The massive retrenchment in activity a year ago heavily distorted the housing market picture in April. On the face of it, home resales and new listings skyrocketed 140 percent to 462 percent among Canada’s largest markets. But base effects vastly exaggerated these numbers. A focus on monthly (seasonally-adjusted) movements reveals signs of moderation across several housing markets in April. After soaring to outer space in prior months, home resales came down to a lower orbit—still generally strong but less excessively so—in Vancouver, Toronto and Ottawa. Montreal lost some altitude a couple of months earlier and has since remained largely in a holding pattern. Activity in Calgary and Edmonton, on the other hand, has yet to change trajectory. Both still trended higher last month despite the third wave of the pandemic reaching worrisome levels in Alberta.

Whether or not moderating in April, all major markets continued to heavily favour sellers. Inventories generally remain low (despite rising somewhat), leaving few options for buyers to fight over and fueling widespread bidding wars. So it isn’t a surprise that home prices showed no signs of moderating. Quite the contrary, they escalated at a faster rate in April in all major markets, reaching new record highs in most markets (except in Alberta). Single-family homes are the undisputed hotter category everywhere but condo prices have gathered steam in recent months. We expect this trend to continue with a sharp deterioration in single-family home affordability (in both large and smaller markets) driving more buyers toward condos. Here are the major market highlights for April:

Toronto area—Some market fatigue sets in?

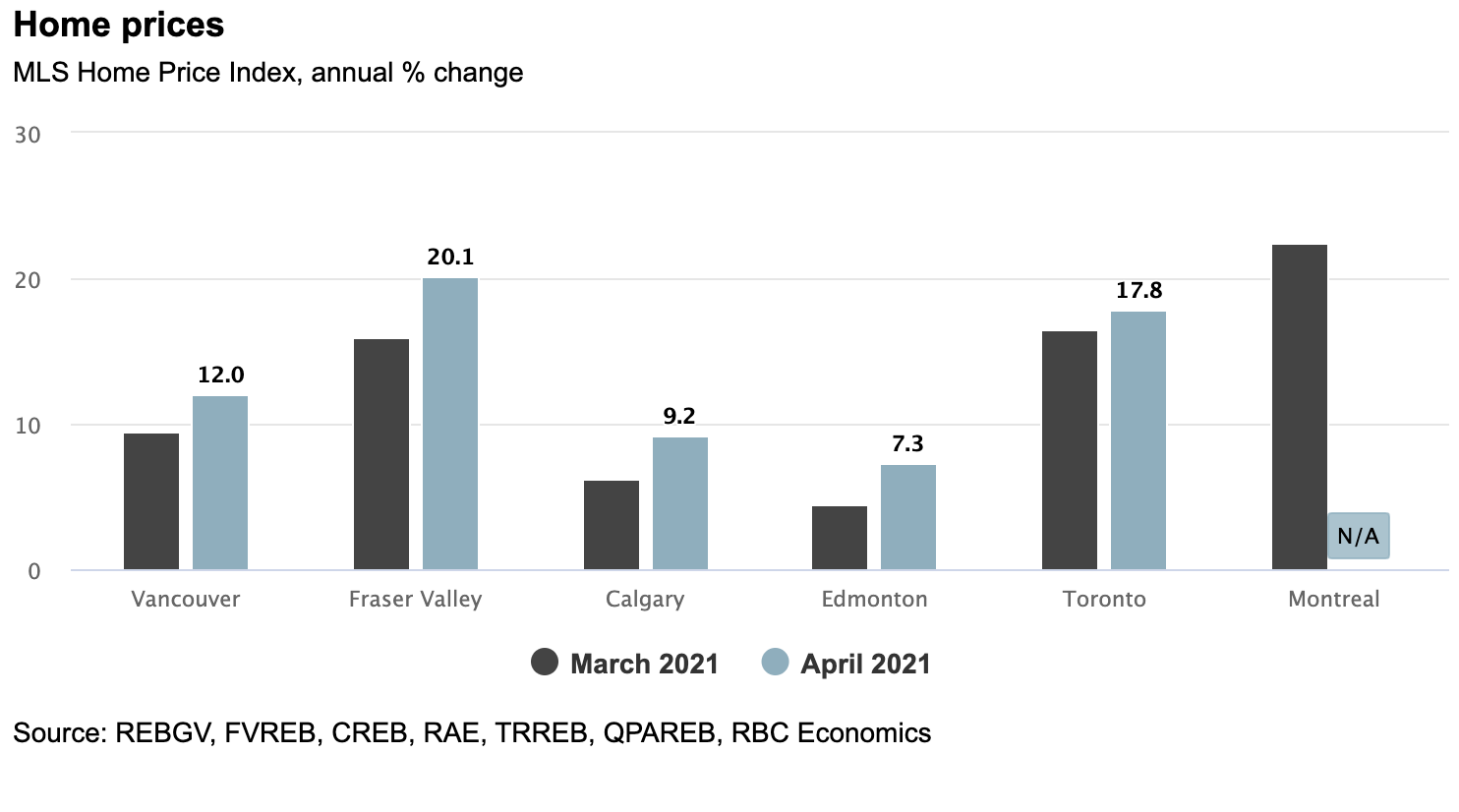

The Toronto Regional Real Estate board estimated home resales fell 20 percent between March and April on a seasonally-adjusted basis, providing the first sign that the furious pace of the last four months is finally slowing down. No doubt the spike in prices—the Toronto area’s composite benchmark is up more than $120,000, or nearly 14 percent, since November—has taken many potential buyers out of contention. Yet, higher prices haven’t opened the floodgates for sellers. Despite rising for three straight months, for-sale inventories are still historically low. So tight demand-supply conditions continue to apply intense upward price pressure. The rate of increase in the area’s MLS Home Price Index climbed to a four-year high of 17.8 percent y/y last month. Single-family homes (up 24.5 percent) accounted for most of the increase though we got further evidence the condo segment is on the mend with prices accelerating for the second-consecutive month (up 4.3 percent). Suburban neighbourhoods have been the hottest spots in the region through the current boom. This continued to be the case in April. The MLS HPI was up 33.5 percent y/y in Durham Region and 24.5 percent in Halton Region, far stronger than the 9.1 percent rise recorded in the City of Toronto (held back by the earlier softness in the downtown condo segment).

Montreal area—In a holding pattern

The market stayed in a holding pattern in April. We estimate home resales rose 2.1 percent m/m (seasonally adjusted)—following a modest 2.9 percent m/m decline in March. Demand-supply conditions and inventories were little changed. They still put sellers squarely in the driver’s seat. Strong competition between buyers kept home prices spiralling further upwards. The area’s median prices surged 39 percent y/y for single-family homes and 23 percent for condos—the fastest rates of increase on record. Single-family homes continued to draw the most bids from buyers, extending a trend throughout the pandemic. Yet it’s condo apartments that registered the stronger resales growth over the past few months. This partly reflects better affordability relative to other housing categories and more plentiful inventories (especially on the Island of Montreal). That said, those inventories have shrunk materially, setting the stage for firmer condo price gains.

Vancouver area—Market still strong despite activity moderating

By our own estimation, home resales dropped more than 20 percent in April from an all-time high in March (seasonally adjusted). This still left activity 56 percent above the 10-year average for the month. In other words: the market continued to be exceptionally strong. For now, sellers remain in command, keeping prices on an accelerating path. Vancouver’s composite MLS HPI increased 12.0 percent y/y in April, up from 9.4 percent in March. Gains are strongest for single-family homes (20.9 percent y/y) thanks to pandemic-induced demand for larger indoor space. Condo prices (up 5.9 percent y/y) are heating up, however, as this category’s relative affordability advantage is now attracting more buyers. The moderation in overall resale activity last month alongside a welcome rise in for-sale inventories—largely seasonal in nature—helped reduce the imbalance between demand and supply. A further cooling of demand and even more listings will be necessary to move the market back to balance and temper price increases. It’s unclear whether this will take place in the coming months.

Calgary—Full steam ahead

Calgary’s market got hotter last month. We estimate home resales shot up more than 10 percent from March on a seasonally adjusted basis, setting a new all-time record. The firmer tone in the market over the past several months attracted more sellers, though not nearly enough to meet supercharged demand. This further intensified competition between buyers and raised price pressure. Calgary’s composite MLS HPI rose 9.2 percent y/y, the fastest rate in seven years. Given the substantial degree of tightness in the market presently, double-digit price gains are likely just around the corner. In fact, single-family homes crossed that threshold last month (appreciated by 11.0 percent y/y). Condo prices are far behind but have been rising for two consecutive months.

Edmonton—Lack of supply

Buyers took a breather in April. Resales slipped approximately two percent from March (seasonally adjusted) based on our own calculation. The pause in activity likely had more to do with a lack of supply—inventories remained historically low—than a waning of demand as activity stayed elevated. Property values appreciated at a faster rate. The composite MLS HPI was up 7.3 percent y/y, the strongest rate in more than a decade.

This report was originally published by RBC Thought Leadership.

Robert Hogue is a member of the Macroeconomic and Regional Analysis Group, with RBC Economics. He is responsible for providing analysis and forecasts for the Canadian housing market and for the provincial economies. His publications include Housing Trends and Affordability, Provincial Outlook and provincial budget commentaries.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.