DIARY OF A PORTFOLIO MANAGER

December 12, 2025

“I don't want a lot for Christmas, there is just one thing I need (and I)

Don't care about the presents underneath the Christmas tree

I don't need to hang my stocking there upon the fireplace (ah)

Santa Claus won't make me happy with a toy on Christmas Day”

All I Want for Christmas is You, Mariah Carey

Good afternoon,

Apparently, Mariah Carey earns $3mm in royalties every year from that song being played over and over again on every music streaming service I subscribe to. Not a bad gig for her. Less so for the rest of us.

Fundamentals?

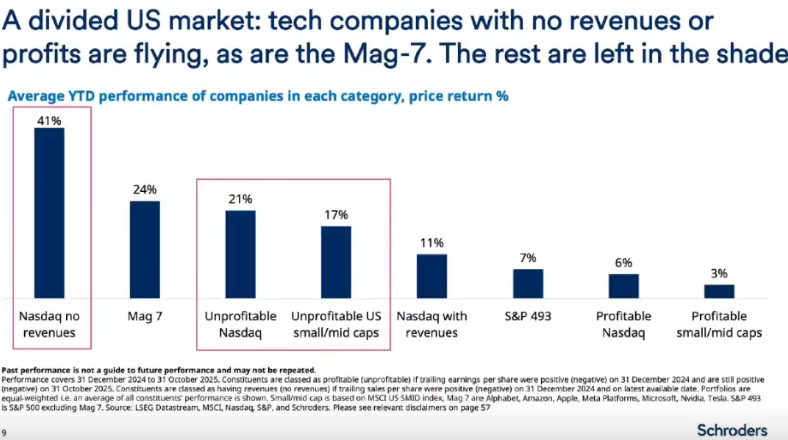

As you are aware by now (hopefully), I look at actual fundamentals and valuations when making recommendations. Appato time. I still can’t understand why business with no revenue has trounced business with revenue yet unprofitable and those have trounced those actually profitable. This can’t end well but we are well poised to profit when there is a transition.

Global Equity Outlook: More but less

RBC Wealth Management has launched the Global Insight 2026 Outlook, titled “The future is here…and gathering speed.” In this week’s letter, we highlight some key excerpts from the outlook report that brings unique perspectives on the near- and long-term market opportunities.

After three successive years of above-average market appreciation, delivering a fourth will be a tall order but not entirely out of the question. Whether equity market returns are “merely” positive or above average, either outcome will depend on the major economies, especially the U.S., avoiding recession and on the current consensus forecasts for GDP, earnings growth, inflation, and interest rates being in the right “ballpark.”

While consensus estimates for US. 2026 GDP growth sit at only 1.9 percent, we think there are some factors at play which might push that growth rate into the potentially more rewarding zone above two percent including a rebound from the government shutdown, the lagged effect of monetary easing, and a capital spending boost from tax policy changes. AI is also very important to GDP growth expectations in 2026 and beyond because of the dramatic growth in capital spending by the big developers and the expectation that more and more successful applications of AI will emerge which promise to prompt heavy future investment by users.

Meanwhile, most developed economies are running stimulative monetary and fiscal policies in the same direction of the United States. These feature rate cutting by central banks, a commitment to much higher defense spending, initiatives to boost power-generation capacity and strengthen grids, as well as to develop AI capability.

They are also faced with many of the same challenges: anemic GDP growth, trade uncertainties, mounting fiscal debt burdens, and fraught politics.

I can see a plausible path to another year of positive gains for most major stock markets – but likely at a more sober pace. Slower earnings growth is the more likely outcome outside of the United States. GDP growth everywhere needs to shift into a higher gear than is currently embodied in consensus forecasts to lift the prospects for equity market performance beyond the “merely” positive toward “above average.”

Commodity & Currency Outlook

Oil: OPEC+ has opted to pause additional output increases for the first quarter of the year. We believe this strategic adjustment has the potential to remove some of the downward pressure and provide some degree of support for prices in the new year.

Gold: The price of gold reached new all-time highs in 2025, driven by a combination of geopolitical risk, a declining interest rate environment, policy uncertainty, and global central banks diversifying reserves away from the U.S. dollar. Looking ahead to 2026, RBC Capital Markets expects continued central bank purchases and sustained macroeconomic uncertainty to maintain sufficient demand to keep bullion prices elevated.

Copper: Despite Chinese economic data revealing factory activity shrinking for most months throughout the year, robust growth in China’s EV production and ongoing renewable energy installations help act as offsets. If the declining rate environment in the U.S. continues, RBC Capital Markets believes we should see higher copper prices through 2027.

Next Quarter Century

Looking ahead to the next year is a necessary exercise for investors, but we think it’s even more useful to focus on investment themes that can endure for years or even decades. In the next quarter century, some themes that have emerged relatively recently should persist, and new themes have the potential to shape global economic development and drive certain sectors.

Continuation of longstanding themes: the continued ascent of China and the global middle class, demographic challenges, tech sector-driven economic growth and innovation.

Relatively new themes that may persist: multipolar world order, deglobalization, artificial intelligence, climate change, fiscal sustainability.

New themes: the prospect of diminished U.S. exceptionalism, faster productivity growth, a peak in oil demand, the rise of India and Southeast Asia.

Takeaways

For the full report, and additional region-specific commentary, please see the Global Insight 2026 Outlook report.

Thank you for another great year. On a closing note, I am working on my year end recommended reading list. Always easier to think about than put on the page. Should you have any questions between now and then, please don’t hesitate to reach out.