The Weekly Insight

The Insights

- Canadian households accumulated a record amount of savings during the pandemic, but the gains have not been evenly distributed.

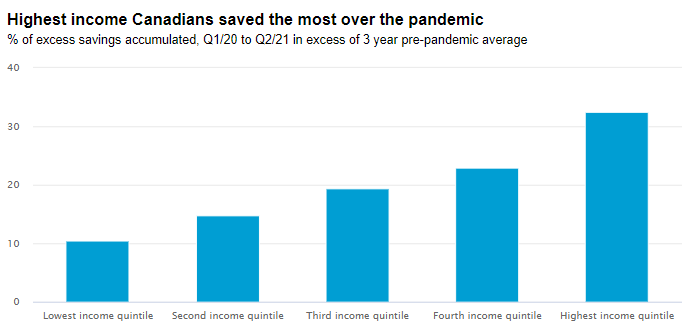

- Higher-income households built the biggest savings stockpile, and now hold more than 30% of overall pandemic savings compared to just 10% held by the lowest income households.

- Though lower-earning households saw the fastest rise in disposable income, much of that was likely spent or used to pay down debt.

- The sizeable cache of overall savings will add substantial upside to growth and inflation risks if spending increases come faster than expected.

The Stakes

Canadian households accumulated the highest amount of excess savings among G7 countries during the pandemic, as estimated by the IMF in October. By our count, household put away about $280 billion in extra savings compared to pre-pandemic trends. Some of those savings were used to pay down non-mortgage debt, some has flowed into financial and housing market investments (which also count as a form of ‘savings’) and a large chunk of the rest sits in cash deposits, which have also surged above from pre-pandemic levels. That savings trove represents over 10% of annual Canadian GDP, enough to support around 3.5 years of pre-pandemic restaurant sales. How and when those savings are spent will have significant implications for GDP, inflation, and ultimately monetary policy going forward.

Source: Bank of Canada, Statistics Canada, RBC Economics

The Context

Government supports shielded incomes during the COVID-19 pandemic, even as opportunities to spend, particularly on services, were sharply curtailed. The result was a massive buildup of household savings, both in Canada and abroad. The recovery in spending to-date has already had a dramatic impact on the global economy, with strong demand for goods swamping global supply chains still grappling with pandemic disruptions. As economies reopen, spending on high-contact travel and hospitality services has also started to normalize. Producers across sectors have warned that input and labour shortages could lead to higher prices for consumers. A surge in spending, driven by record savings, risks exacerbating that imbalance and adding to more persistent inflation pressures.

Source: Statistics Canada, RBC Economics

Our Analysis

The increase in household savings during the pandemic has been disproportionately concentrated in higher-income households that tend to spend less of each additional dollar of income. By our estimation, households in the highest income quintile held a little over 30% of overall excess savings, compared to just 10% held by households from the lowest income quintile. That matters when thinking about the amount of the excess savings that will be spent in the near-term.

Lower income households saw disposable incomes rise the most in percentage terms during the pandemic. But these households are also likely to have already spent much of that income, with many dis-saving (spending more than brought in) for years before the pandemic. By contrast, the highest income households spent 80% of their incomes prior to last year.

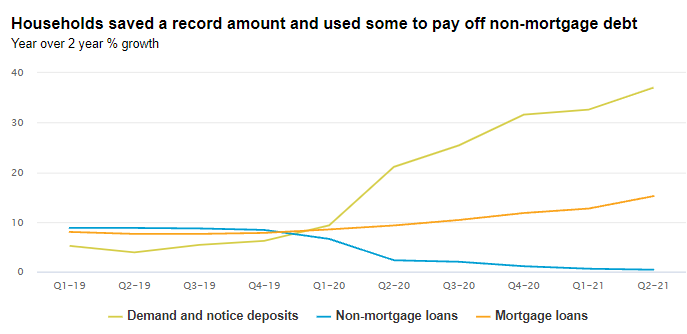

This pattern didn’t change in 2020. Higher-income households that were already saving substantially more merely added to their stockpile. And for the most part, lower income households simply borrowed less for day-to-day use—carrying smaller balances on credit cards. Government income transfers that targeted lower wage workers who lost income have in many cases likely been spent too.

The high rate of saving among higher-income households doesn’t mean the remaining stockpiles won’t be spent—they will. Just not necessarily right away, and not necessarily on goods and services. A large chunk will be directed to purchases of assets (financial markets, housing, etc.) and potentially even bequeathed to future generations.

Source: Statistics Canada, RBC Economics

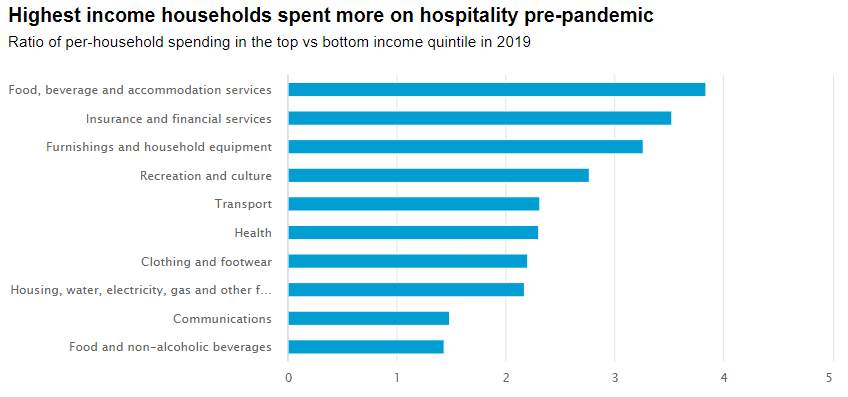

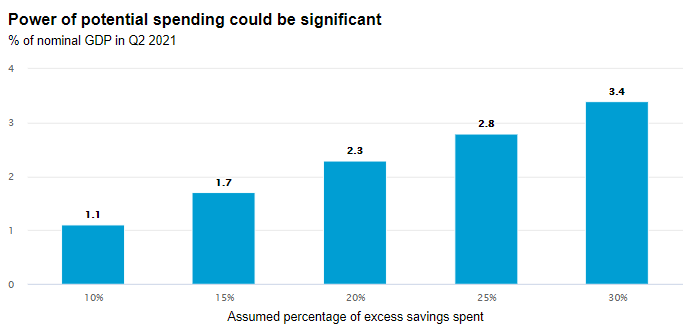

Spending on higher-contact services (restaurants, hotels, etc)—severely limited during the past year and a half—is expected to rebound further. That’s particularly true for higher-income households that tend to spend more on services. For instance, households in the highest-income earning quintile spent almost four times as much on restaurant and accommodation services prior to the pandemic than the lowest-income quintile. The Bank of Canada in October estimated that 20% of accumulated pandemic savings will be spent over the coming years. That adds up to potentially $60 billion of spending above-and-beyond normal levels—the equivalent of over 2% of annual Canadian GDP.

Source: Statistics Canada, RBC Economics Projection

Unleashed, that amount of spending could push demand growth substantially higher in the coming years. But it would also add to inflation pressures at the same time it adds to the volume of goods and services produced (i.e. GDP.) Businesses across sectors face a very difficult challenge to increase their production fast enough to keep up with that level of spending. Labour shortages—which are also becoming more acute in high-contact service industries—will continue to limit their ability to ramp up production and sales. Indeed, many workers that used to be employed in these sectors have switched to other industries and re-hiring may not be possible—at least not at pre-pandemic wage rates. By our calculation, high-contact services industries were still 287,000 workers short of pre-pandemic employment levels in September. That compares to just around 200,000 workers still needed in the overall job market to bring the unemployment rate nearer to a long run trend of 6%. At some point, adding more demand is akin to pushing on a string, at least in the near-term.

The Road Ahead

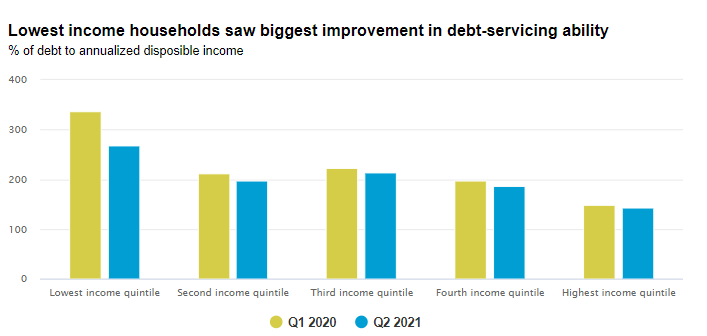

The reality is that the recovery in the labour markets has been strong enough that significant spending isn’t required to support a ‘full’ economic recovery in Canada. Even spending a ‘normal’ share of earned household wage income would be enough. The excess savings and cash holdings may quicken and extend the economic recovery while acting as a substantial buffer to help absorb any unexpected shocks or increases in borrowing costs. With inflation already firming, job markets improving, and vaccinations so far preventing another round of broad economic lockdowns, the Bank of Canada will soon run out of reasons to keep interest rates at rock-bottom levels. The lowest income households saw the biggest improvement in their debt-servicing abilities over the pandemic, as income gains outpaced the rate of debt accumulation. Regardless, these households continue to hold a higher level of indebtedness, leaving them the most vulnerable to interest rate hikes.

Source: Statistics Canada, RBC Economics