Highlights:

- Ottawa pledges $71 billion to pay 75% of wages up to $847 per week for workers in hard-hit industries

- Government estimates amount to paying about a quarter of earnings in the economy for three months

- Support will be for firms with revenues down at least 30% year-over-year, with qualification on a monthly basis

- Small businesses that do not qualify can still claim previously announced 10% subsidy

- Deficit tracking at about $170 billion for 2020/2021 fiscal year

Last Friday, Prime Minister Justin Trudeau announced that the Government would increase a previously announced 10% wage subsidy for small business to cover 75% of pre-COVID wages at select businesses. Minister Morneau confirmed details of the proposed subsidy, pending new authorities to implement it this afternoon.

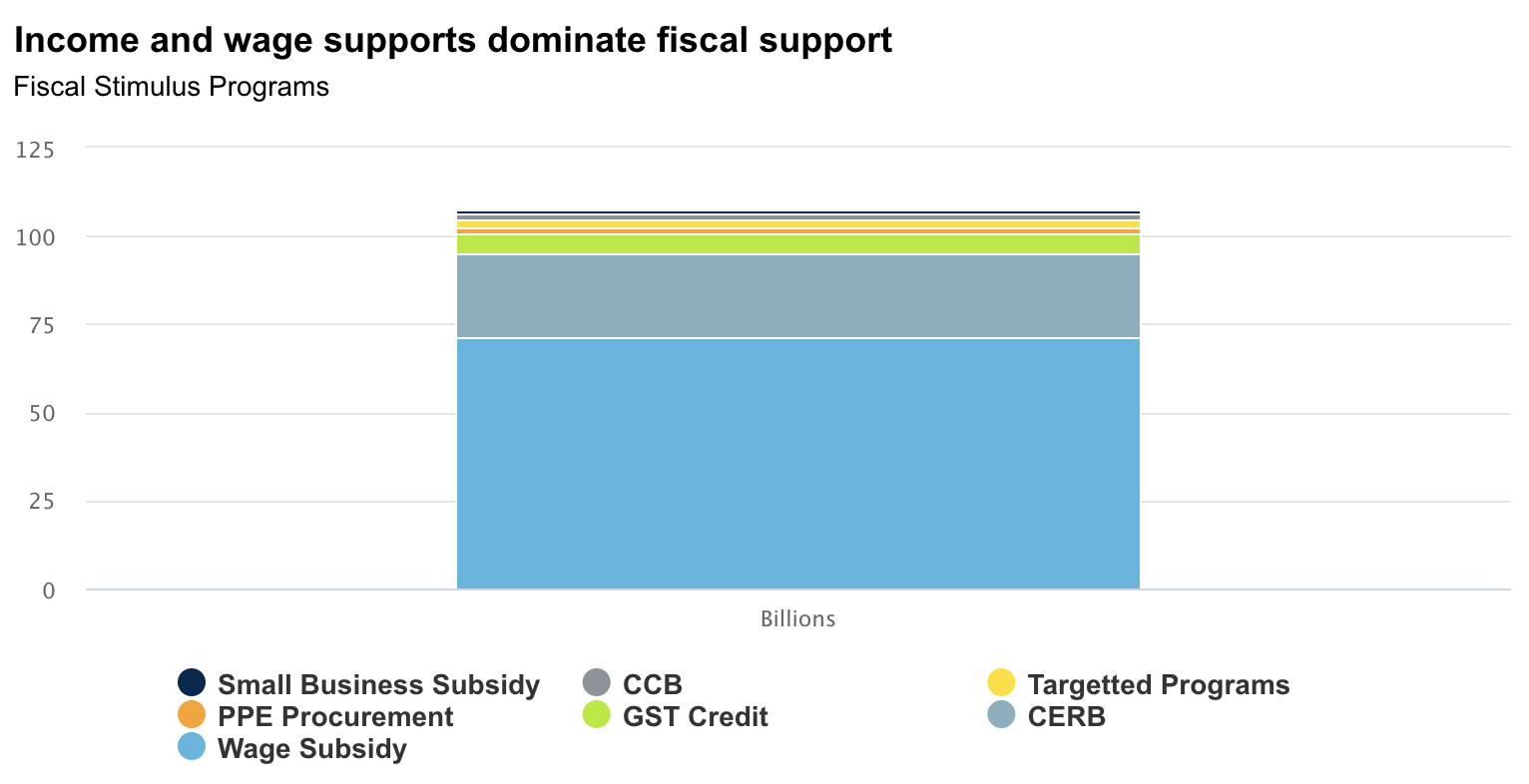

The Government pledged $71 billion (3.1% of GDP) to help businesses of all sizes who suffer revenue drops of 30% or more relative to this time last year. The subsidy will cover 75% of a worker’s pre-COVID earnings for up to 12 weeks, up to a maximum of about $10,000 per worker. For newly hired workers, employers would get 75% of their actual wages up to the same maximum. Firms must re-apply to the CRA every four weeks, and funds will start flowing in three to six weeks. While the Government signaled it expects firms to pay the remaining 25% of their workers’ wages, the program requires only their best efforts to do so.

As always, the devil will be in details: many of the firms most impacted by COVID-19 have little cash held in reserve and thin margins (retail trade, restaurants, etc.) For these firms, three to six weeks may be too long to wait for an infusion of cash. If the Government’s small business loan guarantees flow out quickly over the next few weeks, they could provide a good stop-gap measure for these firms. But even those with a relatively modest staff count would quickly see the $40,000 loan limit depleted by payroll obligations. Many of these firms are at risk of closing or at the very least laying off many of their staff if they cannot find other credit, even if they could qualify for subsidies in the future. More generous guarantees for more firms, clawed back when the subsidy flows out, could help address these risks.

While the measures will help mature firms retain their employees, those with lumpy revenues or short revenue histories may have difficulty accessing the program. Where firms cannot produce year-over-year revenue estimates (i.e., they did not have revenues in March 2019), senior Finance Department officials noted that alternative revenue measures will be available on a case-by-case basis. While promising, this provides little clarity for new firms suffering losses right now and could extend administrative delays in getting sorely needed money out the door.

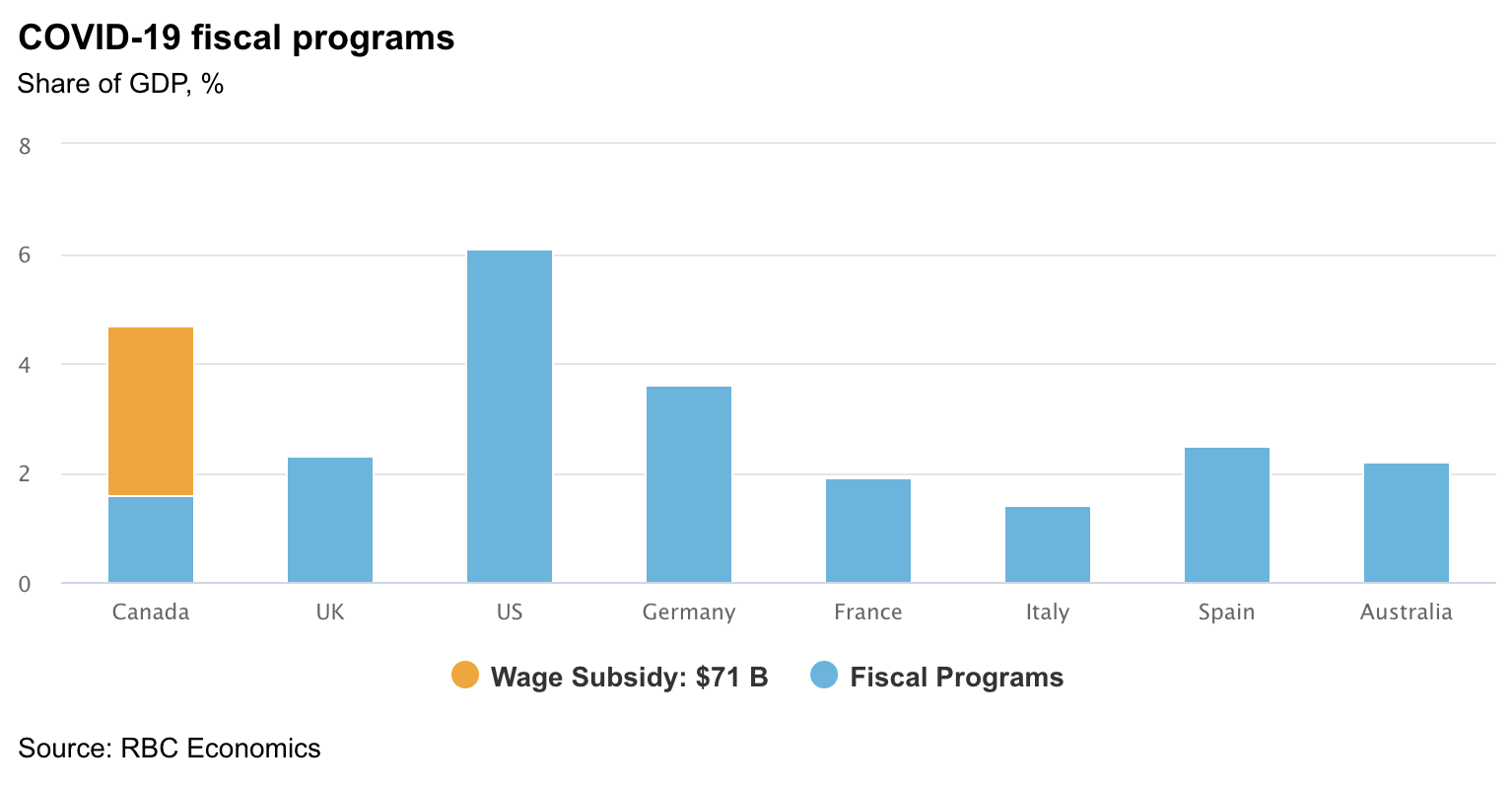

Taken together, these measures bring the federal government’s direct support for the economy to about $105 billion (4.6% of GDP), overwhelmingly focused on income support for workers (totaling $95 billion). Canada’s COVID-19 stimulus package is now among the largest relative to developed economy peers. Our overall view of the deficit for the 2020/2021 fiscal year now tracks at a whopping $170 billion (7.4% of GDP). Additional costs in the form of loan forgiveness under the small business lending program, about $6 billion by our count, and other EDC and BDC lending programs could now bring the deficit within striking distance of our $200 billion upper estimate.

Colin Guldimann is an economist at RBC. He works primarily on issues related to housing markets, energy, and climate change. Prior to joining RBC, Colin worked on housing policy and macroeconomic research at the Department of Finance in Ottawa.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.