Financial decisions touch so many aspects of life. Some decisions are simpler, ranging from day-to-day purchases and choosing products and services for you and your family, while others are more complex, such as saving for your children’s education, caring for an aging parent, or planning for long-term life and retirement goals. And while the bulk of those decisions often take place throughout the various stages of adulthood, that doesn’t mean individuals should wait until those decisions are on the horizon to learn about and understand the related financial concepts and planning approaches. When it comes to financial literacy, a mindset of “it’s never too early to start” is a central one to adopt, as building sound financial management skills early on enables individuals to be confident, informed and capable decision-makers throughout life.

Unfortunately, however, the reality is still that many individuals, and specifically younger Canadians, are not adequately equipped with financial knowledge and skills. In fact, according to a recent report from The Organisation for Economic Co-Operation and Development (OECD) based on the Programme for International Student Assessment (PISA) on financial literacy, 30 percent of teens (the assessment sample was 15-year-olds) still score at or below the minimum threshold of financial knowledge. This means, at best, being able to identify common financial terms, make simple decisions on everyday spending, and recognize the difference between needs and wants. What’s more, less than one-quarter scored at the highest level, which is defined as being able to analyze complex financial products, solve non-routine financial problems and show an understanding of the wider financial landscape.1 And while these particular statistics are limited to teens, broader research and studies also indicate that a lack of financial literacy is not unique to younger individuals in Canada.

Did you know?

According to the most recent Canadian Financial Capability Survey, only 7.1 percent of Canadian adults considered themselves “very knowledgeable” financially.2

To address the findings relative to younger generations and also with a focus on making financial education a priority for everyone, regardless of age or life stage, RBC Wealth Management (RBC WM) has developed a new learning platform to help individuals build sound financial management skills — the RBC WM Financial Literacy program.

![]()

What is the RBC WM Financial Literacy program?

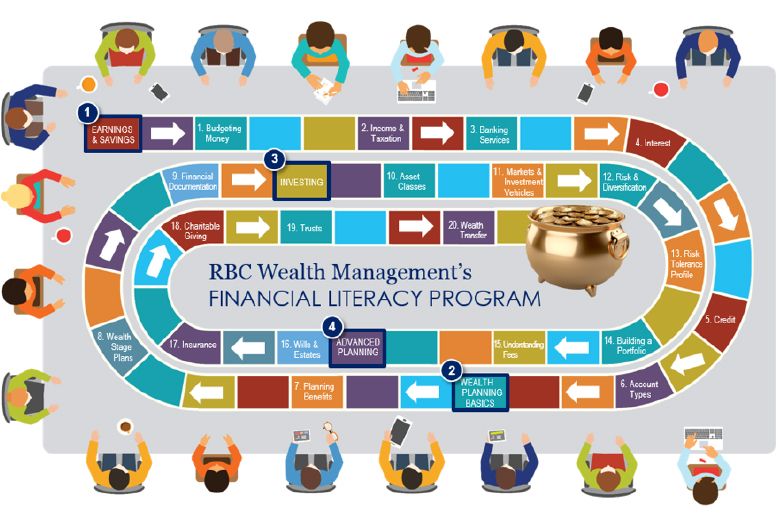

Launched in January of 2018, the RBC WM Financial Literacy (FL) program has been created for individuals who are 16 years of age or older, and it features four main education focus areas — Earnings & Savings, Wealth Planning Basics, Investing, and Advanced Planning — and a total of 20 learning modules. Please see below for a complete list of modules and additional details.

In designing this program, RBC WM has combined three key principles that are proven to be effective when it comes to financial education: formal, comprehensive and structured learning opportunities. This holistic learning model has been created based on industry research surrounding methods of financial education. For example, the RBC WM 2017 Wealth Transfer Report found that while informal learning via family is the most common method of financial education, the most effective way to build financial literacy is actually through formal, structured learning.

The specific approach of the program extends beyond basic informational and instructive learning, using a wide variety of case studies and practical exercises to help individuals apply and embed the lessons and learnings with their day-to-day financial decisions. Through this format and by providing hands-on opportunities to practise the knowledge, this program takes learning further and shows individuals how to use their knowledge in various real-life scenarios. Currently, the RBC WM FL program is advisor-led, so individuals participating in the program gain the added benefits of being taught by a financial professional who acts as their main resource during the learning sessions.

Building financial literacy at every life stage

RBC WM recognizes there are a number of realities many families are facing that drive home the increased significance of building sound financial management skills and has designed the RBC WM FL program to help support multi-generational families.

For younger individuals, research indicates that there is a strong relationship between early learning and confidence level when it comes to financial decision-making, but unfortunately, learning is typically taking place much later than it should (average age is 26, based on findings from the RBC WM 2017 Wealth Transfer Report), leaving many heading into early adulthood with little foundational knowledge, experience or understanding of financial or wealth planning topics. Additionally, when transitioning to greater financial independence, the pressures of both short- and long-term financial decisions are often felt hardest among younger individuals, and these pressures seem to be growing amidst substantial shifts in the job market, economy and technology, and with the impending largest wealth transfer in history underway in Canada. As such, the importance of sound financial management skills is quickly rising to the forefront, and formal education in this regard can be an invaluable tool in helping younger individuals ease the stress around managing finances and in setting financial goals for their futures.

For adults, life events at any stage can often bring to light the importance of having strong foundational knowledge and awareness about a full range of wealth planning topics. For example, according to the 2016 Census, there’s been a 20 percent increase in the number of seniors since 2011 and also during that time a 41 percent increase in those age 100 or over.3 With this significant shift in population demographics, as well as longer life expectancies in Canada, many adults will need to plan for a potentially longer retirement, the potential for health issues or caring for an elder parent/grandparent, but may not have much knowledge or experience in how best to plan financially for these scenarios or what aspects of planning are crucial for this stage of life. As well, some families may be in a position where one partner has traditionally handled all of the finances, and while that may have been the easiest approach, it’s important to remember that unexpected events or life changes could create significant challenges if both partners aren’t educated and comfortable as the family’s financial decision-maker.

Generally speaking, the overall goal of the RBC WM FL program is to make structured, comprehensive financial education accessible and available for all individuals who think they could benefit from improved financial knowledge. While there is a heightened focus on younger generations and the importance of equipping them with sound financial management skills early on, this program is equally relevant and valuable for individuals of all ages and life stages, recognizing that financial literacy is something that’s important for everyone within the family.

The bigger picture – helping to prepare younger Canadians

RBC Future Launch is RBC’s largest-ever commitment to Canada’s future, helping young Canadians prepare for success and access meaningful employment by addressing three critical gaps: experience, skills and networking. One of the main focus areas within RBC Future Launch is helping ensure youth are future ready by providing equitable access to 21st century skills, part of which includes making education a top priority when it comes to financial literacy, critical thinking and problem solving. This aspect is at the core of the RBC WM FL program, the program itself serving as a key tool to help achieve and support the overall youth strategy, while at the same time assisting younger individuals with handling the realities of today and in preparing for the potential challenges and changes of tomorrow.

1. Earnings & Savings

- Budgeting money

- Expenses and how to budget effectively

- Income and taxation

- Sources of income and tax rules

- Banking services

- Bank accounts and digital services

- Interest

- How interest works for the borrower and the lender

- Credit

- Credit scores, borrowing options, mortgages, staying financially fit

- Account types

- Investment accounts available to Canadians

2. Wealth Planning Basics

- Planning benefits

- Planning process approaches, components, benefits and steps

- Wealth stage plans

- Examining the goals of an early saver, a mid-life accumulator, a preserver/spender

- Financial documentation

- Common documents in investing, banking and planning

3. Investing

- Asset classes

- Understanding cash, bonds and stocks

- Markets & investment vehicles

- Examining capital, secondary and stock markets; mutual funds, ETFs, etc.

- Risk & diversification

- Importance of diversification and “risk and return” relationship

- Risk tolerance profile

- Determining investment profile and comfort level with risk

- Building a portfolio

- Building a portfolio for an early saver, a mid-life accumulator, a preserver/spender

- Understanding fees

- What fees are and why they exist

4. Advanced Planning

- Wills & estates

- Components, importance of planning, documentation

- Insurance

- How and where insurance fits into wealth planning

- Charitable giving

- Categories of giving and types of donations

- Trusts

- Trust types, purposes and benefits

- Wealth transfer

- Planning for passing wealth to the next generation

Reference:

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.