Zero-tolerance COVID-19 response

Unlike most of the Western world that is trying to live with COVID-19 by imposing relatively light restrictions, and despite some 85 percent of its population being fully vaccinated, China is steadfast in pursuing its zero-tolerance policy of stopping community transmission through strict and swift containment measures. It recently locked down the city of Xi’an, home to 13 million people and a centre of semiconductor manufacturing. More cities, including Beijing, have also reported omicron cases in the past few days.

Many observers believe China’s zero-tolerance policy is destined to fail due to the emergence of the highly transmissible omicron variant, and eventually China will have no choice but to follow the path taken in the West. Our RBC Wealth Management analysts do not agree. They point out that due to China’s very large population, the unvaccinated 15 percent (totaling 210 million people) could easily overwhelm the health care system should a significant portion require emergency treatment. Moreover, research shows China’s vaccines are less effective against omicron than against previous variants.

Lockdown risks therefore continue to rise in China, even as they decline elsewhere. Increased pandemic restrictions could lead to additional supply chain disruptions, hold back the normalization of the global economy, and fuel global inflation, while capping Chinese economic growth.

Challenges in the property sector

While housing prices are up in most western countries, they are down in China. Recently, many property developers have defaulted on their foreign debt—including high-profile giant Evergrande, which owns more than 1,300 development projects in more than 280 cities. Evergrande is now negotiating with Chinese creditors to delay payments on its domestic debt.

Since the material deterioration of the real estate sector in October 2021, the government hasn’t intervened meaningfully to lessen the sector’s woes. Property developers seeking to raise funding through onshore/offshore credit financing, shareholder support, or asset sales are struggling, as investors’ and homebuyers’ confidence has been dented. The refinancing market remains mostly shut.

Given that the property sector represents a remarkably high 25 percent of China’s GDP, we think the authorities will make every effort to prevent a hard landing with additional incremental easing—though they are also likely to stick to their medium- and long-term deleveraging goals. As a result, the property market slowdown is likely to continue in the first half of the year and weigh on economic growth.

Will economic data stay positive?

Despite these issues, metrics of China’s manufacturing and services activity (PMIs) recently turned higher. This contrasts with the U.S. and the eurozone, where recent economic data are slightly weaker though still consistent with economic expansion. China’s Q4 2021 GDP growth was higher than consensus expected at 4.0 percent y/y, bringing full-year GDP growth to 8.1 percent y/y, much higher than the official target of six percent.

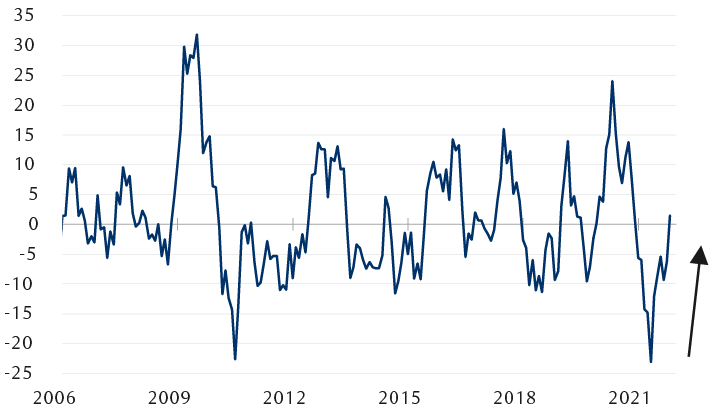

The government is now focused on economic stability and has introduced several measures aimed at supporting growth, including cutting banks’ required reserve ratio, loosening restrictions on mortgage loans, and encouraging banks to lend more to smaller private enterprises. In an encouraging development, RBC Global Asset Management Inc. Chief Economist Eric Lascelles points out that China’s credit impulse, or the monthly change in the flow of new credit as a share of GDP, has turned positive again after a long period in negative territory. This suggests Beijing is relaxing its efforts to curb lending at the moment.

Chinese credit impulse turns positive

Chinese credit impulse (percentage points)

Note: Measured as year-over-year change of 3-month rolling average of sum of total social financing, excluding equities and local government bond issuance, as a percentage of GDP.

Source - RBC Wealth Management, Haver Analytics, RBC Global Asset Management; data through November 2021

Nevertheless, we believe it’s likely that the zero-tolerance COVID-19 policy will eventually hinder Chinese manufacturing and exports, while the ongoing property market woes may hold back consumer spending and pose a threat to China’s macroeconomic and financial stability.

According to a consensus forecast of economists reported by Bloomberg, Chinese GDP is expected to grow at a rate of 5.2 percent in 2022, slightly below previous expectations. RBC Global Asset Management remains comfortable with its below-consensus forecast of GDP growth under five percent for 2022, but believes the government will succeed in stabilizing growth once the omicron wave has retreated.

Monetary policy: Exceptionally flexible

With the risks to the economy tilted to the downside for now, we expect the People’s Bank of China to remain flexible and accommodative. The central bank reduced interest rates for the first time since March 2020 on Jan. 17, lowering the seven-day reverse repo rate and the one-year medium-term lending facility (MLF) rate by 10 basis points (bps) each, to 2.10 percent and 2.85 percent, respectively. This follows other accommodative actions in late 2021, including cutting the required reserve ratio by 50 bps and the one-year loan prime rate by 5 bps, and launching re-lending facilities to support decarbonization and clean coal in November.

Though any further easing will likely be limited, in our view, China is a rare exception to the global trend of monetary tightening. Since at least last summer, Lascelles notes, most central banks have been tilting in an increasingly hawkish direction, either raising rates or signaling that such increases are on the way in 2022.

Despite concerns over downside growth risk and moderate easing, the renminbi has gone from strength to strength recently, thanks to a robust trade surplus and ample dollar liquidity onshore driven by attractive sovereign bond yields. On a six- to 12-month horizon, we believe the imminent inclusion of Chinese bonds in the FTSE World Government Bond Index should continue to attract foreign capital and underpin the currency. RBC Capital Markets expects the renminbi to appreciate slightly in 2022 and reach 6.35 USD at the end of the year.

Is it too early for China equities?

Amid the resurgence of COVID-19, an economic slowdown, and property market turmoil, the MSCI China Index has continued to underperform the MSCI World Index, which represents developed markets.

While valuations have become attractive, in our view, we would hold off adding to China equity positions at the moment given the aforementioned challenges. An opportunity to increase China exposure is likely to emerge after the first quarter, when investors see signs the present wave of COVID-19 infections has started to recede and more clearly understand the earnings impact of recent macro developments and policy changes. When the time comes, we would look at opportunities benefiting from secular growth trends, including electric vehicles, renewables, and advanced manufacturing processes such as robotics, as outlined in our 2022 Outlook article about China’s long-term prospects.