If you'd like to receive our email newsletter, you can subscribe here

Five Things That Caught My Attention This Month

Happy Family Day!

A few observations - from markets, behaviour and everyday life - that stood out this month.

This Month:

- Inflation, Brisket, and Why Infrastructure Keeps Showing Up in Institutional Portfolios

- Preferred Shares: Where’s the Yield?

- Real Estate Watch: Supply Is Starting to Matter

- Market Manipulation by AI Bots Is Coming (If It’s Not Already Here)

- When a Lift Ticket Starts Looking Like a Flight Ticket

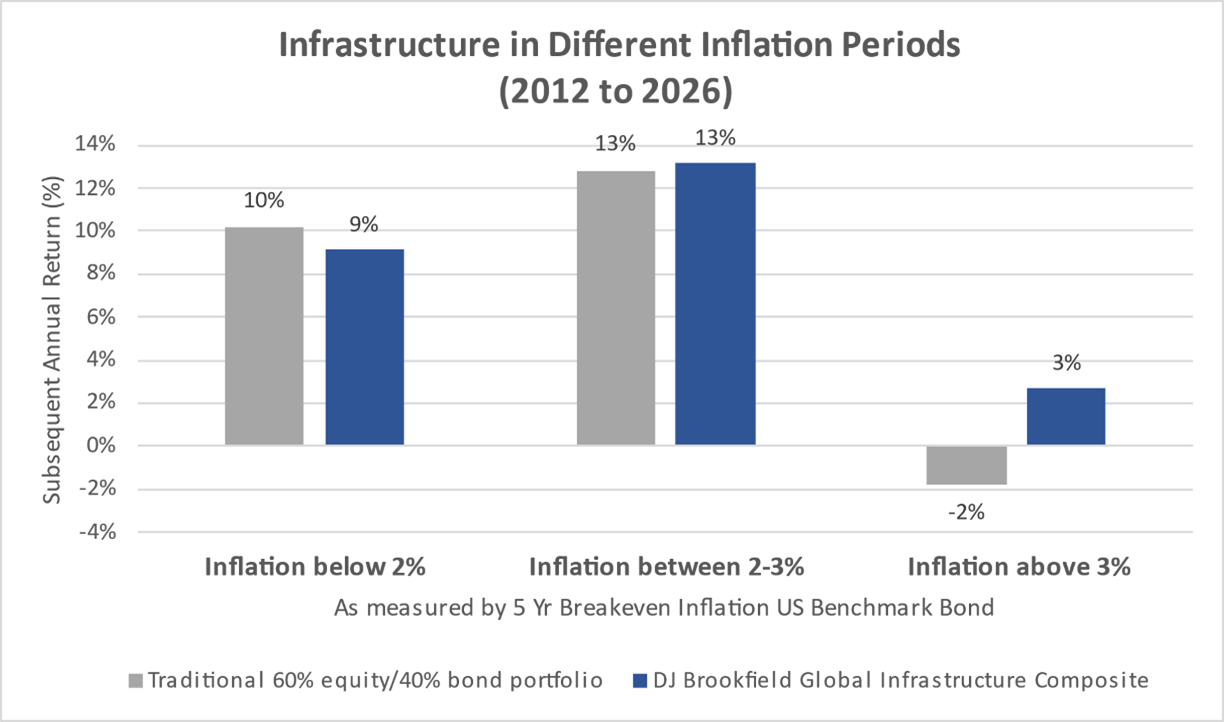

1. Inflation, Brisket, and Why Infrastructure Keeps Showing Up in Institutional Portfolios

I’ve written about inflation a lot over the past year - sometimes through policy and populism, sometimes through affordability, and sometimes through real-world signals like Jays ticket prices, brisket, and (how dare they) coffee. Which leads to the real question: how do we hedge rising costs so even the “necessities” stay within reach?

Gold has been incredible lately (no debate there), but its long-term record as an inflation hedge is mixed since the 1970s, and after such a strong run it’s hard for me to justify allocating incremental capital purely on the inflation narrative. Crypto? I understand the technological appeal, but I still struggle to view it as a reliable inflation hedge.

Instead, I keep coming back to one area institutions have leaned on for decades: infrastructure.

Why Infrastructure Has Become a Core Inflation Allocation

Infrastructure isn’t just an inflation trade, but periods of higher inflation often highlight the structural features that make it attractive. Many assets, such as toll roads, utilities, pipelines, and digital networks, perform well in these environments due to:

Contractual Pricing Power: Inflation-linked escalators and regulated rate bases help revenues move with rising costs. It’s not perfect protection, but the linkage is structural rather than narrative-driven.

Replacement Cost Advantage: Infrastructure is capital intensive. As labour, materials, and energy costs rise, existing assets often become more valuable because rebuilding them becomes more expensive.

Essential Demand & Diversification: Core infrastructure provides long-duration exposure to essential services - transportation, power, connectivity. Historically it has sat between equities and fixed income in risk profile, offering diversification while still participating in nominal growth.

As the chart shows, infrastructure has historically held up better than a traditional balanced portfolio when inflation moved above 3%.

Where the Risks Sit

Infrastructure isn’t immune to macro forces. Rising real rates can pressure valuations, and heavy capital inflows can compress future returns - especially when too much capital chases the same long-duration themes. At the same time, the structural need for new infrastructure remains enormous, particularly across electrification, transportation, and digital networks. That creates opportunity - but also introduces development risk, where timelines, costs, and regulatory approvals can materially impact outcomes.

From a portfolio perspective, implementation matters:

- Development vs. Core Assets: Higher return potential often comes with construction, execution, and permitting risk. Investors need to be honest about their tolerance for volatility and longer timelines.

- Active vs. Passive Exposure: Private infrastructure strategies can offer differentiated access and cash-flow profiles, but fees and manager selection become critical considerations.

- Liquidity: Many private offerings require long holding periods and may not behave like public markets during stress events.

- Regulatory and Political Risk: Infrastructure assets often operate under government oversight, which can introduce policy-driven uncertainty.

There are strong private infrastructure opportunities available - including through institutional platforms - but alignment between strategy, fees, and risk tolerance is key.

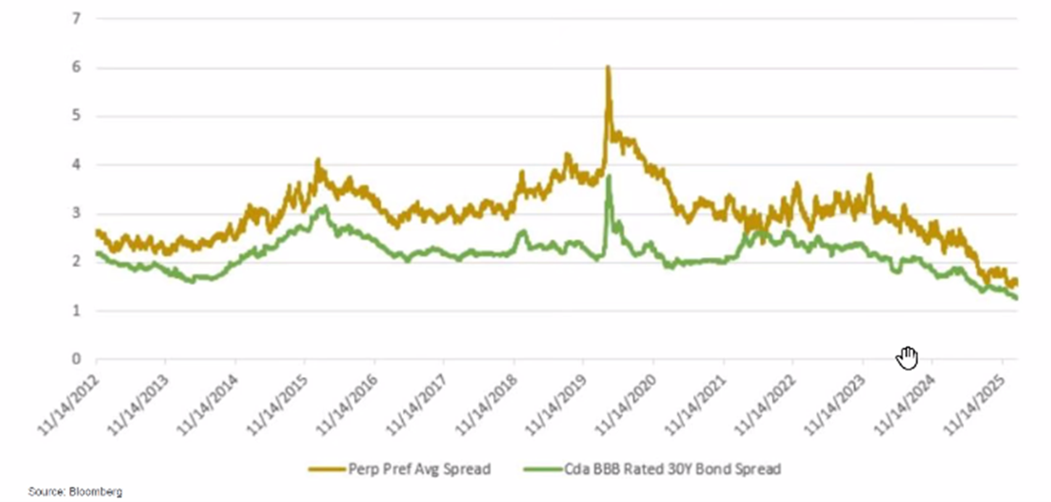

2. Preferred Shares: Where’s the Yield?

Preferred shares have always sat in an awkward place in portfolios. They often behave like long-duration fixed income but without a defined maturity, creating a structural trade-off: investors give up liquidity certainty in exchange for income and may get their capital back only when rates or credit conditions are unfavourable.

Historically, the appeal has been yield. Most Canadian preferred shares pay eligible dividends, which can make them more tax-efficient than bonds in non-registered accounts. But the core issue today is compensation. Yields have compressed to the point where investors may not be getting paid much extra relative to corporate bonds despite taking on call risk, perpetual structures, and greater credit sensitivity. Roughly 40% of perpetual preferreds are trading at or above their call price, limiting the potential benefit from falling rates, while even the remainder may lag traditional bonds as call features cap upside.

Rate-reset structures can help if yields move higher, but they do not eliminate duration or spread risk. Relative to equities, preferreds offer income without relying on growth. Relative to bonds, they offer potential tax efficiency but less structural protection. In practice, they sit somewhere in between, combining elements of both without fully inheriting the strengths of either.

Selective preferred exposure can still work, but as a broad allocation bonds look more compelling at current spreads.

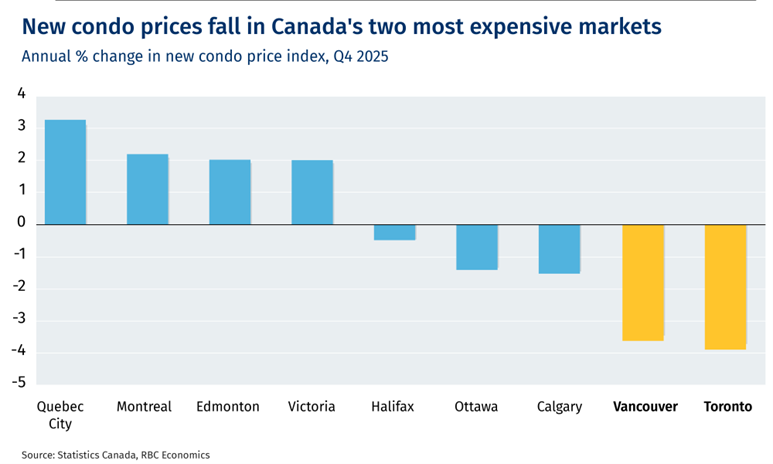

3. Real Estate Watch: Supply Is Starting to Matter

Despite ongoing talk of a near-term bottom, several indicators suggest the residential market, particularly condos in the GTA, may still be working through excess supply. Affordability remains stretched, listing-to-sales ratios are elevated, and new inventory continues to come to market. Anecdotally, I’m hearing that some lenders remain focused on reducing construction-related exposure, with certain mortgages still being referenced to original appraised values rather than recent re-sale levels: a reminder that price discovery in this cycle may take time. Recent analysis from RBC Economics highlights how a national surge in housing supply is contributing to softer pricing trends, with new condo values declining in Canada’s most expensive markets. This doesn’t imply a systemic housing downturn, but it does reinforce that markets may need patience as supply and demand rebalance.

4. Market Manipulation by AI Bots Is Coming (If It’s Not Already Here)

Market manipulation has been banned for decades because history shows how quickly coordinated narratives can pull investors away from fundamentals - from early pump-and-dump schemes to chat-room promotions and modern social-media squeezes. As I wrote in my recent LinkedIn post, the risk today isn’t just louder enthusiasm - it’s scale. Emerging AI-driven networks (like the “Moltbook” concept discussed by CNBC) could amplify sentiment and indirectly influence those who trade on technical analysis by shaping the very inputs charts rely on: price momentum, volume spikes, and breakout behaviour. The challenge going forward won’t simply be picking investments - it will be separating fundamentals from feedback loops and maintaining discipline in a market where both stories and price patterns can be amplified faster than ever.

5. When a Lift Ticket Starts Looking Like a Flight Ticket

I started running the numbers on ski trips back in December after a few too many conversations that began with, “Wait… that was just for one day?” When lift tickets for a family start pushing toward four figures, it stops feeling like a weekend activity and starts looking more like a spreadsheet decision. My takeaway was simple. Once day tickets creep into the $250 to $300 range, the math starts to shift, and the extra airfare to the Alps does not look nearly as outrageous.

Recently I came across an article that did a lot of the comparison work for me, and it reinforced just how quickly things tilt once prices get that high. European lift passes are often dramatically cheaper while unlocking huge interconnected terrain.

What I kept coming back to, whether I invented the term or just stumbled into it, is “value per vertical.” In my own numbers, the best value per vertical came from the big Alpine domains, particularly the Dolomites. And that comparison still does not fully capture the terrain or the ability to move between multiple towns in a single day.

Closing Thoughts

Markets right now continue to reward quality, liquidity, disciplined duration, and thoughtful tax planning. They are far less forgiving of stretched yield, illiquidity, or narratives that rely more on optimism than fundamentals.

Ari Black, CFA, HBA | Investment Advisor

RBC Dominion Securities Inc.