Perspective on Current Markets Q4 2019

Although risks remain especially in light of the novel coronavirus outbreak, several positive signals have led us to a more constructive outlook with lesser odds of a negative scenario unfolding.

Economic growth may be bottoming

After nearly two years of decline, economic growth may be close to bottoming. While actual data has yet to improve, leading indicators of growth have stabilized and/or turned higher in most major regions. In 2019, the economy has been supported by a strong service sector and resilient consumers, offsetting weakness in manufacturing. More recently, monetary easing has helped stabilize economies and we expect the boost from lower interest rates to kick in on a lagged basis. We have, however, trimmed our outlook for 2020 global growth to 3.25% from 3.50%, mainly because of slower-than-expected momentum carrying over from 2019. Emerging-market economies are set to rebound, while developed-market growth may continue to decelerate marginally. With this updated forecast, we expect global growth in 2020 to match that of 2019, which is an encouraging sign after two years of deceleration.

Where do we go from Here?

Macro risks have faded, but not disappeared

Progress on U.S.-China trade and Brexit has reduced two of the key macro risks to our outlook. Trade relations between the U.S. and China have improved as the two countries are nearing a “Phase One” trade deal. That said, there remains friction between the world’s two largest economies and there is no certainty that they will reach a deal that significantly improves the global trade outlook. With Boris Johnson’s delayed and disputed Brexit Bill becoming law a great deal of uncertainty surrounding Brexit has shrunk. The U.K.’s departure from the EU will still inflict economic damage, but less than we had initially feared. The U.S. presidential election in November is likely to provide a new source of uncertainty as the campaign unfolds. Overall, we believe that the macro risks facing economies and markets are less severe than we would have imagined a quarter ago.

Odds of imminent recession reduced slightly

Our assessment of the U.S. business cycle continues to indicate that we are late in the cycle, a view that we have held over the past few years. That said, some of the inputs to our scorecard framework have become less concerning recently. The most noticeable change is that the U.S. yield curve – proxied by the spread between 3-month and 10- year Treasury yields – is no longer inverted. This indicator has been a classic recession signal and the steepening in the yield curve since the summer suggests that the odds of recession have declined. However, other measures continue to show that we are fairly late in the business cycle. For example, most output-gap estimates suggest that the U.S economy is already operating at full capacity. We estimate the risk of recession at approximately 35% over the next year, which is still elevated but down from our prior assessment of 40%.

U.S. dollar tailwinds are waning

After touching multi-decade lows in 2011, the U.S. dollar has appreciated for nearly nine years, buoyed by relatively strong growth and higher interest rates. These tailwinds are beginning to dissipate, however, as the Fed has undertaken a series of rate cuts and resumed quantitative easing. This year’s U.S. election introduces additional downside risk for the greenback, adding to the mounting headwinds of overvaluation, and fiscal and trade deficits. An acceleration in global growth would further erode the relative attractiveness of the dollar and tip the greenback into a period of sustained weakness. In this environment, we are constructive on emerging-market currencies with strong fundamentals and expect the euro and yen to outperform the loonie and the pound.

Central banks deliver monetary stimulus

Financial assets benefited this year from the major tailwind of aggressive monetary easing. The U.S., the Eurozone, China and India all lowered interest rates and some regions restarted quantitative easing. While the U.K. and Japan did not provide additional monetary support, they did not dial back prior stimulus efforts. One challenge that this new round of stimulus presents is the possibility that policymakers will have little room for additional easing in the event that economies require more stimulus. While some central banks have lowered rates into negative territory, we hope that such unorthodox policies don’t last as they could have unintended consequences. With substantial monetary stimulus in place, a logical next step would be for governments to turn to fiscal spending as a tool for supporting economic growth.

Implications

Boosting Equity Allocation as Economy stabilizes, Downsize Risks Diminish

- The global economy is showing signs of stabilization after nearly two years of deceleration. Leading indicators of growth are bottoming and, while the business cycle is indeed mature, traditional gauges of recession risk over the year ahead have become less acute. The bulk of the economic slowdown over the past two years stemmed from manufacturing weakness related to protectionism and business confidence. As various macro threats diminish, consumers have remained healthy and spending is likely to continue fueling the expansion.

- A number of challenges could still disrupt our positive outlook, but downside risks have arguably shrunk given Brexit approval in British Parliament and Chinese stimulus. With the Brexit passed and U.S.-China relations improving as negotiations move toward finalizing a phase-one deal. In our view, the worst-case outcomes we had feared in prior quarters are now less likely to materialize.

- Also helping the economy is the fact that central banks have eased monetary policy so far this year. The Fed delivered three cuts since July and is once again expanding its balance sheet, purchasing short-term Treasuries at a rate of US$60 billion per month. In Europe, the ECB cut rates to -0.50% from -0.40% and also restarted a 20billion euros per month bond-purchase program. Several other global central banks have also cut rates to stimulate their economies, and the broad-based easing of financial conditions is likely to support both economic growth and investors’ appetite for risk-taking.

For Equities Markets:

- Reversing much of the damage from 2018, global equities have enjoyed a powerful and broad-based rally in 2019, with economically-sensitive sectors and investment styles leading the charge in the second half of the year. Cyclicals began to outperform defensives, and value stocks have led growth stocks since August 2019. This rotation in leadership has in the past come in advance of an improving economy and a sustained rally in risk assets.

- Expanding multiples have been the main source of returns in 2019 as investors price in an eventual rebound in earnings growth. The S&P 500 Index has gained over 25% this year and climbed above our modelled estimate of fair value while earnings growth has been flat. Looking ahead, analysts expect corporate profits to grow at relatively normal mid-to-high single-digit rates, which suggests a reasonable possibility of mid-to-high single-digit equity-market returns over the year ahead. However, U.S. equities being above fair value has historically been associated with higher levels of volatility and represents a vulnerability for stocks should profit growth fail to recover. After a decade of lagging performance, equities in Europe, Asia and Emerging Markets continue to trade beneath fair value.

For Fixed Income Markets:

- Bond yields bottomed in the summer/fall of 2019 as the prospect of stabilizing/better economic growth reduced the demand for safe-haven assets. The U.S. 10-year yield has been climbing irregularly from its low of 1.45% in September but remains below our estimated equilibrium level. Although a variety of structural headwinds continue to depress real interest rates (i.e. demographics and shifting preferences in saving versus spending), should the economy’s pulse quicken bond yields are likely to continue rising, generating unimpressive returns for sovereign bonds particularly outside of North America.

For Asset Mix:

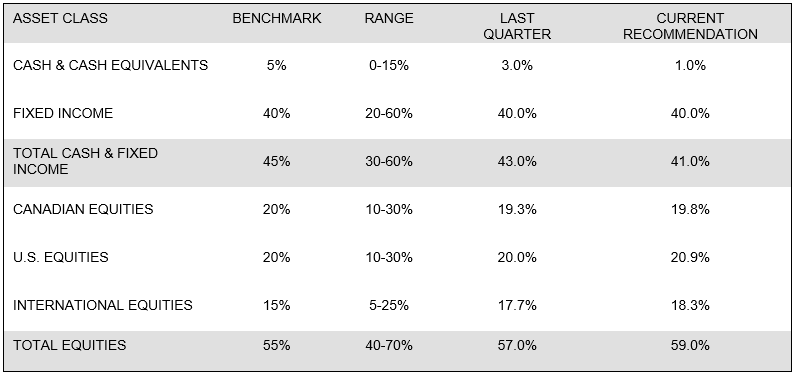

- In our view, the economy is likely to continue expanding over our 12-month horizon and, against this backdrop, we expect stocks to outperform bonds. While challenges remain, during the past quarter we became more constructive on the outlook for risk assets given fading headwinds related to Brexit and trade, yield curves that are no longer inverted and the persistence of the market rotation into economically-sensitive sectors and styles. As a result, we boosted the equity allocation in our portfolios over the period, adding two percentage points to stocks in our model asset mix, sourced from cash. Our current recommended asset mix for a global balanced investor is 59.0% equities (strategic: “neutral”: 55%), 40.0% bonds (strategic “neutral”: 43%) and 1.0% in cash.

How We Are Positioned To Take Advantage Of This Outlook:

Global Asset Mix:

Boosting equity weight, sourced from cash

In our view, the economy is likely to continue to expand at a moderate pace and we therefore expect bond yields to be relatively contained. We remain underweight fixed income given uninspiring return projections over our 1-year forecast horizon. Stocks offer the potential for bigger gains and, balancing the risks and rewards, we think that the risk premium between stocks and bonds is worth capturing at this time. As a result, we have leaned toward taking on more risk this quarter after de-risking our portfolios for more than two years. Stabilization in economic leading indicators, the rotation into value, and improving global market breadth have heightened our conviction in a positive outcome for risk assets. We added two percentage points to our equity allocation this quarter, sourced from cash, marking the first steps in the reversal of our prior de-risking. For a balanced, global investor, we currently recommend an asset mix of 59% equities (strategic neutral position: 55%) and 40% fixed income (strategic neutral position: 43%), with the balance in cash.

Geographic allocations are as follows:

- Canada 19.8%

- United States 20.9%

- International 18.3%

Risk / Reward to our Strategy

Low-yield world is likely to persist

Although bond yields have rebounded somewhat in the last quarter, we don’t believe this increase marks the start of a sustained rise in yields. Real interest rates are being depressed by a number of secular factors such as aging populations, an increased preference for saving versus spending, and slower rates of economic growth. The downward pressure on real rates from these forces is expected to reverse only marginally over the coming decade. We forecast that inflation will be relatively stable, meaning the direction of bond yields will be linked to changes in real interest rates. Our models suggest that bonds are susceptible to valuation risk as yields are below their equilibrium levels, especially outside North America. However, we think that any increase in yields is likely to be gradual and extend over a long period. Given the starting point of extraordinarily low yields and the fact that they are likely to move higher over time, if only a little, we can expect low sovereign-bond returns for the foreseeable future.

Stocks soared in 2019, but could still have room to run

Equities delivered impressive gains in 2019 amid low interest rates, stable inflation and moderate economic growth. The S&P 500 has rallied almost 30% in 2019 and is now the closest to fair value of the major indexes that we track, while stock markets outside the U.S. still look quite attractive. Profit growth will likely need to resume this year to support further equity gains. Analysts expect earnings growth to re-accelerate and a variety of market signals reinforce this view. Since the summer, economically-sensitive sectors have outperformed defensives, value stocks have led the growth style, and international markets have participated in the rally. In the past, these types of market rotations have been associated with improving economic and corporate-profit growth, and may indicate the bull market has room to run.

Conclusion:

2019 was a good year for equity investors. The S&P 500 was up by almost 30%, while the TSX was no slouch either, delivering close to a 20% advance. While these gains were partly attributable to making back the ground lost in 2018’s August-to-Christmas eve stock market swoon, both indexes set new all-time highs in the process.

For the coming year, comparisons will be more difficult for the opposite reason – 2019 has finished on a very strong note with both indexes at or near their highest levels of the year. Nonetheless, we have a constructive outlook for stocks for 2020. The economic expansion in both the U.S. and Canada should have further to run, underpinned by accommodative credit conditions everywhere, the robust good health of the American consumer, easing U.S.-China trade tensions, and the likelihood both countries (along with most developed economies) will deliver some fiscal stimulus. Corporate earnings will likely increase, as should dividends and stock buybacks, pushing share prices higher.

Some of these good things have already arrived in the closing weeks of the year just ended, transforming the gloom of 2019 around trade and recession talk into a somewhat sunnier outlook for most economies. We have bullish expectations for stock prices but at the same time we are approaching the equity market with more caution than at any time in the past decade.

Curveballs

Our caution stems from several factors all relating to the U.S. economy, keeping in mind that U.S. recessions have historically been associated with equity bear markets in all the developed economies. The first development that demands an elevated level of investor vigilance is the inversion of the yield curve that occurred back in August when short-term interest rates finished the month higher than long-term rates. Normally the opposite would be true. The previous time such an inversion occurred was January 2006, 23 months before the start of the recession in December 2007. Since World War II, the U.S. yield curve has inverted 10 times (not counting the latest instance). In nine of those instances, a recession followed on average 14 months later.

The yield curve is only one of the six indicators that we use to gauge the probability of a U.S. recession arriving. Four of the six are still giving the economy a “green light.” That said, they are all much closer to flashing red than they were a year ago. However, it’s not a foregone conclusion they will turn negative; instances of close calls followed by a rebound are common enough.

Another challenge will be the headwind of slow growth. Our estimate for U.S. GDP growth next year is 1.75% (ditto for Canada), much closer to zero than the 2.5% to 3.5% run-rate of prior cycles. Occasional negative quarters inducing more frequent bouts of market volatility can’t be ruled out.

Staying loose

The most important positive factor underpinning our bullish outlook for the economy and stock markets is the fact that credit conditions remain unusually “easy.” The arrival of “tight money” (i.e., prohibitively high interest rates simultaneous with a sharply reduced willingness of banks to lend) has preceded every U.S. recession but one since the 1930s.

Money is not “tight.” Borrowing rates are very low and could go lower. The Fed has cut three times. The European Central Bank has cut its base rate to minus-0.70% and reinstated quantitative easing. The Bank of Canada has struck a dovish tone, indicating it might cut.

Confident consumers

The other tailwind for the U.S. economy (and the global economy) is the robust good health of the American consumer who shows no signs of running out of steam. The unemployment rate is sitting at a half-century low. The U.S. Labor Department reports seven million jobs are currently unfilled (versus six million unemployed). Labour tightness has pushed average hourly earnings gains up to 3.5% from just 2% two years ago. All this has produced a confident consumer who can go on spending at a moderate rate, which should be sufficient to offset any weakness from other sectors.

On top of this, the U.S. election season is likely to produce promises of more tax cuts and increased spending. In Canada, consumers are likely to be buoyed by an expected tax cut for the middle class in the coming budget.

Reasonable valuations

Finally, we are encouraged by the fact that the U.S. and Canadian equity markets don’t look precarious to us. Consensus earnings estimates for the coming year in both countries look reasonable and makeable. Valuations in North America are not outlandish. Stocks are downright cheap in Europe and Japan.

Broad market advance

Importantly, the breadth readings of the market are confirming what the indexes have been doing. In other words, as the broad averages have been moving to new highs, so too have the majority of stocks. For a number of months prior to most bull-market peaks that relationship breaks down: the index gets carried higher by a dwindling number of high-performing, large-cap favorites while a growing majority of issues are either treading water or moving into outright downtrends. No such divergence has appeared, lending confidence to the idea that this market advance has further to go.

And the verdict is …

For the past decade we have been well served by the idea that portfolios should maintain at least a full, target-weight exposure to equities as long as there was no U.S. recession in sight. We continue to be of that view.

If and when the weight of the evidence eventually moves the probabilities of a U.S. recession/bear market to unacceptably high levels, it will be tempting to rationalize away the bad news. When that time arrives, that temptation should be resisted.