April 22 marked the 50th anniversary of Earth Day, a day dedicated to the protection of the planet. This year’s theme was climate action—i.e., taking steps towards restoring the planet. In honor of Earth Day, we highlight a number of environmentally friendly investment themes, including clean energy, low carbon, and fossil fuel free.

All values in Canadian dollars and priced as of April 21, 2020 market close, unless otherwise noted. Produced: Apr 27, 2020 12:05ET; Disseminated: Apr 27, 2020 12:30ET. For distribution in Canada only; for important disclosures and author’s contact information see page 3. By the end of 2019, climate change emerged as a megatrend in investments, as major weather-related events increased in frequency and severity causing US$630 billion in economic damages worldwide. According to a Morgan Stanley survey, 78% of U.S. individual investors have taken notice and are interested in addressing climate change through their investments.

Clean energy

One way to invest in environmentally friendly securities is through the clean energy lens. Clean Energy Canada defines clean energy as ‘the technologies and services that increase renewable energy supply, enhance energy efficiency, improve the infrastructure and systems that transmit, store, and use energy, and deliver key energy services while reducing carbon emissions’. This includes companies that produce energy from renewable resources such as solar and wind. By nature, the clean energy sector tends to be heavily skewed towards Utilities and Industrials companies. Clean energy is synonymous with alternative energy, renewable energy, and green technology.

Low carbon

As per the U.S. Environmental Protection Agency, greenhouse gases trap heat in the atmosphere. This primarily refers to carbon dioxide, but also includes methane, nitrous oxide, and fluorinated gases. Given the extent of carbon dioxide in the greenhouse gas pool, many investments in this category monitor carbon emissions. These strategies will either invest in companies that are the most carbon efficient, or will target a certain carbon efficiency relative to the benchmark. Often these investment solutions also pair the low-carbon mandate with a negative screen (i.e., excluding companies with business involvement in tobacco, weapons, or nuclear, etc.).

One method companies are embracing in an effort to keep their footprint low is carbon offsetting, a practice that gives businesses, individuals, and governments the opportunity to neutralize emissions they put into the environment. In its Climate Blueprint, Royal Bank of Canada outlined the goal of achieving net-zero carbon emissions in global operations annually, by committing to reducing greenhouse gas emissions by 2.5% each year, with a target of 15% by 2023, and increasing its sourcing of electricity from renewable and non-carbon emitting sources to 90% by 2023. This practice may result in some surprising companies (that could include Microsoft, Apple, and Johnson & Johnson) being large holdings in low-carbon investment strategies.

Fossil fuel free

In the context of investing, fossil fuel free generally refers to companies that do not own fossil fuel reserves or those without high fossil fuel usage. Fossil fuel reserves in many cases refer to economically and technically recoverable sources of crude oil, natural gas, and coal. Note that some mandates do not consider metallurgical or coking coal (used in connection with steel production) to be fossil fuel reserves. Solutions that use a fossil fuel free strategy employ negative screening, where they exclude companies that fall under this umbrella.

Climate change implementation

There are a few options investors should consider when trying to make their portfolios more climate-friendly. Mutual funds and/or exchange-traded funds offer a way to get pooled exposure to one of the above themes.

Many of these solutions use different approaches: some are managed actively, while others use a rules-based strategy; and some aim to maintain a target tracking error compared to their parent index while others are benchmark agnostic. As such, it is important to take a look under the hood and understand each product’s methodology. Alternatively, when considering the addition of individual stocks or bonds to a portfolio, investors can weigh the company’s commitment to one of the above themes as an additional evaluation criteria. On the fixed income side, investors can also take a look at green and transition bonds.

Green bonds

A green bond can be issued by governments and businesses, is differentiated from a conventional bond based on the use of proceeds, and accounts for 77% of all sustainable debt issued. Issuers are mandated to disclose how they plan to use the proceeds, which gives investors the opportunity to decipher if the project is in line with their socially responsible investing goals. Issuers can use tools and frameworks developed by the Climate Bond Initiative (CBI) to determine appropriate uses of funds. Common and acceptable green bondfunded projects, according to the CBI taxonomy, would be ones that use renewable energy, reduce water usage, and create “green buildings”.

Transition bonds

A transition bond aims to turn “brown” into “green”, as the bonds are tied to decarbonizing goals, and present a way for industries that are not traditionally “green” to reduce their carbon footprint. The proceeds are mandated to be put towards activities related to climate transition. These bonds are different from green bonds, as the focus is on the issuer’s commitment to becoming greener, whereas proceeds from green bonds are directed towards an environmentally-friendly project. For an economy that is heavily supported by natural resources, such as Canada’s, these bonds provide funding for companies to operate, while reducing greenhouse gas emissions.

Open the toolbox

Given the variety of investment solutions available within clean energy, low carbon, and fossil fuel free themes, we believe investors have access to the tools necessary to position their portfolio to celebrate Earth Day all year round.

Disclosures and disclaimers

Analyst Certification

All of the views expressed in this report accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securities or issuers. No part of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the responsible analyst(s) in this report.

This report is issued by the Portfolio Advisory Group (“PAG”) which is part of the retail division of RBC Dominion Securities Inc. (“RBC DS”). The PAG provides portfolio advisory services to RBC DS Investment Advisors. Reports published by the PAG may be made available to clients of RBC DS through its Investment Advisors. The PAG relies on a number of different sources when preparing its reports including, without limitation, research reports published by RBC Capital Markets (“RBC CM”). RBC CM is not independent of RBC DS or the PAG. RBC CM is a business name used by Royal Bank of Canada and certain of its affiliates, including RBC DS, in connection with its corporate and investment banking activities. As a result of the relationship between RBC DS, the PAG and RBC CM, there may be conflicts of interest relating to the RBC CM analyst that is responsible for publishing research on a company referred to in a report issued by the PAG.

Required Disclosures

With respect to the companies that are the subject of this publication, clients may access current disclosures of RBC Wealth Management and its affiliates by accessing our web site at https://www.rbccm.com/GLDisclosure/PublicWeb/DisclosureLookup.aspx?EntityID=2 or by mailing a request for such information to RBC Wealth Management Research Publishing, 60 South Sixth Street, Minneapolis, MN 55402.

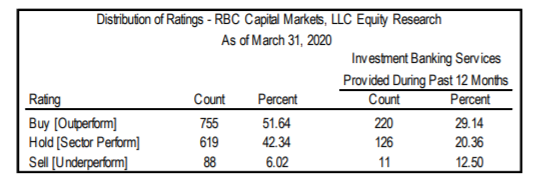

RBC Capital Markets’ Distribution of Ratings

For purposes of ratings distributions, regulatory rules require member firms to assign ratings to one of three rating categories − Buy, Hold/Neutral, or Sell − regardless of a firm’s own rating categories. Although RBC Capital Markets’ ratings of Outperform (O), Sector Perform (SP), and Underperform (U) most closely correspond to Buy, Hold/Neutral and Sell, respectively, the meanings are not the same because our ratings are determined on a relative basis.

Explanation of RBC Capital Markets’ Equity Rating System

An analyst’s “sector” is the universe of companies for which the analyst provides research coverage. Accordingly, the rating assigned to a particular stock represents solely the analyst’s view of how that stock will perform over the next 12 months relative to the analyst’s sector average.

Ratings:

Ratings: Outperform (O): Expected to materially outperform sector average over 12 months. Sector Perform (SP): Returns expected to be in line with sector average over 12 months. Underperform (U): Returns expected to be materially below sector average over 12 months. Restricted (R): RBC policy precludes certain types of communications, including an investment recommendation, when RBC is acting as an advisor in certain merger or other strategic transactions and in certain other circumstances. Not Rated (NR): The rating, price targets and estimates have been removed due to applicable legal, regulatory or policy constraints which may include when RBC Capital Markets is acting in an advisory capacity involving the company.

As of March 31, 2020, RBC Capital Markets discontinued its Top Pick rating. Top Pick rated securities represented an analyst’s best idea in the sector; expected to provide significant absolute returns over 12 months with a favorable risk-reward ratio. Top Pick rated securities have been reassigned to our Outperform rated securities category, which are securities expected to materially outperform sector average over 12 months.

Risk Rating:

The Speculative risk rating reflects a security’s lower level of financial or operating predictability, illiquid share trading volumes, high balance sheet leverage, or limited operating history that result in a higher expectation of financial and/or stock price volatility.

RBC Capital Markets analysts have received (or will receive) compensation based in part upon the investment banking revenues of RBC Capital Markets.

RBC Capital Markets Conflicts Policy

RBC Capital Markets Policy for Managing Conflicts of Interest in Relation to Investment Research is available from us on request. To access our current policy, clients should refer to https://www. rbccm.com/global/file-414164.pdf or send a request to RBC Capital Markets Research Publishing, P.O. Box 50, 200 Bay Street, Royal Bank Plaza, 29th Floor, South Tower, Toronto, Ontario M5J 2W7. We reserve the right to amend or supplement this policy at any time.

Dissemination of Research & Short Term Ideas

RBC Capital Markets endeavours to make all reasonable efforts to provide research simultaneously to all eligible clients, having regard to local time zones in overseas jurisdictions. Subject to any applicable regulatory considerations, “eligible clients” may include RBC Capital Markets institutional clients globally, the retail divisions of RBC Dominion Securities Inc. and RBC Capital Markets LLC, and affiliates. RBC Capital Markets’ equity research is posted to our proprietary websites to ensure eligible clients receive coverage initiations and changes in rating, targets and opinions in a timely manner. Additional distribution may be done by the sales personnel via email, fax or regular mail. Clients may also receive our research via third party vendors. Please contact your investment advisor or institutional salesperson for more information regarding RBC Capital Markets research. RBC Capital Markets also provides eligible clients with access to SPARC on its proprietary INSIGHT website. SPARC contains market color and commentary, and may also contain Short-Term Trade Ideas regarding the securities of subject companies discussed in this or other research reports. A Short-Term Trade Idea reflects the research analyst’s directional view regarding the price of the security of a subject company in the coming days or weeks, based on market and trading events. A Short-Term Trade Idea may differ from the price targets and/or recommendations in our published research reports reflecting the research analyst’s views of the longer-term (one year) prospects of the subject company, as a result of the differing time horizons, methodologies and/or other factors. Thus, it is possible that the security of a subject company that is considered a long-term ‘Sector Perform’ or even an ‘Underperform’ might be a short-term buying opportunity as a result of temporary selling pressure in the market; conversely, the security of a subject company that is rated a long-term ‘Outperform’ could be considered susceptible to a short-term downward price correction. Short-Term Trade Ideas are not ratings, nor are they part of any ratings system, and RBC Capital Markets generally does not intend, nor undertakes any obligation, to maintain or update Short-Term Trade Ideas. Short-Term Trade Ideas discussed in SPARC may not be suitable for all investors and have not been tailored to individual investor circumstances and objectives, and investors should make their own independent decisions regarding any Short-Term Trade Ideas discussed therein.

Conflict Disclosures

In the event that this is a compendium report (covers six or more subject companies), RBC DS may choose to provide specific disclosures for the subject companies by reference. To access RBC CM’s current disclosures of these companies, please go to https://www.rbccm.com/GLDisclosure/PublicWeb/DisclosureLookup.aspx?entityId=1. Such information is also available upon request to RBC Dominion Securities, Attention: Manager, Portfolio Advisory Group, 155 Wellington Street West, 17th Floor, Toronto, ON M5V 3K7. The authors are employed by RBC Dominion Securities Inc., a securities broker-dealer with principal offices located in Toronto, Canada.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”) and is licensed for use by RBC. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

References herein to “LIBOR”, “LIBO Rate”, “L” or other LIBOR abbreviations means the London interbank offered rate as administered by ICE Benchmark Administration (or any other person that takes over the administration of such rate).

Disclaimer

The information contained in this report has been compiled by RBC Dominion Securities Inc. (“RBC DS”) from sources believed by it to be reliable, but no representations or warranty, express or implied, are made by RBC DS or any other person as to its accuracy, completeness or correctness. All opinions and estimates contained in this report constitute RBC DS’ judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. This report is not an offer to sell or a solicitation of an offer to buy any securities. Additionally, this report is not, and under no circumstances should be construed as, a solicitation to act as securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. This material is prepared for general circulation to Investment Advisors and does not have regard to the particular circumstances or needs of any specific person who may read it. RBC DS and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC DS and its affiliates may also issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC DS or its affiliates may at any time have a long or short position in any such security or option thereon. Neither RBC DS nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. No matter contained in this document may be reproduced or copied by any means without the prior written consent of RBC DS in each instance.

In all jurisdictions where RBC Capital Markets conducts business, we do not offer investment advice on Royal Bank of Canada. Certain regulations prohibit member firms from soliciting orders and offering investment advice or opinions on their own stock. References to Royal Bank are for informational purposes only and not intended as a direct or implied recommendation for investing in Royal Bank and all related securities.

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ®Registered trademarks of Royal Bank of Canada. Used under licence. ©2020 Royal Bank of Canada. All rights reserved.