Another runaway U.S. inflation report put markets back on edge this week as the Consumer Price Index showed headline inflation running at an annual pace of 7.5 percent, once again outpacing consensus expectations, suggesting that economists are still struggling to get a grip on underlying inflationary pressures.

And that inflation uncertainty, and associated uncertainty around the Fed’s policy response to it, is now reverberating through global fixed income markets as traders have sharply repriced the Fed’s expected policy response.

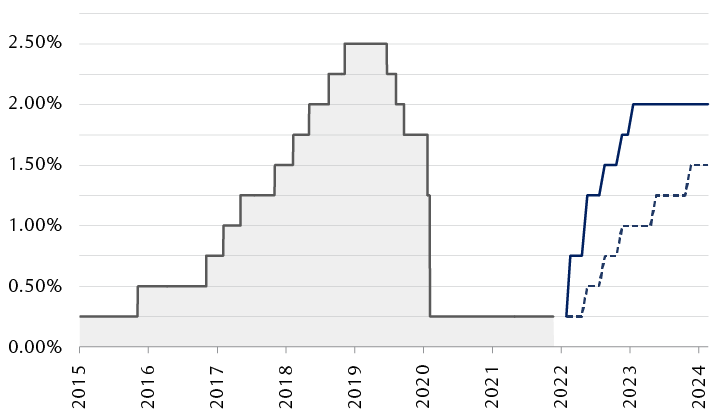

The chart below shows how much things have changed in just a few months since the Fed last met in December. Markets are now looking for a total of six to seven rate hikes this year, which could bring the upper bound of the Fed’s overnight fed funds rate to as high as 2.0 percent. On top of that, markets see a significant chance that the Fed could deliver a 50 basis point (bps) rate hike in March, something it hasn’t done since May 2001, having preferred to move in more customary 25 bps increments. Thus far in 2022, rate hike expectations also have become more aggressive in Canada, Europe, and the UK.

The market now expects an accelerated Fed tightening timeline, but will policymakers follow it?

Source - RBC Wealth Management, Bloomberg; shows upper bound of Fed’s target federal funds rate range

As a result, fixed income markets faced significant selling pressure this week both inside the U.S. and outside. The yield on the benchmark 10-year Treasury jumped above the two percent level for the first time since the summer of 2019. Yields at the front end of the Treasury yield curve—which are more sensitive to expected Fed rate hike plans—have risen by an even greater degree where the two-year yield now stands at nearly 1.60 percent, up from just 0.20 percent as of last fall.

With bond prices falling as yields rise across markets, performance numbers show that many U.S. fixed income sectors are off to their worst start to a calendar year in decades: Treasuries are down 2.9 percent, investment-grade corporate bonds have dipped by 4.4 percent, municipals have lost 2.7 percent, and preferred shares—which are sensitive to both interest rates and stock market volatility—have posted losses of 7.2 percent (all based on Bloomberg bond indexes).

Inflation will ease. Seriously this time.

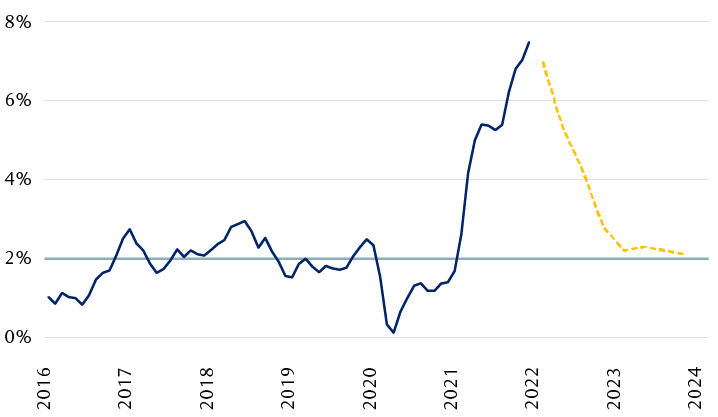

While inflation has clearly proved more persistent than anyone has expected, there are reasons to believe that developed economies are nearing the end of the worst of it. As RBC Capital Markets, LLC’s Chief U.S. Economist Tom Porcelli has highlighted in recent notes, the inflation story remains largely one of too much demand chasing too few goods, which should fade as consumers gradually revert to pre-pandemic spending patterns, and to spending on services and away from goods. Additionally, high inventories raise the possibility that goods prices could decline more than expected. RBC Capital Markets projects the year-over-year U.S. consumer inflation rate to fall back below three percent by the end of the year.

Through it all, economists continue to see inflationary pressures fading toward the Fed’s 2% target

Source - RBC Wealth Management, Bloomberg, RBC Economics forecasts for February 2022

What’s priced in?

So after a volatile start to the year, there are plenty of reasons to believe that things should begin to stabilize from here. As the chart below shows, the dramatic shift higher in the Treasury yield curve from last year’s levels has yields now nearing RBC Capital Markets’ recently updated yield forecasts for the end of 2022. With the market expecting that the Fed’s policy rate will peak around 2.00 percent to 2.25 percent this cycle, we believe the benchmark 10-year Treasury yield will settle into a trading range within that same window, as markets have fully priced the Fed’s rate hike expectations, and perhaps even overly so.

The bulk of the Treasury market’s repricing of Fed rate hike expectations now looks to have occurred

Source - RBC Wealth Management, RBC Capital Markets forecasts, Bloomberg

Should yields stabilize, then we believe coupons earned from fixed income securities will help to gradually claw back some of the underperformance that we have seen through the first six weeks of the year. For investors with cash on the sidelines, the recent backup in yields could soon offer attractive entry points, in our view.

Everything in moderation

Indeed, the Fed has been late to respond to inflation over the past six months, but overreacting to yesterday’s inflation at the moment that tomorrow’s inflation may fade not only risks making a policy error but also puts a sustained economic expansion in jeopardy—which would run counter to the Fed’s ultimate goal.

Our base case remains that the Fed will deliver four rate hikes this year, with balance sheet reduction serving as a de facto fifth hike. We think a reasonable scenario is that the Fed right-sizes its policy rate this year to better align with the current economic backdrop before pausing the rate hike cycle to assess the future economic backdrop. The Fed’s March policy meeting will likely come with a 25 bps rate hike, but it will also come with more clarity, which should ultimately ease the market’s fears.

So while fears around Fed policy have sparked recent volatility, the historically strong and quick economic and labor market recovery has been one of the great policy success stories of recent decades. Recent market volatility around the Fed’s need to counteract some of that strength—and associated inflation—is perhaps just the price of that success.