becoming more tangible. Data for two other vaccines are due before the end of the year. The vaccine being developed by AstraZeneca and Oxford University is possibly the most eagerly anticipated. Based on a different technology, only one dose is required, and it wouldn’t need to be kept below freezing temperatures, suggesting it would be more scalable than Pfizer/BioNTech’s. Moreover, it is reportedly already known to be effective for the elderly. We should also know the results of the Moderna vaccine trial by year-end and the results of four others will likely come in sometime in the first half of next year. Should most of these be successful, the global vaccination rollout could make important inroads next year.

Good for the economy

To be sure, the manufacturing capacity and the distribution of the vaccine will not be in place to save the winter in the Northern Hemisphere. Social distancing and lockdown measures will likely stay in place for now, capping economic growth in the economically important Q4 2020 and possibly in Q1 2021. But the Pfizer/BioNTech data brings forward the possibility of a better outlook for economic growth in 2021 for several reasons, and as such, it is undeniably good news.

The availability of a vaccine and the success of its technology likely reduces the risk of a potential third wave in autumn 2021. Knowing there is an end to the crisis in sight, some governments could opt to give more generous fiscal relief than would have otherwise been the case. Our national research correspondent thinks a U.S. COVID-19 stimulus package of $1 trillion is more likely than one of $500 billion. A vaccine also helps investors to look through the COVID-19 valley and focus more confidently on the recovery and the post-pandemic world.

The vaccine announcement brought on abrupt risk-on moves in financial markets that day. The S&P 500 closed up 1.2 percent, a performance that came on top of post-election gains which had been the highest in history.

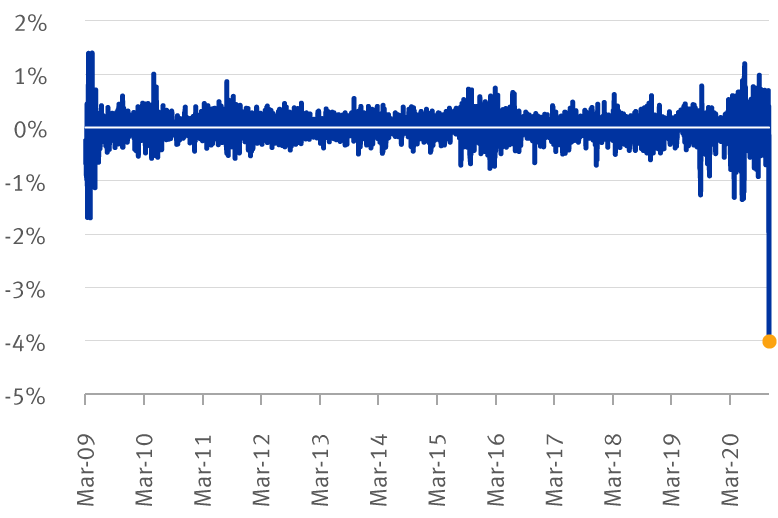

Sharpest market reversal since 2009

Daily price change in the Bloomberg US Pure Momentum Portfolio Total Return Index

ALT = Chart of daily price change (percentage) in the Bloomberg US Pure Momentum Portfolio Total Return Index from March 2009 through Nov. 10, 2020.

Source - Bloomberg; daily data through 11/10/20

The S&P 500’s move camouflages an aggressive rotation in equity markets. Momentum strategies, in which investors buy securities when their prices have been rising and sell those when they have been declining, had their worst performance since 2009. The FAANGs (Facebook, Amazon, Apple, Netflix, and Google parent Alphabet), which have led market gains since March, also retreated abruptly. These technology companies’ business models have thrived in the COVID-19 era, with their stocks being widely perceived by market participants as defensive investments in these difficult times. Globally, megacaps underperformed riskier small caps. Struggling Financials and Energy stocks roared upwards. Meanwhile, the oversold FTSE All-Share Index, a broad index of UK stocks, closed up approximately five percent, a rarely seen showing and its second-best performance since the 2016 Brexit referendum.

Other traditional growth indicators also pointed to an improvement in the economic outlook: the U.S. yield curve steepened, with the yield on the 10-year Treasury note increasing to 0.95 percent from 0.80 percent prior to the vaccine announcement. Profit-takers brought gold prices down to $1,855/oz, perhaps a sign of a safer environment.

A flash in the pan?

For investors, the question is whether these aggressive one-day moves herald a broader, more sustained rotation towards cyclical positions. To be fair, they were probably also a function of crowded positions, i.e., investors all chasing similar themes and being heavy in certain sectors (such as the FAANG group with their resilient business models for the current environment) while avoiding others (like the Energy sector due to the sharp fall in oil prices and banks due to ultralow interest rates). The aggressive market rotation also facilitated a record valuation differential between growth and value stocks.

A general and longer-lasting rotation towards reflationary positioning, or economically-sensitive stocks, would require inflation expectations to continue their ascent and Treasury yields to extend their moves upward.

For now, we believe it’s reasonable to expect a period of consolidation for equities following the sharp gains since the U.S. elections and vaccine news. Moreover, the global economy is not out of the woods yet, and investors may start to ponder the logistical challenges of rolling out vaccines globally.

Investors should use this time to consider their portfolios’ exposure to cyclicality, or economically-sensitive stocks. The possibility of viable vaccines should enable investors to look through the crisis and assess companies that were most affected by COVID-19 on the basis of normalised earnings. Many of these companies’ stocks will appear undervalued, in our view. We recommend adding some exposure to cyclicals and value stocks to take advantage of the likely improvement in economic conditions that COVID-19 vaccines could bring.

Non-U.S. Analyst Disclosure: Frédérique Carrier, an employee of RBC Wealth Management USA’s foreign affiliate RBC Europe Limited, contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since they are not associated persons of RBC Wealth Management, they may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.