...I’ll predict that the monthly balance is lower than usual, and not just by a modest amount. Assuming this prediction is correct, then as it turns out you are not alone:

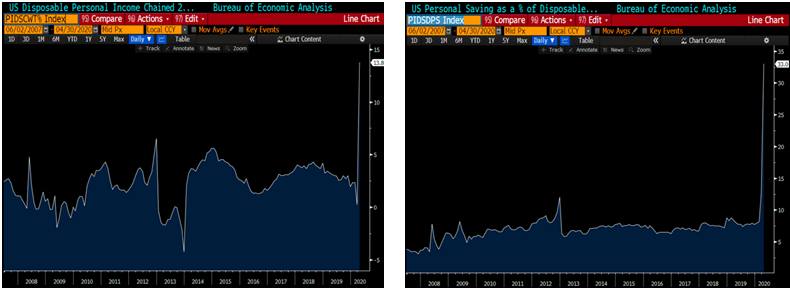

US Disposable Income (YoY%, left) and Personal Savings Rate (YoY%, right) – June 2007 to date

Source: BEA, Bloomberg

Not only is after-tax personal income meaningfully higher as a result of government benefits, but the percentage of it being saved is almost literally off the charts. Combined with the fact that US consumers reduced their borrowing as a percentage of income over the past the decade, on paper the US consumer has never been healthier. The Canadian consumer is not in quite the same position given that leverage was at an all-time high going into the pandemic; but of course for the path of a global economic recovery, it is the former that matters most.

As mentioned in previous updates, re-opening the economy is a process and at this point the process is still improving. High frequency data favourited by institutional investors like Apple’s Mobility Trends (an interesting too, link here) and credit card transaction data are showing positive momentum, even if off of a lower base. Very importantly, 7-day average infection rates continue to fall in North America despite the number of daily tests expanding significantly. Equity markets continue to drift higher in response.

Together with the consumer data above, the picture painted is one of government stimulus working exactly as intended at this point: cushioning consumers from the initial shock of the shutdown, positioning them to bounce back to normal quickly as the lockdowns end. But one has to wonder if we are just seeing the “easy gains” so far, and if so whether financial markets have overreacted to them. Given the large amount of new equity issuance that has been conducted over the past ten days, arguably corporate management teams seem to think so.

While policy makers have begun to ease the lockdown, consumers and business still appear very reluctant to resume to normal life without the perception of widely available testing, therapeutics and/or a vaccine. As just one example, on Friday the largest employers in Toronto together with the Mayor announced that employees won’t return to downtown offices until at least September, which will have a host of knock-on effects for smaller businesses and landlords. A more obvious and impactful example is the fact that global spending on business travel, tourism, major events and restaurant dining all remain at a small fraction of their pre-pandemic levels with no obvious timeline for anything but a very modest recovery. Said differently, the growth in Personal Savings is much high than the growth in Disposable Income, and those savings are obviously coming from somewhere.

What this suggest, then, is that we are advancing towards a couple of challenges as the “easy gain” period begins to fade over the coming weeks:

- A money velocity challenge, as the government stimulus to consumers mainly pools in savings accounts rather than being spent. This is similar to the challenge that Quantitative Easing faced last decade, where banks left huge excess reserves on deposit with the Fed rather than lending them out; and,

- A bridging period challenge, with the largest US consumer support programs scheduled in 8 weeks while businesses are not yet seeing enough revenue growth or enough direct aid to re-hire aggressively.

The second of these issues may get addressed by another(!) multi trillion-dollar stimulus package, but political jockeying ahead of that along with a short, 8-week fuse creates an environment for equity market volatility, especially given valuations. Meanwhile, the first issue above is going to remain a lingering problem until there is progress on a definitive medical solution. In the background, concerns over the coming US elections may re-emerge as the mid-August Democratic Convention and running-mate selection draws closer.

In the medium-term, a cashed-up US consumer that is temporarily reluctant to spend can be a fantastic asset for the US, Canadian and global economies. Over the same time horizon, it arguably also provides a strong tailwind for asset prices when compounded with near-zero interest rates. But in the short-term, with equity valuations having already risen in anticipation of a recovery, stock markets are vulnerable to the perception that the timing of the recovery is getting pushed out.

** Note: During the summer months, Street Savvy will move to a monthly frequency since news flow is typically light. If we see relevant and timely insights that we think you might value within a shorter time period, we will provide a mid-month update on an ad-hoc basis. The regular, twice-per-month cadence will resume in September.