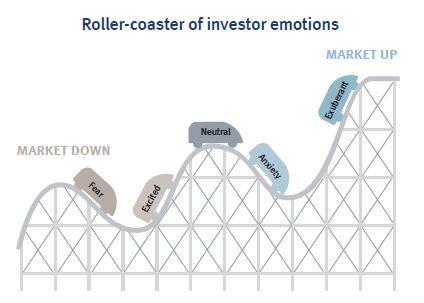

Watching the value of your investments fluctuate can be an emotional experience. When markets are falling and your investments decrease in value, you may become anxious and worry about what impact it will have on your overall financial well-being. When markets are climbing, you may become excited and over-confident, willing to take on additional risk to see your assets grow further. All of these emotions are entirely understandable but reacting based on these emotions can be detrimental to you reaching your investment goals.

During periods of heightened emotions, decisions tend to be

based on short-term objectives, without much consideration

for their long-term implications. While it may be difficult to

watch the value of your portfolio decline, it may be even

more difficult to recover from a series of poorly timed

decisions. Remaining calm during all market environments

and staying focused on the long term is critical to reaching

your financial goals.

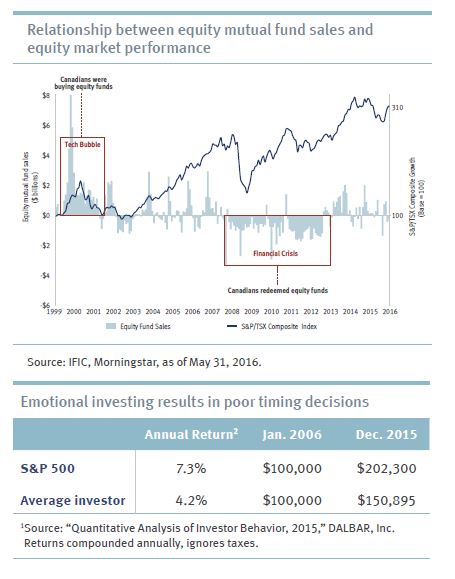

Emotions can prove costly

When shopping, most consumers prefer to look for deals

on goods and aim to pay the lowest price possible. Yet,

when it comes to investing, this is one area where many

consumers consistently pay higher prices and avoid the

opportunity to pay lower prices. The chart to the right shows

a positive relationship between equity mutual fund sales and

equity market performance. As equity markets were soaring

during the tech bubble of 1999/2000, so were equity fund

sales. And following the financial crisis of 2008/09 when

equity markets tumbled, Canadians redeemed their equity

funds. The problem is that investors are consistently buying

high and selling low, a situation that can lead to disappointing

portfolio performance over the long term.

A study by DALBAR, a leading financial services market

research firm, found that the average annual return for an

equity mutual fund investor over the 10-year period ending

December 2015 was 4.2%. This compares to the S&P 500

Index, which returned 7.3% per year over the same period.

The study concluded that underperformance was mostly

explained by emotional reactions during periods of market

stress, resulting in poor timing decisions. After 10 years,

this underperformance would have resulted in a difference

of over $50,000 on an initial investment of $100,000.

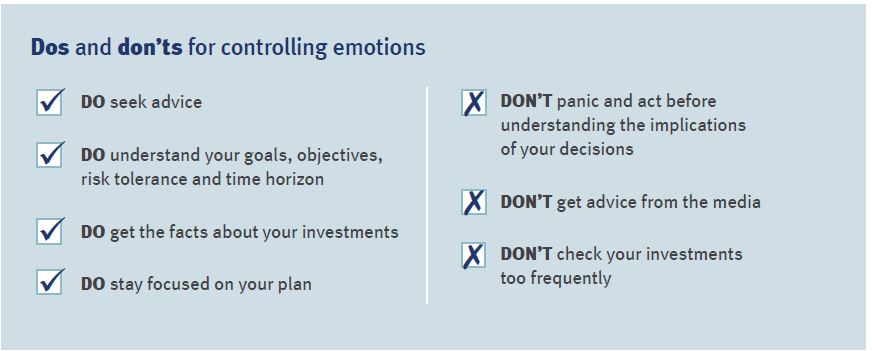

Controlling your emotions

Remaining calm during all market environments and staying focused is critical to reaching your goals. Here are a few suggestions:

1. Ask big picture questions

There are reasons why you began investing in the first

place, which in turn helped determine how your portfolio

is constructed. It may be helpful to revisit these goals when

volatility picks up to see if anything has changed. Consider

asking yourself questions like:

Are my goals the same now that my investments have

declined?

Is my investment time horizon the same as it was when we built my portfolio?

Is my financial situation the same?

Is my portfolio aligned with my risk tolerance?

Does my portfolio have an appropriate level of diversification?

If the answer is “yes” to these questions, then ask yourself why you need to make any changes, particularly knowing the risks involved in getting it wrong. If the only thing that has changed is the short-term value of your portfolio, should this affect your long-term plan? These bigger picture questions can help shift the focus away from the short-term discomfort.

However, if the answer to any of the questions is “no,” discuss these changes with your advisor, as they will review and work with you to adjust your investment plan.

2. Tune out the headlines

A major source of uncertainty comes from the media,

where the focus tends to be negative and sometimes

alarmist. It is extremely difficult for forecasters to

accurately predict where markets will go in the short term

and no forecaster has insight into your unique situation.

Watching the news and reading headlines will only serve

to heighten your anxiety during difficult times and increase

the chance that you’ll react emotionally.

3. Stop constantly checking your investments

Are you guilty of obsessively checking your portfolio on

a daily basis? One way to reduce the emotional impact of

market volatility is by simply looking at it less often. The

market tends to be more volatile over shorter time periods,

so the more often you check, the greater the likelihood

you’ll see wider fluctuations in the value of your portfolio.

Checking your portfolio monthly, quarterly or even yearly

means you’re more likely to see trends over the long term.

4. Speak with an advisor

Many advisors have been through multiple market cycles

and have seen difficult periods before. Having an objective

advisor who can share their expertise and experience

and provide you with advice during difficult times can be

extremely important in keeping your plan on track.

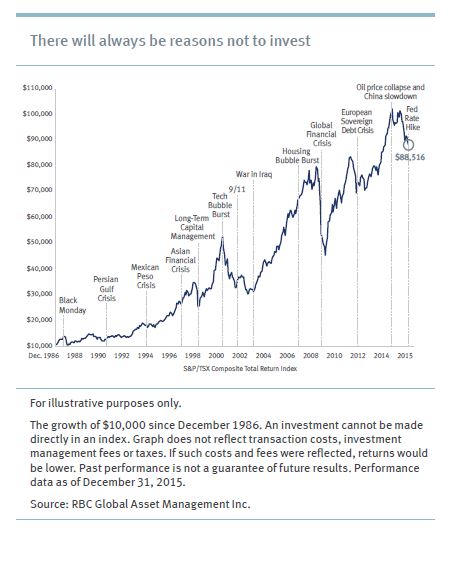

Thinking about taking a break?

If you are nervous about market volatility and are thinking about moving your investments to cash, it is important to understand that by doing so you will introduce several new risks to your portfolio. While moving to cash may feel safe, remaining in cash for an extended period of time ultimately erodes your purchasing power. Even at a modest inflation rate of 2%, you will lose 10% of your purchasing power

over a five-year period. Inflation is a serious threat to your long-term plan, it’s just less obvious because the face value of the assets don’t decline.

Here are some questions to consider if you are thinking about moving to the sidelines:

What is my plan for getting back into the markets?

What are the tax implications of my decision?

Where should I direct my savings in the meantime?

How long can I afford to be out of the market while ensuring my goals are still achievable?

When will I know it is safe to get back in?

How can I ensure that I do not continue to pull out of the markets in the future?

Keep your emotions in check

Reacting emotionally often complicates the investment process and the more you try to time the markets, the worse off you are likely to be. Investment plans shouldn’t be derailed by uncertainty and periods of volatility. Make sure to sit down with an advisor on a regular basis to review your risk tolerance, time horizon and objectives to ensure your plan is appropriate and you can remain on track.

Source: RBC Global Asset Management